QUESTION 2 (25 Marks) 21 Amachine purchased three years ago for R95 000 is now being sold for R15 000 and will be replaced with a new ‘machine costing R187 500. Delivery of the new machine to the warehouse will incur transportation costs of R16 150, and installation wil cost an additional R6 350. The new machine is expected to generate monthly operational cost savings of R11 900, while the sale of the old machine will increase working capital requirements by R10 950. The ‘company depreciates assets over a five-year period and is subject to a corporate tax rate of 27%. [Yor Newbee Joes | I I) BE I IT Rom ww ww) | ef mew] rw] [sew] 0 Calculate the annual incremental cashfiows of the two machines. (10 marks) 22 KKL Ltd sold goods at R62 000 and offers a 1,75% cash discount when accounts are settled within 30 (5 marks) days. Normal trading terms are 65 days. The current investment rate is 10,5% at a financial institution. Advise, with calculations, whether KKL Ltd should opt for the early settiement of the account, or invest the funds and pay on the due date. 23 Evaluate the feasibility of financing a five-year lease through a loan of R95 000. The loan will be (6 marks) repaid in equal annual payments at the end of each year, with interest charged at 11,25% per annum, ‘compounded annually. Prepare a detailed loan amortisation schedule and provide an interpretation to assess the financial implications of the financing arrangement. Do not round off any values (present all ‘amounts at two decimal places). 24 Jax (Pty) Ltd offers a 65-day credit term to HO (Pty) Ltd. Jax (Pty) Ltd is prepared to allow an 1,65% (4 marks) rebate if the account is settled in 28 days. Calculate the cost to HO (Pty) Ltd of not accepting the discount. The company policy requires the use of 365 days per calendar year.

Question:

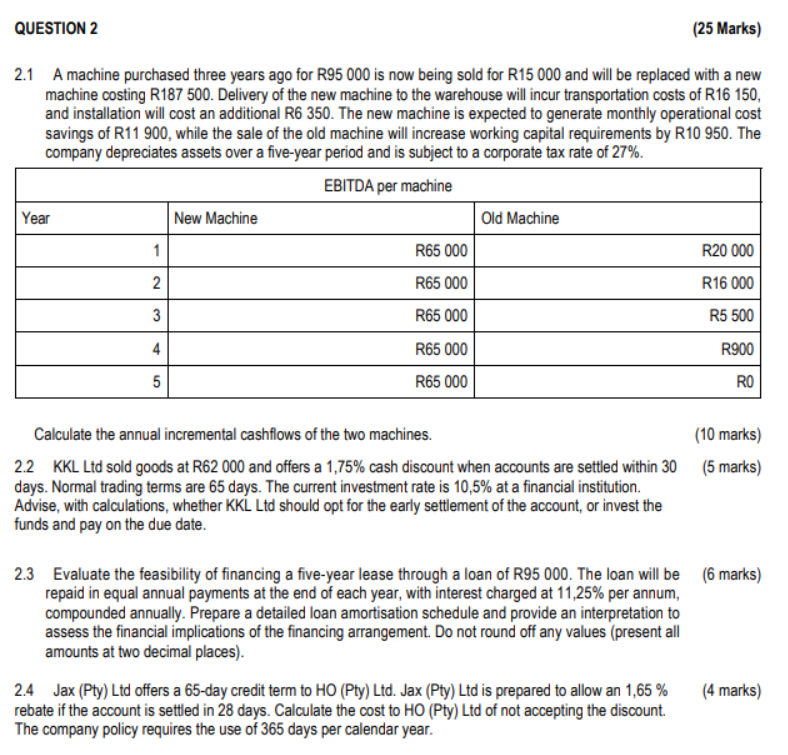

QUESTION 2 (25 Marks)

21 Amachine purchased three years ago for R95 000 is now being sold for R15 000 and will be replaced with a new

‘machine costing R187 500. Delivery of the new machine to the warehouse will incur transportation costs of R16 150,

and installation wil cost an additional R6 350. The new machine is expected to generate monthly operational cost

savings of R11 900, while the sale of the old machine will increase working capital requirements by R10 950. The

‘company depreciates assets over a five-year period and is subject to a corporate tax rate of 27%.

[Yor Newbee Joes |

I I) BE

I IT Rom

ww ww)

| ef mew] rw]

[sew] 0

Calculate the annual incremental cashfiows of the two machines. (10 marks)

22 KKL Ltd sold goods at R62 000 and offers a 1,75% cash discount when accounts are settled within 30 (5 marks)

days. Normal trading terms are 65 days. The current investment rate is 10,5% at a financial institution.

Advise, with calculations, whether KKL Ltd should opt for the early settiement of the account, or invest the

funds and pay on the due date.

23 Evaluate the feasibility of financing a five-year lease through a loan of R95 000. The loan will be (6 marks)

repaid in equal annual payments at the end of each year, with interest charged at 11,25% per annum,

‘compounded annually. Prepare a detailed loan amortisation schedule and provide an interpretation to

assess the financial implications of the financing arrangement. Do not round off any values (present all

‘amounts at two decimal places).

24 Jax (Pty) Ltd offers a 65-day credit term to HO (Pty) Ltd. Jax (Pty) Ltd is prepared to allow an 1,65% (4 marks)

rebate if the account is settled in 28 days. Calculate the cost to HO (Pty) Ltd of not accepting the discount.

The company policy requires the use of 365 days per calendar year.

QUESTION 2 (25 Marks)

21 Amachine purchased three years ago for R95 000 is now being sold for R15 000 and will be replaced with a new

‘machine costing R187 500. Delivery of the new machine to the warehouse will incur transportation costs of R16 150,

and installation wil cost an additional R6 350. The new machine is expected to generate monthly operational cost

savings of R11 900, while the sale of the old machine will increase working capital requirements by R10 950. The

‘company depreciates assets over a five-year period and is subject to a corporate tax rate of 27%.

[Yor Newbee Joes |

I I) BE

I IT Rom

ww ww)

| ef mew] rw]

[sew] 0

Calculate the annual incremental cashfiows of the two machines. (10 marks)

22 KKL Ltd sold goods at R62 000 and offers a 1,75% cash discount when accounts are settled within 30 (5 marks)

days. Normal trading terms are 65 days. The current investment rate is 10,5% at a financial institution.

Advise, with calculations, whether KKL Ltd should opt for the early settiement of the account, or invest the

funds and pay on the due date.

23 Evaluate the feasibility of financing a five-year lease through a loan of R95 000. The loan will be (6 marks)

repaid in equal annual payments at the end of each year, with interest charged at 11,25% per annum,

‘compounded annually. Prepare a detailed loan amortisation schedule and provide an interpretation to

assess the financial implications of the financing arrangement. Do not round off any values (present all

‘amounts at two decimal places).

24 Jax (Pty) Ltd offers a 65-day credit term to HO (Pty) Ltd. Jax (Pty) Ltd is prepared to allow an 1,65% (4 marks)

rebate if the account is settled in 28 days. Calculate the cost to HO (Pty) Ltd of not accepting the discount.

The company policy requires the use of 365 days per calendar year.

Asked by: REDDY BHARGAVA SURYA TEJA

Created at: 2025-11-13 15:45:11

Final Answer:

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :