4)Calculation Based MCQ Question’s Prompt: 1: Introduction: Provide the necessary conceptual background and introduction required to understand and answer the given question. Add an Explanation block at the end of the introduction by adding various relevant supporting statements and explaining the introduction concisely. Note: Do not use personal pronouns like I, we, you, etc. The response must look as if it is written by a human. Explanation: Clearly elucidate the introductory concepts, with more relevant comprehensive supporting the narrative with necessary statements that establish the context and relevance of the concepts in answering the question. 2: Identifying the Correct Option Among The Choices: Identify the correct choice from the provided options. Explanation: Provide a comprehensive justification for why this option is correct. Enhance the explanation with detailed reasoning, incorporating relevant concepts, theories, or formulas as necessary. A Step-by-Step Calculation: Write a step-by-step in-depth comprehensive straight forward complete solution in a structured way without missing anything as per the requirements and also include explanation [ Write relevant supporting statements in the explanation block ] for every step in the solution. Explanation: Break down the calculation process into clear, logical steps. Each step should be accompanied by an explanation that justifies the operations performed and the intermediate results obtained. 3: Analysis of why other Options are Incorrect: List the options that are incorrect. Explanation: Offer a detailed analysis as to why each of these options does not satisfy the question's requirements. Support each explanation with logical reasoning or conceptual discrepancies. Conclusion: Conclude with a brief yet complete summary of the answer, encapsulating the main points addressed and the solution's effectiveness. Follow These Guidelines While Answering The Question: 1. Maintain a professional and impersonal tone throughout, avoiding personal pronouns such as 'I', 'we', 'you', etc. 2. Ensure more accuracy and adherence to the necessary concepts and correct textbook based correct formulas and other relevant, required to solve the question. 3. Include an Explanation block at the end of each step to provide context and clarify the methodology used by providing the necessary supporting statements. 4. Focus solely on delivering a well-explained direct and complete answer to the question, without additional guidance [ I don’t need any guidance of how to solve the question – I just need well-explained complete solution ] or extraneous content. 5. Make sure that strictly follow the specified format, ensuring that each section, especially the introduction and each step of the solution, is accompanied by a detailed relevant supporting statement in the explanation. 6. I need the exact detailed comprehensive direct step-by-step answer as I don’t need any guidance to write the answer and strictly add the explanation for each with the required supporting statement & Please give me the complete answer as per the question requirements without skipping anything in the answer. 7. Always provide correct, complete detailed & well-explained solution. 8. Ensure that there are no typo/formula/calculation/programming/grammatical errors are present in your solution. 9. Give the correct graphs/diagrams/tables/charts whenever required in the solution. 10. Ensure that there are NO Errors in Units/Notations are there in your solution. 11. Avoid missing any vital part in the solution [ Don’t miss any part in the solution ].You are given the following information about a portfolio you are to manage. For the long term, you are bullish, but you think the market may fall over the next month Portfolio Value $ 1 million Portfolio's Beta 0.60 Current S&P500 Value 1400 Anticipated S&P500 Value 1200 | For a 200-point drop in the S&P 500, by how much does the value of the futures position change?

Question:

4)Calculation Based MCQ Question’s Prompt:

1: Introduction:

Provide the necessary conceptual background and introduction required to understand

and answer the given question. Add an Explanation block at the end of the introduction by

adding various relevant supporting statements and explaining the introduction concisely.

Note: Do not use personal pronouns like I, we, you, etc. The response must look as if it is

written by a human.

Explanation: Clearly elucidate the introductory concepts, with more relevant

comprehensive supporting the narrative with necessary statements that establish the

context and relevance of the concepts in answering the question.

2: Identifying the Correct Option Among The Choices:

Identify the correct choice from the provided options.

Explanation: Provide a comprehensive justification for why this option is correct. Enhance

the explanation with detailed reasoning, incorporating relevant concepts, theories, or

formulas as necessary.

A Step-by-Step Calculation:

Write a step-by-step in-depth comprehensive straight forward complete solution in a

structured way without missing anything as per the requirements and also include

explanation [ Write relevant supporting statements in the explanation block ] for every step

in the solution.

Explanation: Break down the calculation process into clear, logical steps. Each step

should be accompanied by an explanation that justifies the operations performed and the

intermediate results obtained.

3: Analysis of why other Options are Incorrect:

List the options that are incorrect.

Explanation: Offer a detailed analysis as to why each of these options does not satisfy the

question's requirements. Support each explanation with logical reasoning or conceptual

discrepancies.

Conclusion:

Conclude with a brief yet complete summary of the answer, encapsulating the main points

addressed and the solution's effectiveness.

Follow These Guidelines While Answering The Question:

1. Maintain a professional and impersonal tone throughout, avoiding personal

pronouns such as 'I', 'we', 'you', etc.

2. Ensure more accuracy and adherence to the necessary concepts and correct

textbook based correct formulas and other relevant, required to solve the question.

3. Include an Explanation block at the end of each step to provide context and clarify

the methodology used by providing the necessary supporting statements.

4. Focus solely on delivering a well-explained direct and complete answer to the

question, without additional guidance [ I don’t need any guidance of how to solve

the question – I just need well-explained complete solution ] or extraneous content.

5. Make sure that strictly follow the specified format, ensuring that each section,

especially the introduction and each step of the solution, is accompanied by a

detailed relevant supporting statement in the explanation.

6. I need the exact detailed comprehensive direct step-by-step answer as I don’t need

any guidance to write the answer and strictly add the explanation for each with the

required supporting statement & Please give me the complete answer as per the

question requirements without skipping anything in the answer.

7. Always provide correct, complete detailed & well-explained solution.

8. Ensure that there are no typo/formula/calculation/programming/grammatical errors

are present in your solution.

9. Give the correct graphs/diagrams/tables/charts whenever required in the solution.

10. Ensure that there are NO Errors in Units/Notations are there in your solution.

11. Avoid missing any vital part in the solution [ Don’t miss any part in the solution ]. You are given the following information about a portfolio you are to manage. For the long term, you are bullish, but you think

the market may fall over the next month

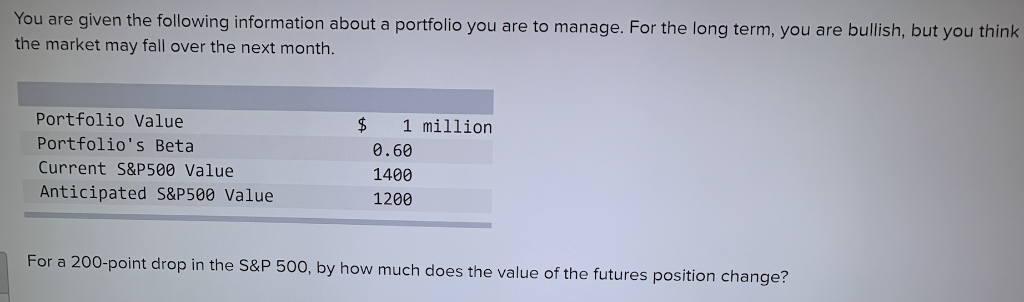

Portfolio Value $ 1 million

Portfolio's Beta 0.60

Current S&P500 Value 1400

Anticipated S&P500 Value 1200

| For a 200-point drop in the S&P 500, by how much does the value of the futures position change?

You are given the following information about a portfolio you are to manage. For the long term, you are bullish, but you think

the market may fall over the next month

Portfolio Value $ 1 million

Portfolio's Beta 0.60

Current S&P500 Value 1400

Anticipated S&P500 Value 1200

| For a 200-point drop in the S&P 500, by how much does the value of the futures position change?

Asked by: Boreddy Mahendra

Created at: 2025-06-28 11:47:44

Final Answer:

Question:

2)Updated Calculations Question Prompt: 1: Introduction: Provide the complete necessary conceptual background concepts explanation and the introduction required to understand and answer the given question. Add an Explanation block at the end of the introduction by adding various relevant supporting statements and explaining the introduction concisely. Note: Do not use personal pronouns like I, we, you, etc. The response must look as if it is written by a human. Explanation: Articulate the importance of the introduction, providing more relevant comprehensive supporting statements that link these concepts directly to the question. This explanation should clarify how the introduction aids in comprehending the subsequent steps. 2: Presentation of Relevant Formulas Required To Solve The Question: List and also describe all formulas required to solve the question. Ensure each formula is presented clearly and is directly applicable to the problem. Explanation: Detail the derivation or rationale behind each formula, explaining its relevance and necessity in the context of the problem-solving process. Use more relavent comprehensive supporting statements to reinforce the significance of these mathematical tools. 3: A Detailed Step-by-Step Solution: Write a step-by-step in-depth comprehensive straight forward complete solution in a structured way without missing anything as per the requirements and also include explanation [ Write relevant supporting statements in the explanation block ] for every step in the solution. Conclusion: Conclude with a concise summary of the solution, succinctly presenting the final answer short summary derived from the calculations. Follow These Guidelines While Answering The Question: 1. Maintain a professional and impersonal tone throughout, avoiding personal pronouns such as 'I', 'we', 'you', etc. 2. Ensure more accuracy and adherence to the necessary concepts and correct textbook based correct formulas and other relevant, required to solve the question. 3. Include an Explanation block at the end of each step to provide context and clarify the methodology used by providing the necessary supporting statements. 4. Focus solely on delivering a well-explained direct and complete answer to the question, without additional guidance [ I don’t need any guidance of how to solve the question – I just need well-explained complete solution ] or extraneous content. 5. Make sure that strictly follow the specified format, ensuring that each section, especially the introduction and each step of the solution, is accompanied by a detailed relevant supporting statement in the explanation. 6. I need the exact detailed comprehensive direct step-by-step answer as I don’t need any guidance to write the answer and strictly add the explanation for each with the required supporting statement & Please give me the complete answer as per the question requirements without skipping anything in the answer. 7. Always provide correct, complete detailed & well-explained solution. 8. Ensure that there are no typo/formula/calculation/programming/grammatical errors are present in your solution. 9. Give the correct graphs/diagrams/tables/charts whenever required in the solution. 10. Ensure that there are NO Errors in Units/Notations are there in your solution. 11. Avoid missing any vital part in the solution [ Don’t miss any part in the solution ].

Asked by: Boreddy Mahendra

Created at: 2025-06-28 11:48:41

Final Answer:

Question:

### 1. **Introduction:** In financial portfolio management, **systematic risk**, also referred to as **market risk**, is often measured using a metric called **beta**. Beta quantifies a portfolio's sensitivity to movements in the market index, such as the **S\&P 500**. A beta of 1 indicates that the portfolio's value moves in line with the market, whereas a beta less than 1 suggests reduced volatility relative to the market. When a market downturn is anticipated, investors often use **futures contracts** to hedge against potential losses in their portfolios. The value of these futures positions adjusts inversely to the changes in the underlying market index, providing an effective means of risk mitigation. In the context of a predicted **200-point drop** in the S\&P 500, it becomes critical to evaluate how much the **value of a hedging futures position** would change in response to such a market movement. This allows portfolio managers to quantify the hedge effectiveness and the extent of financial protection provided against anticipated losses. #### **Explanation:** Understanding beta and its application in market risk estimation is essential in portfolio risk management. Futures contracts serve as financial instruments that can be utilized to hedge against adverse market movements. When the market is expected to decline, futures are typically shorted, and the gain from the drop in index value offsets the portfolio losses. This introduction builds the foundation for determining how the change in the market translates into changes in portfolio value and how much compensation a futures position must provide to hedge that loss accurately. These foundational concepts ensure clarity in the subsequent steps of computation. --- ### 2. **Presentation of Relevant Formulas Required To Solve The Question:** To compute the change in the value of the futures position, the following formulas are required: #### **Formula 1: Percentage Change in the Index** $$ \text{Percentage Change in Index} = \frac{\text{Anticipated Index Value} - \text{Current Index Value}}{\text{Current Index Value}} \times 100 $$ #### **Formula 2: Portfolio Value Change Due to Beta Exposure** $$ \text{Change in Portfolio Value} = \text{Portfolio Beta} \times \text{Percentage Change in Index} \times \text{Portfolio Value} $$ --- #### **Explanation:** * **Formula 1** calculates how much the market is expected to decline in percentage terms, which serves as the basis for evaluating the portfolio's response. * **Formula 2** incorporates the portfolio's beta to estimate how sensitive the portfolio is to market fluctuations. Multiplying this adjusted percentage change by the total portfolio value quantifies the expected financial impact of the market decline. * These formulas are essential because they establish a direct link between market movements and portfolio performance. By applying these relationships, the value change in a hedging futures position needed to counteract portfolio losses can be determined accurately. --- ### 3. **A Detailed Step-by-Step Solution:** **Step 1: Compute the Percentage Change in the S\&P 500 Index** $$ \text{Percentage Change} = \frac{1200 - 1400}{1400} \times 100 = \frac{-200}{1400} \times 100 = -14.2857\% $$ #### **Explanation:** The index is expected to fall from 1400 to 1200, resulting in a 200-point drop. The formula translates this absolute change into a percentage to standardize it for beta-based application across different portfolio sizes and market levels. --- **Step 2: Compute the Expected Change in Portfolio Value** $$ \text{Change in Portfolio Value} = 0.60 \times (-14.2857\%) \times \$1{,}000{,}000 $$ $$ = -0.085714 \times \$1{,}000{,}000 = -\$85{,}714.29 $$ #### **Explanation:** Applying the portfolio's beta adjusts the raw market change to reflect the portfolio’s specific sensitivity. The result quantifies the expected decline in the portfolio's market value due to the anticipated market downturn. --- **Step 3: Interpret the Change in Futures Position Value** Since the question asks: **"For a 200-point drop in the S\&P 500, by how much does the value of the futures position change?"** Assuming the futures are used to hedge against the loss, the change in the value of the futures position will mirror the portfolio loss in magnitude but with an opposite sign: $$ \text{Change in Futures Value} = +\$85{,}714.29 $$ #### **Explanation:** The futures position gains value as the market drops, offsetting the portfolio loss. This step completes the hedge analysis by equating the loss from the equity portfolio to the gain from the futures position. It reflects proper risk management application and confirms that the hedging strategy is appropriately calibrated. --- ### **Conclusion:** The anticipated **200-point decline** in the S\&P 500 index results in a **14.29%** drop in the index. Given the portfolio's **beta of 0.60** and value of **\$1,000,000**, the portfolio is expected to lose **\$85,714.29** in value. Consequently, the value of the futures position changes by **+\$85,714.29**, thereby offsetting the loss and serving as an effective hedge.

Asked by: Boreddy Mahendra

Created at: 2025-06-28 11:50:25

Final Answer:

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :