‘The current prices of zero-coupon bonds are in the following table. If the Expectations Hypothesis holds, what is the market's expectation of 2-year spot rate in 3 years from today, Eq[R(3,5)]2 mani ci PY Maturity Date Price 1 year 096 2years 091 dyears 085 dyears 079 Syears 072 In order to hedge their interest rate risk for borrowing beginning 3 months from now, ExxonMobil’s treasury department entered into a 3x5 Forward Rate Agreement (FRA) with Barclays with a notional of $100mm where LIBOR was the reference rate and the forward rate agreement rate was 7%. If in 3 months, 2-month LIBOR decreased to 4.5%, what transfer would take place at the settlement date? I»

Question:

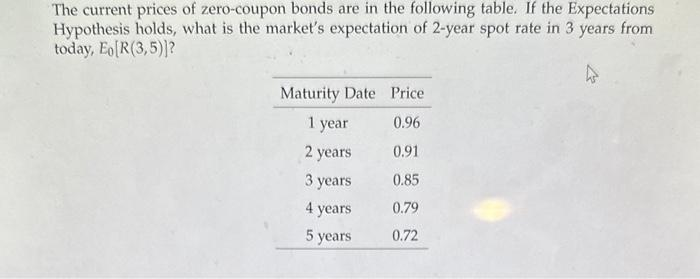

‘The current prices of zero-coupon bonds are in the following table. If the Expectations

Hypothesis holds, what is the market's expectation of 2-year spot rate in 3 years from

today, Eq[R(3,5)]2

mani ci PY

Maturity Date Price

1 year 096

2years 091

dyears 085

dyears 079

Syears 072

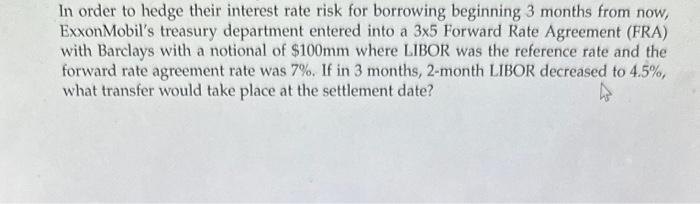

In order to hedge their interest rate risk for borrowing beginning 3 months from now,

ExxonMobil’s treasury department entered into a 3x5 Forward Rate Agreement (FRA)

with Barclays with a notional of $100mm where LIBOR was the reference rate and the

forward rate agreement rate was 7%. If in 3 months, 2-month LIBOR decreased to 4.5%,

what transfer would take place at the settlement date? I»

‘The current prices of zero-coupon bonds are in the following table. If the Expectations

Hypothesis holds, what is the market's expectation of 2-year spot rate in 3 years from

today, Eq[R(3,5)]2

mani ci PY

Maturity Date Price

1 year 096

2years 091

dyears 085

dyears 079

Syears 072

In order to hedge their interest rate risk for borrowing beginning 3 months from now,

ExxonMobil’s treasury department entered into a 3x5 Forward Rate Agreement (FRA)

with Barclays with a notional of $100mm where LIBOR was the reference rate and the

forward rate agreement rate was 7%. If in 3 months, 2-month LIBOR decreased to 4.5%,

what transfer would take place at the settlement date? I»

This is AI generated Response.

Asked by: Sampangi Swetha

Created at: 2025-06-28 10:02:01

Asked by: Sampangi Swetha

Created at: 2025-06-28 10:02:01

Final Answer:

Rendered

Raw Text

Did you like this answer?

Let's solve each question step-by-step:

---

### **Question 1: Expectation of 2-year spot rate in 3 years**

#### **Given Table:**

| Maturity Date | Price |

|:-------------:|:-----:|

| 1 year | 0.96 |

| 2 years | 0.91 |

| 3 years | 0.85 |

| 4 years | 0.79 |

| 5 years | 0.72 |

We are to find the market's expectation of the **2-year spot rate in 3 years** (i.e., the forward rate from year 3 to year 5).

#### **Step 1: Find the forward rate \( f_{3,5} \)**

The formula for the forward rate from \( t_1 \) to \( t_2 \) is:

\[

f_{t_1, t_2} = \left( \frac{P(0,t_1)}{P(0,t_2)} \right)^{1/(t_2-t_1)} - 1

\]

Where \( P(0,t) \) is the price of a zero-coupon bond maturing at \( t \) years.

So for 3 to 5 years:

\[

f_{3,5} = \left( \frac{P(0,3)}{P(0,5)} \right)^{1/2} - 1

\]

Given:

- \( P(0,3) = 0.85 \)

- \( P(0,5) = 0.72 \)

\[

f_{3,5} = \left( \frac{0.85}{0.72} \right)^{1/2} - 1

\]

\[

f_{3,5} = (1.1806)^{0.5} - 1

\]

\[

f_{3,5} = 1.0865 - 1 = 0.0865 \text{ or } 8.65\%

\]

**Final Answer:**

\[

\boxed{8.65\%}

\]

---

### **Question 2: 3x5 FRA Settlement Value**

#### **Given:**

- Notional: $100,000,000

- FRA Rate (\( K \)): 7%

- Actual 2-month LIBOR after 3 months (\( R \)): 4.5%

- FRA Period: 2 months (from 3 months to 5 months)

- Settlement in 3 months (so discounting is needed for the settlement amount)

#### **FRA Settlement Formula:**

The value of the FRA to the borrower at settlement (time \( t \)) is:

\[

\text{Settlement Amount} = \frac{(R - K) \times \text{Notional} \times \frac{\Delta t}{360}}{1 + R \times \frac{\Delta t}{360}}

\]

Where:

- \( R \) = Actual LIBOR (4.5% or 0.045)

- \( K \) = FRA Rate (7% or 0.07)

- \( \Delta t \) = 60 days (2 months), or \( \frac{2}{12} = 0.1667 \) years (but conventionally 60/360 = 1/6)

Plug in the values:

\[

\text{Settlement Amount} = \frac{(0.045 - 0.07) \times 100,000,000 \times \frac{60}{360}}{1 + 0.045 \times \frac{60}{360}}

\]

\[

= \frac{(-0.025) \times 100,000,000 \times \frac{1}{6}}{1 + 0.0075}

\]

\[

= \frac{(-0.025) \times 16,666,667}{1.0075}

\]

\[

= \frac{-416,666.67}{1.0075}

\]

\[

= -413,567.16

\]

**Interpretation:**

- Since the actual LIBOR is less than the FRA rate, **ExxonMobil receives $413,567.16 from Barclays** at settlement.

---

## **Summary:**

1. **Forward 2-year spot rate in 3 years:** **8.65%**

2. **FRA settlement amount:** **ExxonMobil receives $413,567.16 from Barclays**

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :