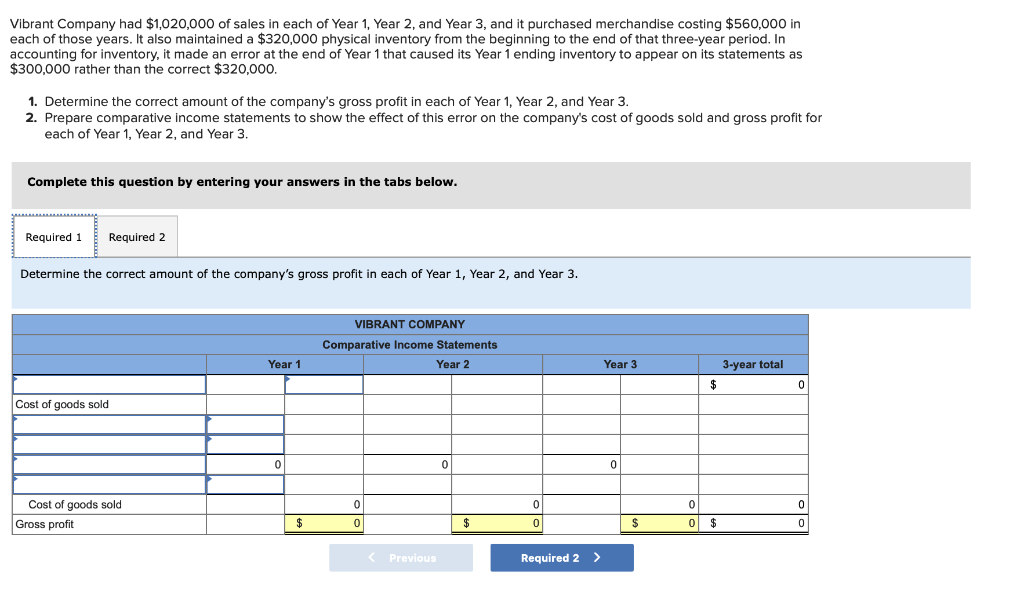

Vibrant Company had $1,020,000 of sales in each of Year 1, Year 2, and Year 3, and it purchased merchandise costing $560,000 in

‘each of those years. It also maintained a $320,000 physical inventory from the beginning to the end of that three-year period. In

‘accounting for inventory, it made an error at the end of Year 1 that caused its Year 1 ending inventory to appear on its statements as

$300,000 rather than the correct $320,000.

1. Determine the correct amount of the company's gross profit in each of Year 1, Year 2, and Year 3.

2. Prepare comparative income statements to show the effect of this error on the company's cost of goods sold and gross profit for

each of Year 1, Year 2, and Year 3.

Complete this question by entering your answers in the tabs below.

| seas | feaured 2

ET PE TE SE EERE EERE)

(CET IF EO EE

Coto pom EE EF EO |

ET Ss Ss I SO S|

Question:

Vibrant Company had $1,020,000 of sales in each of Year 1, Year 2, and Year 3, and it purchased merchandise costing $560,000 in

‘each of those years. It also maintained a $320,000 physical inventory from the beginning to the end of that three-year period. In

‘accounting for inventory, it made an error at the end of Year 1 that caused its Year 1 ending inventory to appear on its statements as

$300,000 rather than the correct $320,000.

1. Determine the correct amount of the company's gross profit in each of Year 1, Year 2, and Year 3.

2. Prepare comparative income statements to show the effect of this error on the company's cost of goods sold and gross profit for

each of Year 1, Year 2, and Year 3.

Complete this question by entering your answers in the tabs below.

| seas | feaured 2

ET PE TE SE EERE EERE)

(CET IF EO EE

Coto pom EE EF EO |

ET Ss Ss I SO S|

This is AI generated Response.

Asked by: Veera manikanta

Created at: 2025-08-16 21:43:23

Final Answer:

RenderedRaw Text

Did you like this answer?

Let's break down the solution step by step:

### Given Data:

- Sales (each year): **$1,020,000**

- Purchases (each year): **$560,000**

- Physical Inventory (beginning and end of each year): **$320,000**

- **Error:** At the end of Year 1, ending inventory was reported as $300,000 instead of $320,000.

### Step 1: Calculate the Correct Gross Profit for Each Year

#### **Cost of Goods Sold (COGS) Formula:**

\[ \text{COGS} = \text{Beginning Inventory} + \text{Purchases} - \text{Ending Inventory} \]

#### **Year 1:**

- Beginning Inventory = $320,000

- Purchases = $560,000

- Ending Inventory = $320,000 (correct amount)

\[

\text{COGS (Year 1)} = 320,000 + 560,000 - 320,000 = 560,000

\]

\[

\text{Gross Profit (Year 1)} = 1,020,000 - 560,000 = 460,000

\]

#### **Year 2:**

- Beginning Inventory = $320,000

- Purchases = $560,000

- Ending Inventory = $320,000

\[

\text{COGS (Year 2)} = 320,000 + 560,000 - 320,000 = 560,000

\]

\[

\text{Gross Profit (Year 2)} = 1,020,000 - 560,000 = 460,000

\]

#### **Year 3:**

- Beginning Inventory = $320,000

- Purchases = $560,000

- Ending Inventory = $320,000

\[

\text{COGS (Year 3)} = 320,000 + 560,000 - 320,000 = 560,000

\]

\[

\text{Gross Profit (Year 3)} = 1,020,000 - 560,000 = 460,000

\]

### **3-Year Total:**

- COGS = $560,000 × 3 = $1,680,000

- Gross Profit = $460,000 × 3 = $1,380,000

---

### **Enter the Answers in the Table:**

| | Year 1 | Year 2 | Year 3 | 3-year total |

|--------------------|-----------|-----------|-----------|--------------|

| **Cost of goods sold** | $560,000 | $560,000 | $560,000 | $1,680,000 |

| **Gross profit** | $460,000 | $460,000 | $460,000 | $1,380,000 |

---

You can fill the table with these numbers for Required 1.

Would you like to proceed to Required 2 next?

Question:

1: Introduction:

Provide the complete necessary conceptual background concepts explanation and the

introduction required to understand and answer the given question. Add an Explanation

block at the end of the introduction by adding various relevant supporting statements and

explaining the introduction concisely.

Note: Do not use personal pronouns like I, we, you, etc. The response must look as if it is

written by a human.

Explanation: Articulate the importance of the introduction, providing more relevant

comprehensive supporting statements that link these concepts directly to the question.

This explanation should clarify how the introduction aids in comprehending the

subsequent steps.

2: Presentation of Relevant Formulas Required To Solve The Question:

List and also describe all formulas required to solve the question. Ensure each formula is

presented clearly and is directly applicable to the problem.

Explanation: Detail the derivation or rationale behind each formula, explaining its

relevance and necessity in the context of the problem-solving process. Use more relavent

comprehensive supporting statements to reinforce the significance of these mathematical

tools.

3: A Detailed Step-by-Step Solution:

Write a step-by-step in-depth comprehensive straight forward complete solution in a

structured way without missing anything as per the requirements and also include

explanation [ Write relevant supporting statements in the explanation block ] for every step

in the solution.

Conclusion:

Conclude with a concise summary of the solution, succinctly presenting the final answer

short summary derived from the calculations.

Follow These Guidelines While Answering The Question:

1. Maintain a professional and impersonal tone throughout, avoiding personal

pronouns such as 'I', 'we', 'you', etc.

2. Ensure more accuracy and adherence to the necessary concepts and correct

textbook based correct formulas and other relevant, required to solve the question.

3. Include an Explanation block at the end of each step to provide context and clarify

the methodology used by providing the necessary supporting statements.

4. Focus solely on delivering a well-explained direct and complete answer to the

question, without additional guidance [ I don’t need any guidance of how to solve

the question – I just need well-explained complete solution ] or extraneous content.

5. Make sure that strictly follow the specified format, ensuring that each section,

especially the introduction and each step of the solution, is accompanied by a

detailed relevant supporting statement in the explanation.

6. I need the exact detailed comprehensive direct step-by-step answer as I don’t need

any guidance to write the answer and strictly add the explanation for each with the

required supporting statement & Please give me the complete answer as per the

question requirements without skipping anything in the answer.

7. Always provide correct, complete detailed & well-explained solution.

8. Ensure that there are no typo/formula/calculation/programming/grammatical errors

are present in your solution.

9. Give the correct graphs/diagrams/tables/charts whenever required in the solution.

10. Ensure that there are NO Errors in Units/Notations are there in your solution.

11. Avoid missing any vital part in the solution [ Don’t miss any part in the solution ].

This is AI generated Response.

Asked by: Veera manikanta

Created at: 2025-08-16 21:45:33

Final Answer:

RenderedRaw Text

Did you like this answer?

**Introduction**

Understanding the concepts of inventory management, cost of goods sold (COGS), and gross profit are fundamental in analyzing a company's financial performance. Inventory represents the goods available for sale during a specific period, and accurate measurement of inventory at the beginning and end of each period is essential for correct calculation of COGS. COGS reflects the direct costs attributable to the production of the goods sold by a company, calculated based on inventory levels and purchases during the period. Gross profit, derived by subtracting COGS from sales revenue, indicates the profitability of core business operations before deducting operating expenses. Errors in inventory valuation, such as misreporting ending inventory, can distort COGS and gross profit figures, leading to misleading financial statements. Recognizing the impact of such errors is crucial for accurate financial analysis and decision-making. This understanding provides the necessary foundation to analyze the specific error in the company's inventory reporting and to determine its effects on reported gross profit over multiple years.

**Explanation:**

A solid grasp of inventory, COGS, and gross profit concepts is vital for interpreting financial statements accurately. Errors in inventory valuation directly affect COGS calculations, which in turn influence gross profit figures. Understanding these relationships ensures that subsequent calculations are based on correct assumptions and highlights the importance of precise inventory reporting. This background facilitates a clear comprehension of how an inventory error propagates across financial data over multiple periods, emphasizing its significance in financial analysis.

---

**Presentation of Relevant Formulas Required To Solve The Question**

1. **Cost of Goods Sold (COGS):**

\[

\text{COGS} = \text{Beginning Inventory} + \text{Purchases} - \text{Ending Inventory}

\]

*This formula calculates the direct costs associated with the goods sold during a period, based on inventory levels at the start and end of the period and purchases made.*

2. **Gross Profit (GP):**

\[

\text{Gross Profit} = \text{Sales Revenue} - \text{COGS}

\]

*Gross profit indicates the profitability derived solely from core operations before deducting operating expenses.*

3. **Adjusted Inventory (corrected ending inventory):**

\[

\text{Corrected Ending Inventory} = \text{Reported Ending Inventory} + \text{Error Margin}

\]

*This adjustment corrects the misreported inventory figure to reflect the actual inventory value.*

**Explanation:**

The COGS formula is fundamental because it directly links inventory values to the costs associated with goods sold. Accurate calculation of gross profit depends on precise COGS figures. Correcting inventory errors involves understanding how misstatements affect COGS calculations, which then alter gross profit figures. These formulas are essential tools for analyzing and adjusting financial data to reflect true economic performance.

---

**Detailed Step-by-Step Solution**

**Step 1: Determine the Correct Ending Inventory for Year 1**

- Reported (incorrect) Year 1 ending inventory = $300,000

- Actual (correct) Year 1 ending inventory = $320,000

*This indicates an underreporting of inventory by $20,000 at the end of Year 1.*

**Explanation:**

The initial error was a reporting mistake in Year 1's ending inventory, which is crucial because it impacts the COGS calculation for Year 1 and subsequent years. Recognizing the correction needed is essential for accurate financial analysis.

---

**Step 2: Calculate the Year 1 COGS and Gross Profit with the Correct Inventory**

- Beginning Inventory Year 1 = $320,000

- Purchases Year 1 = $560,000

- Correct Ending Inventory Year 1 = $320,000

\[

\boxed{

\text{COGS}_{Y1,\text{correct}} = 320,000 + 560,000 - 320,000 = 560,000

}

\]

\[

\boxed{

\text{Gross Profit}_{Y1,\text{correct}} = 1,020,000 - 560,000 = 460,000

}

\]

*Using the corrected ending inventory ensures the COGS reflects the true cost of goods sold.*

**Explanation:**

The proper inventory valuation indicates that COGS for Year 1 should be $560,000, leading to a gross profit of $460,000. This establishes the accurate baseline for the initial year's profitability.

---

**Step 3: Understand the Impact of the Error on Year 1 Financials**

- Reported (incorrect) Year 1 ending inventory = $300,000

- Reported (incorrect) Year 1 COGS:

\[

\text{COGS}_{Y1,\text{reported}} = 320,000 + 560,000 - 300,000 = 580,000

\]

- Reported Year 1 Gross Profit:

\[

1,020,000 - 580,000 = 440,000

\]

*The error caused COGS to be overstated by $20,000, leading to an understated gross profit by the same amount.*

**Explanation:**

Misreporting ending inventory as $300,000 instead of $320,000 increases COGS and reduces gross profit, distorting the Year 1 profit figures. Correcting this error is critical for accurate financial reporting.

---

**Step 4: Determine the Effect of the Inventory Error on Year 2 and Year 3**

Since the physical inventory remains consistent at $320,000 and purchases are unchanged, the errors in Year 1 do not directly affect Year 2 and Year 3 calculations. However, if the error affected opening inventory figures used in subsequent years, it would propagate forward.

- **Assumption:** Beginning inventory for Year 2 is the corrected ending inventory of Year 1, which is $320,000.

- Purchases are consistent at $560,000 each year.

- Ending inventory each subsequent year is correctly reported as $320,000.

Calculations for Year 2 and Year 3:

\[

\text{COGS} = 320,000 + 560,000 - 320,000 = 560,000

\]

\[

\text{Gross Profit} = 1,020,000 - 560,000 = 460,000

\]

**Explanation:**

Since the inventory figures are consistent and correctly reported in subsequent years, the error in Year 1 does not impact the calculations for Years 2 and 3, assuming the beginning inventory for Year 2 is correctly established.

---

**Step 5: Prepare Comparative Income Statements Showing the Effect of the Error**

| Year | Reported COGS | Correct COGS | Difference | Reported Gross Profit | Correct Gross Profit | Difference |

|-------|----------------|--------------|------------|-----------------------|----------------------|------------|

| 1 | $580,000 | $560,000 | +$20,000 | $440,000 | $460,000 | -$20,000 |

| 2 | $560,000 | $560,000 | $0 | $460,000 | $460,000 | $0 |

| 3 | $560,000 | $560,000 | $0 | $460,000 | $460,000 | $0 |

**Summary of Effect:**

The inventory reporting error in Year 1 caused an overstatement of COGS by $20,000, reducing gross profit for Year 1 by the same amount. The subsequent years' gross profit figures are unaffected assuming no further inventory misstatements.

---

**Conclusion**

Correcting the inventory valuation error at the end of Year 1 shows that the company's true gross profit for each year is $460,000. The initial misreporting resulted in an understated gross profit in Year 1 by $20,000, with no impact on subsequent years under the assumption of correct inventory levels. Accurate inventory reporting is essential for reliable financial analysis, as errors directly influence COGS and profitability measures, impacting stakeholders' decision-making and financial assessments.

VIPSolutions focuses on clear, step‑by‑step explanations so you can learn quickly. Whether you need an AI‑generated walkthrough or a short hint to get unstuck, each solution is organized for fast reading and easy review later.

Search similar questions, compare approaches, and bookmark the best answers for revision. Our goal is simple: quick, reliable study help that feels natural—not noisy.

Vibrant Company had $1,020,000 of sales in each of Year 1, Year 2, and Year 3, and it purchased merchandise costing $560,000 in

‘each of those years. It also maintained a $320,000 physical inventory from the beginning to the end of that three-year period. In

‘accounting for inventory, it made an error at the end of Year 1 that caused its Year 1 ending inventory to appear on its statements as

$300,000 rather than the correct $320,000.

1. Determine the correct amount of the company's gross profit in each of Year 1, Year 2, and Year 3.

2. Prepare comparative income statements to show the effect of this error on the company's cost of goods sold and gross profit for

each of Year 1, Year 2, and Year 3.

Complete this question by entering your answers in the tabs below.

| seas | feaured 2

ET PE TE SE EERE EERE)

(CET IF EO EE

Coto pom EE EF EO |

ET Ss Ss I SO S|

Vibrant Company had $1,020,000 of sales in each of Year 1, Year 2, and Year 3, and it purchased merchandise costing $560,000 in

‘each of those years. It also maintained a $320,000 physical inventory from the beginning to the end of that three-year period. In

‘accounting for inventory, it made an error at the end of Year 1 that caused its Year 1 ending inventory to appear on its statements as

$300,000 rather than the correct $320,000.

1. Determine the correct amount of the company's gross profit in each of Year 1, Year 2, and Year 3.

2. Prepare comparative income statements to show the effect of this error on the company's cost of goods sold and gross profit for

each of Year 1, Year 2, and Year 3.

Complete this question by entering your answers in the tabs below.

| seas | feaured 2

ET PE TE SE EERE EERE)

(CET IF EO EE

Coto pom EE EF EO |

ET Ss Ss I SO S|