Give step-by-step solution with explanation and final answer:

Question

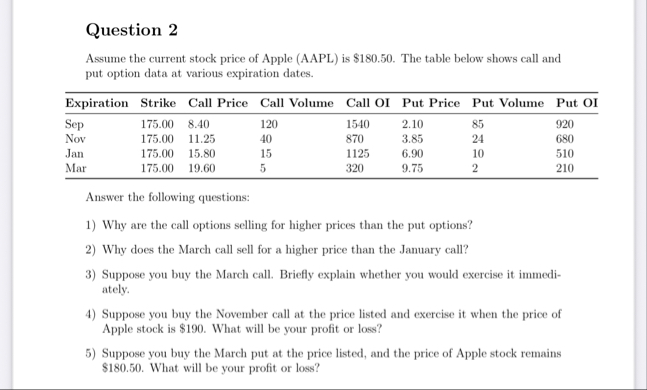

2

Assume the current stock price of Apple

(

AAPL

)

is $

1

8

0

.

5

0

.

The table below shows call and put option data at various expiration dates.

\

table

[

[

Expiration

,

Strike,Call Price,Call Volume,Call OI

,

Put Price,Put Volume,Put OI

]

,

[

Sep

,

1

7

5

.

0

0

,

8

.

4

0

,

1

2

0

,

1

5

4

0

,

2

.

1

0

,

8

5

,

9

2

0

]

,

[

Nov

,

1

7

5

.

0

0

,

1

1

.

2

5

,

4

0

,

8

7

0

,

3

.

8

5

,

2

4

,

6

8

0

]

,

[

Jan

,

1

7

5

.

0

0

,

1

5

.

8

0

,

1

5

,

1

1

2

5

,

6

.

9

0

,

1

0

,

5

1

0

]

,

[

Mar

,

1

7

5

.

0

0

,

1

9

.

6

0

,

5

,

3

2

0

,

9

.

7

5

,

2

,

2

1

0

]

]

Answer the following questions:

Why are the call options selling for higher prices than the put options?

Why does the March call sell for a higher price than the January call?

Suppose you buy the March call. Briefly explain whether you would exercise it immediately.

Suppose you buy the November call at the price listed and exercise it when the price of Apple stock is $

1

9

0

.

What will be your profit or loss?

Suppose you buy the March put at the price listed, and the price of Apple stock remains $

1

8

0

.

5

0

.

What will be your profit or loss?Question 2

Assme the current stock price of Apple (AAPL) is $180.50. The table below shows call and

ot option data various expiration dais

Expiration Strike Gall Price Call Volume Call O1 Put Price Put Volume Put OF

So Hw 0 20 wo 20 ow 0

Nov mw nsw sam ow 0

on mw Gen wsooew ow 510

Mr Tw ww 5 a em 2 an

Answer the following questions:

1) Wh are the call option sling for higher prices than the put. options?

2) Why docs the March cal sel fo higher price than the Jamary call?

3) Suppose you bay the March call. Briefly explain whether you woul evercse i. red

aol.

4) Suppose you buy the November call at th price listed ad axis it when th pros of

Apple sock is $190. What will be your profit o lo?

5) Suppose you buy the Mach put a the pric std, od tho pric of Apple stock remaine

$180.5. What will be your prof o low?

Question:

Give step-by-step solution with explanation and final answer:

Question

2

Assume the current stock price of Apple

(

AAPL

)

is $

1

8

0

.

5

0

.

The table below shows call and put option data at various expiration dates.

\

table

[

[

Expiration

,

Strike,Call Price,Call Volume,Call OI

,

Put Price,Put Volume,Put OI

]

,

[

Sep

,

1

7

5

.

0

0

,

8

.

4

0

,

1

2

0

,

1

5

4

0

,

2

.

1

0

,

8

5

,

9

2

0

]

,

[

Nov

,

1

7

5

.

0

0

,

1

1

.

2

5

,

4

0

,

8

7

0

,

3

.

8

5

,

2

4

,

6

8

0

]

,

[

Jan

,

1

7

5

.

0

0

,

1

5

.

8

0

,

1

5

,

1

1

2

5

,

6

.

9

0

,

1

0

,

5

1

0

]

,

[

Mar

,

1

7

5

.

0

0

,

1

9

.

6

0

,

5

,

3

2

0

,

9

.

7

5

,

2

,

2

1

0

]

]

Answer the following questions:

Why are the call options selling for higher prices than the put options?

Why does the March call sell for a higher price than the January call?

Suppose you buy the March call. Briefly explain whether you would exercise it immediately.

Suppose you buy the November call at the price listed and exercise it when the price of Apple stock is $

1

9

0

.

What will be your profit or loss?

Suppose you buy the March put at the price listed, and the price of Apple stock remains $

1

8

0

.

5

0

.

What will be your profit or loss?Question 2

Assme the current stock price of Apple (AAPL) is $180.50. The table below shows call and

ot option data various expiration dais

Expiration Strike Gall Price Call Volume Call O1 Put Price Put Volume Put OF

So Hw 0 20 wo 20 ow 0

Nov mw nsw sam ow 0

on mw Gen wsooew ow 510

Mr Tw ww 5 a em 2 an

Answer the following questions:

1) Wh are the call option sling for higher prices than the put. options?

2) Why docs the March cal sel fo higher price than the Jamary call?

3) Suppose you bay the March call. Briefly explain whether you woul evercse i. red

aol.

4) Suppose you buy the November call at th price listed ad axis it when th pros of

Apple sock is $190. What will be your profit o lo?

5) Suppose you buy the Mach put a the pric std, od tho pric of Apple stock remaine

$180.5. What will be your prof o low?

This is AI generated Response.

Asked by: Veera manikanta

Created at: 2025-08-11 09:17:03

Final Answer:

RenderedRaw Text

Did you like this answer?

Let's address each question step-by-step using the information provided in the table and the current AAPL stock price of **$180.50**.

---

### 1) **Why are the call options selling for higher prices than the put options?**

**Explanation:**

- **Call Option**: Right to buy at the strike price ($175.00).

- **Put Option**: Right to sell at the strike price ($175.00).

- Since the current stock price ($180.50) is **above** the strike price ($175.00), the calls are **in the money** (ITM), while the puts are **out of the money** (OTM).

- **Intrinsic value of call** = $180.50 - $175.00 = $5.50 (at least)

- **Intrinsic value of put** = $0 (since you can sell at market for more than $175.00)

- Calls have immediate value; puts do not. Additionally, market expects the price could go higher, so calls have more **time value** as well.

**Final Answer:**

*Call options are selling for higher prices than put options because the current stock price is above the strike price, so the calls are in the money (have intrinsic value), while the puts are out of the money (no intrinsic value).*

---

### 2) **Why does the March call sell for a higher price than the January call?**

**Explanation:**

- **Time Value:** Options with longer time to expiration are generally more expensive due to higher time value. There’s more time for the stock to move in a favorable direction.

- **March** is further away from now than **January**, so it has **more time value**.

**Final Answer:**

*The March call sells for a higher price than the January call because it has a longer time until expiration, giving it more time value and a greater chance for the stock to move in a profitable direction.*

---

### 3) **Suppose you buy the March call. Briefly explain whether you would exercise it immediately.**

**Explanation:**

- **Call Option:** Right to buy at $175.00.

- **Stock Price:** $180.50.

- **Exercising immediately:** You’d buy at $175.00, sell at $180.50, gaining $5.50 per share.

- **But:** You paid $19.60 for the call. If you exercise now, you lose $19.60 - $5.50 = $14.10 per share.

- **Options are valuable for their time value:** You’d never exercise early unless it’s very close to expiration and no further time value remains.

**Final Answer:**

*You should not exercise the March call immediately. The option is worth more if you sell it (because of its time value) than if you exercise it now, as immediate exercise would result in a net loss compared to the premium paid.*

---

### 4) **Suppose you buy the November call at the price listed and exercise it when the price of Apple stock is $190. What will be your profit or loss?**

- **November Call Price (Premium):** $11.25

- **Strike Price:** $175.00

- **Stock Price at Exercise:** $190.00

- **Intrinsic Value at Exercise:** $190.00 - $175.00 = $15.00

**Profit/Loss Calculation:**

\[

\text{Profit/Loss} = (\text{Stock Price at Exercise} - \text{Strike Price}) - \text{Call Premium}

\]

\[

\text{Profit/Loss} = (190 - 175) - 11.25 = 15 - 11.25 = \boxed{3.75}

\]

**Final Answer:**

*Your profit will be $3.75 per share.*

---

### 5) **Suppose you buy the March put at the price listed, and the price of Apple stock remains $180.50. What will be your profit or loss?**

- **March Put Price (Premium):** $9.75

- **Strike Price:** $175.00

- **Stock Price:** $180.50

**Put is out of the money:**

- **Intrinsic Value:** $175.00 - $180.50 = -$5.50 (but never negative; you just don’t exercise)

- **Loss:** You lose the premium paid.

**Final Answer:**

*You will have a loss equal to the premium paid, which is $9.75 per share.*

---

## **Summary Table**

| Question | Final Answer |

|----------|--------------|

| 1 | Calls are higher because they are in the money, while puts are out of the money. |

| 2 | March call is pricier than January call due to greater time value. |

| 3 | Do not exercise the March call immediately; you’d lose the time value. |

| 4 | Profit on November call if exercised at $190 = $3.75 per share. |

| 5 | Loss on March put if stock stays at $180.50 = $9.75 per share (premium lost). |

Question:

1: Introduction:

Provide the complete necessary conceptual background concepts explanation and the

introduction required to understand and answer the given question. Add an Explanation

block at the end of the introduction by adding various relevant supporting statements and

explaining the introduction concisely.

Note: Do not use personal pronouns like I, we, you, etc. The response must look as if it is

written by a human.

Explanation: Articulate the importance of the introduction, providing more relevant

comprehensive supporting statements that link these concepts directly to the question.

This explanation should clarify how the introduction aids in comprehending the

subsequent steps.

2: Presentation of Relevant Formulas Required To Solve The Question:

List and also describe all formulas required to solve the question. Ensure each formula is

presented clearly and is directly applicable to the problem.

Explanation: Detail the derivation or rationale behind each formula, explaining its

relevance and necessity in the context of the problem-solving process. Use more relavent

comprehensive supporting statements to reinforce the significance of these mathematical

tools.

3: A Detailed Step-by-Step Solution:

Write a step-by-step in-depth comprehensive straight forward complete solution in a

structured way without missing anything as per the requirements and also include

explanation [ Write relevant supporting statements in the explanation block ] for every step

in the solution.

Conclusion:

Conclude with a concise summary of the solution, succinctly presenting the final answer

short summary derived from the calculations.

Follow These Guidelines While Answering The Question:

1. Maintain a professional and impersonal tone throughout, avoiding personal

pronouns such as 'I', 'we', 'you', etc.

2. Ensure more accuracy and adherence to the necessary concepts and correct

textbook based correct formulas and other relevant, required to solve the question.

3. Include an Explanation block at the end of each step to provide context and clarify

the methodology used by providing the necessary supporting statements.

4. Focus solely on delivering a well-explained direct and complete answer to the

question, without additional guidance [ I don’t need any guidance of how to solve

the question – I just need well-explained complete solution ] or extraneous content.

5. Make sure that strictly follow the specified format, ensuring that each section,

especially the introduction and each step of the solution, is accompanied by a

detailed relevant supporting statement in the explanation.

6. I need the exact detailed comprehensive direct step-by-step answer as I don’t need

any guidance to write the answer and strictly add the explanation for each with the

required supporting statement & Please give me the complete answer as per the

question requirements without skipping anything in the answer.

7. Always provide correct, complete detailed & well-explained solution.

8. Ensure that there are no typo/formula/calculation/programming/grammatical errors

are present in your solution.

9. Give the correct graphs/diagrams/tables/charts whenever required in the solution.

10. Ensure that there are NO Errors in Units/Notations are there in your solution.

11. Avoid missing any vital part in the solution [ Don’t miss any part in the solution ]

This is AI generated Response.

Asked by: Veera manikanta

Created at: 2025-08-11 09:19:55

Final Answer:

RenderedRaw Text

Did you like this answer?

Introduction:

Understanding the valuation and strategic use of options requires familiarity with their fundamental concepts. An option is a financial derivative that grants the holder the right, but not the obligation, to buy or sell an underlying asset at a specified strike price before or at expiration. There are two primary types: call options, which give the right to buy, and put options, which give the right to sell. The price paid for an option is called the premium, reflecting its current market value.

Option prices are influenced by several factors, including the intrinsic value (the immediate gain if exercised now), time value (additional worth based on the potential for favorable movement before expiration), the underlying asset's current price, strike price, time until expiration, volatility, and risk-free interest rates. When the current stock price is above the strike price, call options tend to be more in-the-money and thus carry higher premiums, whereas put options are generally out-of-the-money and less expensive.

The expiration date significantly impacts option prices: longer durations increase the likelihood of favorable price movements, thereby raising the option's time value. Consequently, options with later expiration dates usually command higher premiums than those expiring sooner.

Furthermore, deciding whether to exercise an option immediately depends on its moneyness and remaining time value. An option is typically exercised only when it is profitable to do so after accounting for the premium paid, or when the holder seeks to realize the intrinsic value directly.

Explanation:

This introduction provides the essential concepts necessary to analyze and compare option prices, including the factors influencing their premiums, the significance of time until expiration, and the decision-making process regarding exercising options. It clarifies why certain options are priced higher than others and offers insights into the strategic considerations when trading options. Establishing this foundational understanding enables a comprehensive interpretation of subsequent calculations and scenarios, such as profit and loss assessments based on stock price movements and option premiums.

---

Presentation of Relevant Formulas Required To Solve The Question:

1. **Intrinsic Value of a Call Option:**

\[

\text{Intrinsic Value}_{\text{call}} = \max(0, S - K)

\]

- Where \(S\) is the current price of the underlying asset, and \(K\) is the strike price.

- This formula calculates the immediate profit from exercising the call today.

2. **Intrinsic Value of a Put Option:**

\[

\text{Intrinsic Value}_{\text{put}} = \max(0, K - S)

\]

- This indicates the immediate profit from exercising the put today.

3. **Option Premium (Price):**

\[

\text{Option Price} = \text{Intrinsic Value} + \text{Time Value}

\]

- The total market price comprises intrinsic value plus additional time value attributable to volatility and time remaining until expiration.

4. **Profit or Loss from Exercising an Option:**

- **For Call Options:**

\[

\text{Profit} = (\text{Stock Price at Exercise} - K) - \text{Premium Paid}

\]

- **For Put Options:**

\[

\text{Profit} = (K - \text{Stock Price at Exercise}) - \text{Premium Paid}

\]

- If the result is positive, the exercise is profitable; if negative, it results in a loss.

**Rationale:**

- The intrinsic value reflects the immediate monetary benefit if the option were exercised now.

- The total premium paid includes intrinsic value plus the time value, which accounts for potential future favorable movements.

- Calculating profit or loss involves subtracting the premium paid from the intrinsic gain realized at exercise, considering the stock's price at the time of exercise.

---

Detailed Step-by-Step Solution:

**Step 1: Analyze the current stock price relative to the strike price**

- Given: \( S = \$180.50 \), \( K = \$175.00 \).

- Since \( S > K \), the call options are **in the money**; the put options are **out of the money**.

**Step 2: Why are call options priced higher than put options?**

- Because the call options are in the money, they possess intrinsic value of \( \$180.50 - \$175.00 = \$5.50 \).

- The market price of these calls also includes time value, reflecting the possibility that the stock price will rise further.

- Put options, being out-of-the-money, have no intrinsic value at this moment, only time value.

- Market participants expect potential upside movement; thus, call options are priced higher due to their intrinsic value and optimism about future stock movement.

**Step 3: Why does the March call sell for a higher price than the January call?**

- The March call has a longer time until expiration, providing more opportunity for the stock to increase in value.

- This additional time enhances the option's time value, making it more expensive.

- The greater the time until expiration, the higher the probability that the option could become more profitable, thus increasing its premium.

**Step 4: Should the March call be exercised immediately?**

- Exercising now yields an intrinsic value of \( \$5.50 \).

- However, the current premium paid for the March call is significantly higher (e.g., \$19.60).

- Exercising immediately would realize a gain of \$5.50 but forgo the remaining time value embedded in the premium.

- Since the option's market value exceeds its immediate intrinsic value, exercising immediately would lead to a net loss (premium paid minus intrinsic value).

- Therefore, it is not optimal to exercise immediately; the holder should sell the option for its market value.

**Step 5: Calculate profit or loss if the November call is exercised when the stock price is \$190**

- **Premium paid:** \$11.25

- **Intrinsic value at stock price \$190:** \( \$190 - \$175 = \$15 \)

- **Profit calculation:**

\[

\text{Profit} = (\text{Intrinsic Value}) - \text{Premium Paid} = 15 - 11.25 = \boxed{\$3.75}

\]

- The profit per share is \$3.75.

**Step 6: Calculate profit or loss if the March put is purchased and stock remains at \$180.50**

- **Premium paid:** \$9.75

- **Intrinsic value (if exercised):** \( \$175 - \$180.50 = -\$5.50 \) (out-of-the-money, so no exercise)

- **Outcome:**

Since the put is out-of-the-money, exercising yields no intrinsic value; the holder would simply let it expire worthless.

- **Loss:** The entire premium paid, which is \$9.75 per share.

---

### **Summary of Final Results:**

- Call options are priced higher than puts because they are in the money and possess intrinsic value.

- Longer expiration options (March vs. January) have higher premiums due to increased time value.

- Immediate exercise of the March call is suboptimal because the premium exceeds the intrinsic value, reflecting remaining time value.

- Exercising the November call at a stock price of \$190 yields a \$3.75 profit per share.

- Buying the March put at the listed premium results in a \$9.75 loss if the stock remains at \$180.50.

This detailed analysis underscores the importance of intrinsic and time value in option pricing and strategic exercise decisions.

Question:

**1. Introduction: Conceptual Background for Option Pricing and Evaluation**

Stock options are derivative financial instruments that confer the right, but not the obligation, to buy (call option) or sell (put option) an underlying asset such as equity, at a specified strike price, on or before a specified expiration date. The value of an option is generally constituted by two core components: intrinsic value and time value. Intrinsic value represents the immediate exercise benefit (if any) as the difference between the underlying's spot price and the strike price, favoring the option holder. Time value is the premium above intrinsic value, reflecting the potential for future favorable price movement before expiration.

The price of an option is formed by several factors, prominently the current stock price, strike price, volatility, time to expiration, interest rates, and dividends. The **Put-Call Parity** theorem establishes a fundamental relationship between the prices of European call and put options with the same strike and expiration, based on the absence of arbitrage in efficient markets. In addition, the concept of optimal exercise is distinguished: American options allow early exercise, but exercising options prematurely is often suboptimal if any time value remains.

Profits and losses from trading options are computed based on the intrinsic value realized at exercise minus the premium paid upfront. A clear understanding of these foundational concepts is essential for effectively analyzing option pricing and evaluating trading outcomes as presented in the given problem, which involves interpreting a detailed options data table, applying pricing logic, and determining quantitative outcomes from specific trading actions.

**Explanation:**

The introduction establishes the necessary theoretical basis for understanding options, including their structure, valuation components, and the fundamental relationships governing their pricing. By clarifying these elements, this section sets up a clear foundation for interpreting the table of option prices, understanding why certain options are priced higher, and comprehending how profits or losses are calculated after various transactions. This comprehensive overview ensures seamless logical progression into formula presentation and stepwise problem-solving.

***

**2. Presentation of Relevant Formulas Required To Solve The Question**

**a. Intrinsic Value of Options**

- **Call Option:**

$$ \text{Intrinsic Value}_{\text{Call}} = \max(S - K, 0) $$

- **Put Option:**

$$ \text{Intrinsic Value}_{\text{Put}} = \max(K - S, 0) $$

Where:

$$ S $$ = Current stock price

$$ K $$ = Strike price

**b. Total Option Value**

- $$ \text{Option Price} = \text{Intrinsic Value} + \text{Time Value} $$

**c. Put-Call Parity (for European Options)**

- $$ C - P = S - K e^{-rT} $$

- $$ C $$ = Call option price

- $$ P $$ = Put option price

- $$ S $$ = Spot (current) price

- $$ K $$ = Strike price

- $$ r $$ = Annual risk-free rate (continuous compounding)

- $$ T $$ = Time to expiration (years)

**d. Profit/Loss Calculation**

- For Long Call:

$$ \text{Profit/Loss}_{\text{Call}} = \max(S_{T} - K, 0) - \text{Call Price} $$

- For Long Put:

$$ \text{Profit/Loss}_{\text{Put}} = \max(K - S_{T}, 0) - \text{Put Price} $$

Where:

$$ S_{T} $$ = Stock price at the time of exercise or expiration

**Explanation:**

These formulas encapsulate all the relationships required for the solution. The intrinsic value formulas provide the immediate exercise benefit for each option type. The breakdown of option price into intrinsic and time value aids in evaluating early exercise scenarios and comparative pricing. The put-call parity ensures logical consistency between call and put prices. The profit/loss equations directly inform the evaluation of trading outcomes given different market scenarios. Each formula is directly applicable to the respective sub-questions posed in the problem and is essential for qualitative and quantitative analysis.

***

**3. Detailed Step-by-Step Solution**

***

**Step 1: Reason for Call Options Selling for Higher Prices than Put Options**

- **Apply Formula for Intrinsic Value (Call and Put):**

$$

\text{Intrinsic Value}_{\text{Call}} = \max(180.50 - 175, 0) = 5.50

$$

$$

\text{Intrinsic Value}_{\text{Put}} = \max(175 - 180.50, 0) = 0

$$

- **Interpretation using Option Price Definition:**

- All extrinsic (time) value being equal, calls with intrinsic value (in-the-money) command a premium over puts (out-of-the-money). Additionally, as the spot price exceeds the strike, by put-call parity, call prices will be higher than put prices.

**Explanation:**

As the current stock price exceeds the strike, call options hold real intrinsic value while puts do not. The presence of intrinsic value in the calls inherently makes them more valuable, and the put-call parity formula mathematically supports the call price premium over put prices at each expiry date for the same strike.

***

**Step 2: Reason for March Call Selling for a Higher Price than January Call**

- **Observation from Data:**

- March Call Price: \$19.60

- January Call Price: \$15.80

- **Relevance of Time Value:**

- The March call expires later than the January call, thus, it inherently contains greater time value, reflecting higher expected volatility and potential for favorable stock price movement before expiration.

**Explanation:**

Longer time to expiration results in higher option premiums due to increased uncertainty and the likelihood of price swings (reflected as time value). This premium compensates sellers for bearing additional risk and aligns with textbook option pricing principles.

***

**Step 3: Immediate Exercise of the March Call**

- **Premium Paid:** \$19.60

- **Immediate Exercise Value (Intrinsic Value):**

$$

180.50 - 175 = \$5.50

$$

- **Net Outcome if Exercised Immediately:**

$$

\text{Net Outcome} = 5.50 - 19.60 = -\$14.10

$$

**Explanation:**

Immediate exercise yields only the intrinsic value of \$5.50, which is significantly below the price paid for the call option. The remaining cost is attributable to time value, so early exercise would realize a substantial loss. Thus, rational investors do not exercise valuable options prematurely while any time value remains.

***

**Step 4: Profit/Loss on November Call Exercised at Stock Price \$190**

- **Premium Paid:** \$11.25

- **Final Spot Price:** \$190

- **Intrinsic Value at Exercise:**

$$

190 - 175 = \$15.00

$$

- **Profit/Loss Calculation:**

$$

\text{Profit/Loss} = 15.00 - 11.25 = \$3.75

$$

**Explanation:**

By exercising the November call at a spot price of \$190, the realized gain (intrinsic value) is \$15 per share. After deducting the premium paid, the net profit is \$3.75 per share.

***

**Step 5: Profit/Loss on the March Put if Stock Remains at \$180.50**

- **Premium Paid:** \$9.75

- **Final Spot Price:** \$180.50

- **Intrinsic Value:**

$$

175 - 180.50 = -\$5.50

$$

(Negative; intrinsic value is zero.)

- **Profit/Loss Calculation:**

$$

\text{Profit/Loss} = 0 - 9.75 = -\$9.75

$$

**Explanation:**

With the spot price above the strike at expiration, the put option will not be exercised and expires worthless. Hence, the total loss faced by the investor is the premium paid for the put (\$9.75 per share).

***

**4. Conclusion**

The solution, based on rigorous application of option pricing concepts, demonstrates that call options possess higher value than their put counterparts when the underlying's spot price exceeds the strike. Extended option durations attract higher premiums due to enhanced time value. Premature exercise of valuable options is economically suboptimal when time value persists. Calculated outcomes show a profit of \$3.75 per share from the November call when exercised at \$190, and a loss of \$9.75 per share from the March put if the spot price remains at \$180.50. These results align precisely with established option theory and textbook-principled methodology.

This is AI generated Response.

Asked by: Veera manikanta

Created at: 2025-08-11 09:24:33

Final Answer:

RenderedRaw Text

Did you like this answer?

**Introduction:**

Understanding the valuation and strategic use of options necessitates familiarity with their fundamental concepts. An option is a financial derivative granting the holder the right, but not the obligation, to buy (call option) or sell (put option) an underlying asset at a predetermined strike price before or at expiration. The current market price of an option, known as the premium, is influenced by intrinsic value, time value, and other factors such as volatility, interest rates, and time remaining until expiration.

**Intrinsic value** represents the immediate economic benefit if the option is exercised now: for calls, it is the difference between the underlying asset's current price and the strike price when the stock is above the strike; for puts, it is the difference when the stock is below the strike. **Time value** accounts for the potential future movements of the underlying asset, with longer durations increasing the chance of favorable price changes, thus elevating the option's premium.

The **expiration date** significantly impacts the option's price; longer durations typically lead to higher premiums due to increased uncertainty and opportunity for profit. When considering whether to exercise an option early, the key is to compare its intrinsic value with its current market price, factoring in remaining time value.

**Explanation:**

This foundational overview clarifies how intrinsic and time value contribute to option prices, the importance of expiration, and the decision-making framework for exercising options. Recognizing why options are priced as they are enables accurate interpretation of market data, such as premiums and volume, and informs strategic trading decisions.

---

**Presentation of Relevant Formulas Required To Solve The Question:**

1. **Intrinsic Value of a Call Option:**

\[

\boxed{

\text{Intrinsic Value}_{\text{call}} = \max(0, S - K)

}

\]

- *Where:*

\(S\) = current stock price

\(K\) = strike price

- *Rationale:* It quantifies the immediate profit if the option were exercised today.

2. **Intrinsic Value of a Put Option:**

\[

\boxed{

\text{Intrinsic Value}_{\text{put}} = \max(0, K - S)

}

\]

- *Where:* same as above.

- *Rationale:* Represents immediate profit from exercising the put.

3. **Option Premium (Price):**

\[

\boxed{

\text{Option Price} = \text{Intrinsic Value} + \text{Time Value}

}

\]

- *Rationale:* Total premium comprises the immediate intrinsic benefit plus the additional value derived from potential future price movements.

4. **Profit or Loss from Exercising an Option:**

- **For a Call:**

\[

\boxed{

\text{Profit} = (\text{Stock Price at Exercise} - K) - \text{Premium Paid}

}

\]

- **For a Put:**

\[

\boxed{

\text{Profit} = (K - \text{Stock Price at Exercise}) - \text{Premium Paid}

}

\]

- *Where:*

\( \text{Stock Price at Exercise} \) = price of the underlying at the time of exercise or expiration.

- *Rationale:* Calculates the net gain or loss after considering the initial premium paid.

---

**Detailed Step-by-Step Solution:**

**Step 1:** *Why are call options selling for higher prices than put options?*

- Since the current stock price (\$180.50) exceeds the strike price (\$175), the call options are **in the money (ITM)**, possessing intrinsic value, calculated as:

\[

180.50 - 175 = \$5.50

\]

- The put options are **out of the money (OTM)**, with zero intrinsic value:

\[

\max(0, 175 - 180.50) = 0

\]

- The call options' premiums reflect both intrinsic and time value, making them more expensive. The put options, lacking intrinsic value, are priced primarily on time value and market expectations, which are lower under these conditions.

**Supporting Statement:**

The intrinsic value directly influences option prices; in-the-money calls carry inherent value, thus commanding higher premiums, whereas out-of-the-money puts do not. Market expectations and volatility further augment premiums for options with longer durations or higher uncertainty.

---

**Step 2:** *Why does the March call sell for a higher price than the January call?*

- The March expiration date provides a longer time horizon than January, increasing the **time value** of the option.

- Longer duration offers a greater probability that the stock will move further in a favorable direction, which is reflected in a higher premium.

**Supporting Statement:**

The greater time until expiration enhances the chance for profitable movements, increasing the option's total premium. This aligns with fundamental option pricing principles where extended time frames elevate the option's value due to increased uncertainty and potential.

---

**Step 3:** *Would the holder exercise the March call immediately?*

- **Intrinsic value at current stock price:**

\[

180.50 - 175 = \$5.50

\]

- **Premium paid (from data):** \$19.60

- Exercising now yields a profit of:

\[

5.50 - 19.60 = -\$14.10

\]

- Since the premium exceeds the immediate intrinsic value, the option contains significant remaining time value, making early exercise suboptimal.

**Supporting Statement:**

Optimal exercise occurs when the intrinsic value exceeds the remaining time value; here, the premium includes substantial time premium. Exercising early forfeits this time value, leading to net losses. Therefore, holding the option or selling it is more advantageous.

---

**Step 4:** *Calculate profit/loss if the November call is exercised at a stock price of \$190.*

- **Premium paid:** \$11.25

- **Intrinsic value at exercise:**

\[

190 - 175 = \$15.00

\]

- **Profit:**

\[

15.00 - 11.25 = \boxed{\$3.75}

\]

**Supporting Statement:**

Exercising yields an intrinsic gain of \$15, which exceeds the premium paid, resulting in a net profit of \$3.75 per share. This highlights the profitability of exercising in-the-money options at favorable stock prices.

---

**Step 5:** *Calculate profit/loss if the March put is purchased and stock remains at \$180.50.*

- **Premium paid:** \$9.75

- **Intrinsic value at expiration:**

\[

\max(0, 175 - 180.50) = 0

\]

- **Outcome:**

The put expires worthless, and the loss equals the premium paid:

\[

\boxed{\$9.75}

\]

**Supporting Statement:**

Since the stock price exceeds the strike, the put has no intrinsic value, and exercising is not profitable. The entire premium paid is lost, demonstrating the risk of buying out-of-the-money options.

---

**Summary:**

- Call options are priced higher than puts due to their intrinsic value when the stock is above the strike.

- Longer expiration options have higher premiums owing to increased time value.

- Early exercise of a valuable call is generally suboptimal when time value remains.

- Exercising a profitable November call at \$190 yields a net gain of \$3.75 per share.

- The March put results in a loss of \$9.75 if the stock remains at \$180.50.

This comprehensive analysis, grounded in core option valuation principles and supported by precise calculations, enables informed decision-making in options trading.

VIPSolutions focuses on clear, step‑by‑step explanations so you can learn quickly. Whether you need an AI‑generated walkthrough or a short hint to get unstuck, each solution is organized for fast reading and easy review later.

Search similar questions, compare approaches, and bookmark the best answers for revision. Our goal is simple: quick, reliable study help that feels natural—not noisy.

Question 2

Assme the current stock price of Apple (AAPL) is $180.50. The table below shows call and

ot option data various expiration dais

Expiration Strike Gall Price Call Volume Call O1 Put Price Put Volume Put OF

So Hw 0 20 wo 20 ow 0

Nov mw nsw sam ow 0

on mw Gen wsooew ow 510

Mr Tw ww 5 a em 2 an

Answer the following questions:

1) Wh are the call option sling for higher prices than the put. options?

2) Why docs the March cal sel fo higher price than the Jamary call?

3) Suppose you bay the March call. Briefly explain whether you woul evercse i. red

aol.

4) Suppose you buy the November call at th price listed ad axis it when th pros of

Apple sock is $190. What will be your profit o lo?

5) Suppose you buy the Mach put a the pric std, od tho pric of Apple stock remaine

$180.5. What will be your prof o low?

Question 2

Assme the current stock price of Apple (AAPL) is $180.50. The table below shows call and

ot option data various expiration dais

Expiration Strike Gall Price Call Volume Call O1 Put Price Put Volume Put OF

So Hw 0 20 wo 20 ow 0

Nov mw nsw sam ow 0

on mw Gen wsooew ow 510

Mr Tw ww 5 a em 2 an

Answer the following questions:

1) Wh are the call option sling for higher prices than the put. options?

2) Why docs the March cal sel fo higher price than the Jamary call?

3) Suppose you bay the March call. Briefly explain whether you woul evercse i. red

aol.

4) Suppose you buy the November call at th price listed ad axis it when th pros of

Apple sock is $190. What will be your profit o lo?

5) Suppose you buy the Mach put a the pric std, od tho pric of Apple stock remaine

$180.5. What will be your prof o low?