Return 15% SML 10% 5% 1 2 Beta What is the beta for a portfolio with an expected return of 12.5%?

Question:

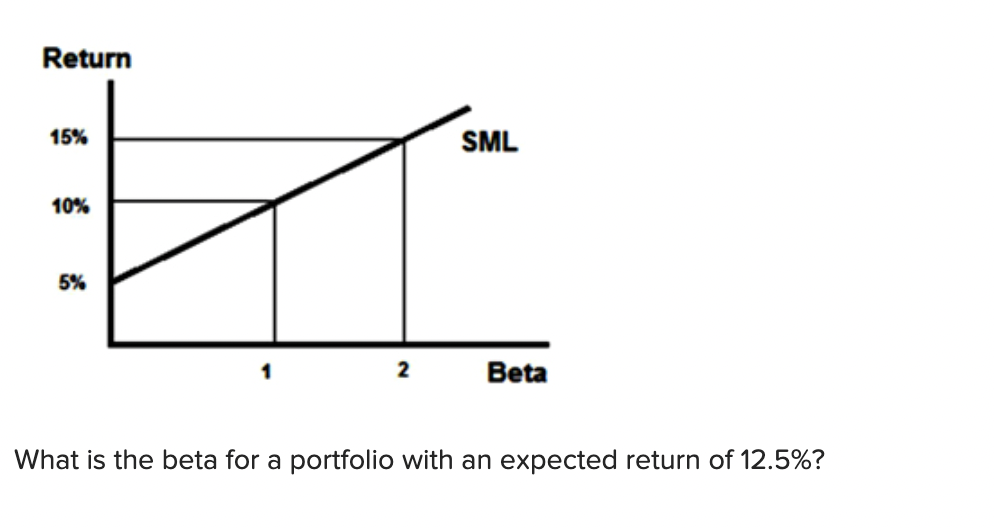

Return

15% SML

10%

5%

1 2 Beta

What is the beta for a portfolio with an expected return of 12.5%?

Return

15% SML

10%

5%

1 2 Beta

What is the beta for a portfolio with an expected return of 12.5%?

This is AI generated Response.

Asked by: Sampangi Swetha

Created at: 2025-06-28 09:26:40

Asked by: Sampangi Swetha

Created at: 2025-06-28 09:26:40

Final Answer:

Rendered

Raw Text

Did you like this answer?

To find the beta for a portfolio with an expected return of **12.5%**, we use the Security Market Line (SML) from the Capital Asset Pricing Model (CAPM):

\[

\text{Expected Return} = R_f + \beta (R_m - R_f)

\]

From the graph:

- The risk-free rate (\( R_f \)) is **5%** (where Beta = 0).

- The market return (\( R_m \)) is **10%** (where Beta = 1).

Plug in the values:

\[

12.5\% = 5\% + \beta (10\% - 5\%)

\]

\[

12.5\% = 5\% + 5\%\beta

\]

\[

12.5\% - 5\% = 5\%\beta

\]

\[

7.5\% = 5\%\beta

\]

\[

\beta = \frac{7.5\%}{5\%} = 1.5

\]

**Answer:**

The beta for a portfolio with an expected return of **12.5%** is **1.5**.

Question:

step by step for chegg eith explanations

This is AI generated Response.

Asked by: Sampangi Swetha

Created at: 2025-06-28 09:27:10

Asked by: Sampangi Swetha

Created at: 2025-06-28 09:27:10

Final Answer:

Rendered

Raw Text

Did you like this answer?

Let's determine the beta for a portfolio with an expected return of 12.5% step by step, using the Security Market Line (SML) from the Capital Asset Pricing Model (CAPM).

**Step 1: Understand the given information**

From the image and the data provided:

- The risk-free rate (\( R_f \)) is **5%** (corresponds to Beta = 0).

- The market return (\( R_m \)) is **10%** (corresponds to Beta = 1).

- The portfolio's expected return is **12.5%**.

**Step 2: Recall the CAPM formula (the Security Market Line equation):**

\[

\text{Expected Return} = R_f + \beta (R_m - R_f)

\]

Where:

- \( R_f \) = risk-free rate

- \( R_m \) = market return

- \( \beta \) = measure of systematic risk

**Step 3: Plug in known values into the formula**

\[

12.5\% = 5\% + \beta (10\% - 5\%)

\]

Simplify the expression inside the parentheses:

\[

12.5\% = 5\% + \beta \times 5\%

\]

**Step 4: Isolate \( \beta \)**

Subtract 5% from both sides:

\[

12.5\% - 5\% = \beta \times 5\%

\]

\[

7.5\% = 5\% \times \beta

\]

**Step 5: Solve for \( \beta \)**

Divide both sides by 5%:

\[

\beta = \frac{7.5\%}{5\%} = \frac{7.5}{5} = 1.5

\]

**Final answer:**

The beta for the portfolio with an expected return of 12.5% is **1.5**.

---

**Summary:**

- The expected return of 12.5% lies above the risk-free rate and the market return, indicating higher risk.

- The calculated beta of 1.5 confirms this higher systematic risk.

- The approach involves plugging known values into the CAPM formula and solving for beta.

Question:

recheck

This is AI generated Response.

Asked by: Sampangi Swetha

Created at: 2025-06-28 09:27:33

Asked by: Sampangi Swetha

Created at: 2025-06-28 09:27:33

Final Answer:

Rendered

Raw Text

Did you like this answer?

Let's carefully recheck the calculation step by step:

**Given Data:**

- Risk-free rate (\( R_f \)) = 5%

- Market return (\( R_m \)) = 10%

- Portfolio expected return (\( R_p \)) = 12.5%

**Step 1: Write the CAPM formula:**

\[

R_p = R_f + \beta (R_m - R_f)

\]

**Step 2: Plug in known values:**

\[

12.5\% = 5\% + \beta (10\% - 5\%)

\]

Simplify:

\[

12.5\% = 5\% + \beta \times 5\%

\]

**Step 3: Isolate \( \beta \):**

Subtract 5% from both sides:

\[

12.5\% - 5\% = \beta \times 5\%

\]

\[

7.5\% = 5\% \times \beta

\]

Divide both sides by 5%:

\[

\beta = \frac{7.5\%}{5\%} = \frac{7.5}{5} = 1.5

\]

**Conclusion:**

The beta corresponding to an expected return of 12.5% is **1.5**.

**Rechecking confirms the initial calculation.**

Question:

calculations are missing

This is AI generated Response.

Asked by: Sampangi Swetha

Created at: 2025-06-28 09:28:13

Asked by: Sampangi Swetha

Created at: 2025-06-28 09:28:13

Final Answer:

Rendered

Raw Text

Did you like this answer?

Let's re-express and verify each step carefully, including the calculations:

---

### Given Data:

- Risk-free rate, \( R_f = 5\% \)

- Market return, \( R_m = 10\% \)

- Portfolio expected return, \( R_p = 12.5\% \)

---

### Step 1: Write the CAPM equation

\[

R_p = R_f + \beta (R_m - R_f)

\]

### Step 2: Plug in the known values

\[

12.5\% = 5\% + \beta (10\% - 5\%)

\]

Calculate the difference \( R_m - R_f \):

\[

10\% - 5\% = 5\%

\]

So,

\[

12.5\% = 5\% + \beta \times 5\%

\]

---

### Step 3: Isolate \( \beta \)

Subtract 5% from both sides:

\[

12.5\% - 5\% = \beta \times 5\%

\]

\[

7.5\% = 5\% \times \beta

\]

---

### Step 4: Solve for \( \beta \)

Divide both sides by 5%:

\[

\beta = \frac{7.5\%}{5\%}

\]

Express percentages as decimals to clarify calculations:

\[

\beta = \frac{0.075}{0.05} = 1.5

\]

---

### **Final Answer:**

**The beta of the portfolio is \(\boxed{1.5}\).**

This indicates the portfolio has 1.5 times the systematic risk compared to the market.

---

### **Summary:**

- The calculation confirms that, given the expected return and the market data, the beta is **1.5**.

- The steps involve plugging the values into the CAPM equation and solving algebraically.

Let me know if you'd like further clarification!

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :