Act like a helpful tutor and exlain Give step-by-step solution with explanation and final answer:EEE Er EN es FET LT gr TTI Chee meme Below are the project financial estimates. Investment Plan: ECT a bam Sa le Ee [EA A BR CA Be ee All figures in CAD'000 (Thousands). TT ee es Ee] I I Eee Working capital required {Zo [sss las [a3 [ams fase] [ewstomense ———— 1 [ow [oa [ma [we Ta] Production Plan: i Revenue: hil Ori Price or cae] EI HN 1 3 om Xo 2 Production Quantity (000 | Te76 [610 | [o45 [eds Teio | lover masons rE TTT JST ie 1.Unit Material Cost percase) | [$100 | [$1.00 [$1.00 Labour 1,013 [11215 [1485 1,485 Overhead (incremental cash flow) 405 473 473 || [473 These figures are based on current (year 0) prices. Neither inflation nor capital allowances on the equipment have been reflected yet. The following additional data also apply to the project. All cash flows are assumed to occur at the end of the year, (1) Selling prices, working capital, and cost of materials increase with inflation by 5% each year over the prior year. (2) Labour costs and overhead expenses (assumed all incremental cash flow) increase by 15% each year over the prior year. I (8) For tax purposes, Capital Cost Allowances (CCA) will be available against the taxable profits of the project, at a CCA rate of 20% a year (half-year rule applies). The first claim will start in Year 1. Cash flow from tax savings will materialise in the same year when allowances are claimed. Any unclaimed allowance at the end of 5 years will be forfeited. (4) The corporate tax rate is 309%, and payment is due one year in arrears. (5) The equipment will have a zero salvage value at the end of the. project's life. (6) The company's real after-tax weighted average cost of capital is estimated to be 15%, and its nominal after-tax weighted average cost of capital is 20%. Mr. Maxims has no idea about project risk. He assumed the project risk to be the same as the overall risk of the company. Holiday Group, Inc. (“The Group”) is a Canadian hotel group that has operated for over 30 years. =| The Group owns and manages five hotels across Alberta: Traveler's Inn, Holiday Lodge, Resort : Alpha, Resort Beta, and Hotel Charles. Currently, all soft drinks and beverages served in guestrooms and hotel restaurants are purchased from regional dealers and distributors. This was a significant income source in the past. Owner and CEO, Mr. John Maxims, is considering a strategic initiative to produce a proprietary juice and cocktail brand with his family recipe to supply its internal beverage needs. If successful, the Group | intends to expand the juice and cocktail brand into a standalone commercial product line, selling to external hospitality and retail clients. : The research was carried out from September to December 2025: = Phase 1: Preliminary questionnaires and suggestions were collected from room guests and restaurant customers. The cost was absorbed in normal operation costs. The result was encouraging and positive. = Phase 2: Sample production, with free tasting sessions carried out in the reception area and restaurants. The cost of sample production was $8,000. The feedback and comments from tasters were also positive. = Phase 3: Marketing research and a pilot tasting group were carried out by Alberta Marketer, Inc. The research cost was $40,000. The marketer believed the new product was attractive and recommended a 5-year pilot project on small-scale production. i As a result, the Group is considering an investment in the juice processing and bottling facility in i one of the storage facilities in the hotel area owned by the company. It was currently abandoned (i and has no resale value. A production machine set, with an expected life of five years, will be fil acquired for this project. hi

Question:

Act like a helpful tutor and exlain Give step-by-step solution with explanation and final answer:

EEE Er EN es FET LT gr TTI Chee meme

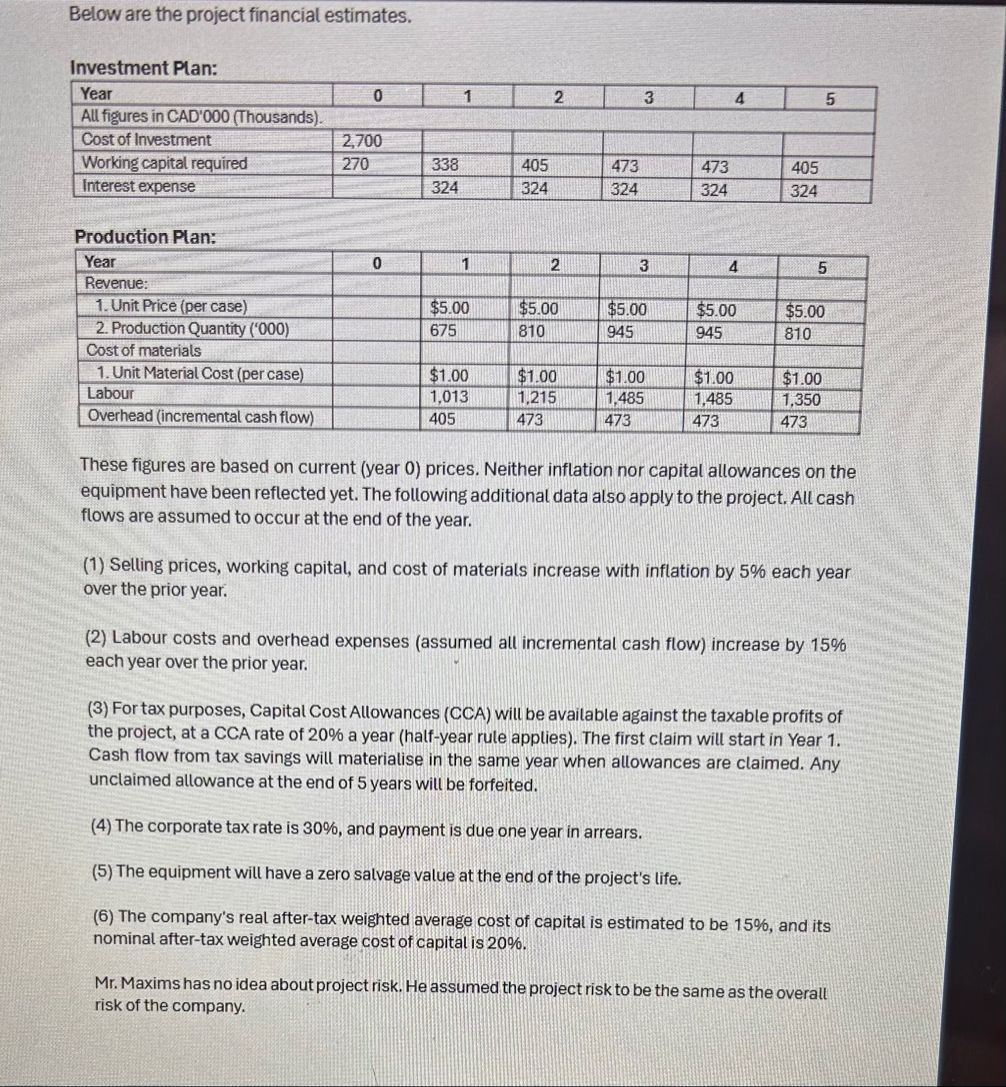

Below are the project financial estimates.

Investment Plan:

ECT a bam Sa le Ee [EA A BR CA Be ee

All figures in CAD'000 (Thousands).

TT ee es Ee] I I Eee

Working capital required {Zo [sss las [a3 [ams fase]

[ewstomense ———— 1 [ow [oa [ma [we Ta]

Production Plan: i

Revenue: hil

Ori Price or cae] EI HN 1 3 om Xo

2 Production Quantity (000 | Te76 [610 | [o45 [eds Teio |

lover masons rE TTT JST ie

1.Unit Material Cost percase) | [$100 | [$1.00 [$1.00

Labour 1,013 [11215 [1485 1,485

Overhead (incremental cash flow) 405 473 473 || [473

These figures are based on current (year 0) prices. Neither inflation nor capital allowances on the

equipment have been reflected yet. The following additional data also apply to the project. All cash

flows are assumed to occur at the end of the year,

(1) Selling prices, working capital, and cost of materials increase with inflation by 5% each year

over the prior year.

(2) Labour costs and overhead expenses (assumed all incremental cash flow) increase by 15%

each year over the prior year. I

(8) For tax purposes, Capital Cost Allowances (CCA) will be available against the taxable profits of

the project, at a CCA rate of 20% a year (half-year rule applies). The first claim will start in Year 1.

Cash flow from tax savings will materialise in the same year when allowances are claimed. Any

unclaimed allowance at the end of 5 years will be forfeited.

(4) The corporate tax rate is 309%, and payment is due one year in arrears.

(5) The equipment will have a zero salvage value at the end of the. project's life.

(6) The company's real after-tax weighted average cost of capital is estimated to be 15%, and its

nominal after-tax weighted average cost of capital is 20%.

Mr. Maxims has no idea about project risk. He assumed the project risk to be the same as the overall

risk of the company.

Holiday Group, Inc. (“The Group”) is a Canadian hotel group that has operated for over 30 years. =|

The Group owns and manages five hotels across Alberta: Traveler's Inn, Holiday Lodge, Resort :

Alpha, Resort Beta, and Hotel Charles.

Currently, all soft drinks and beverages served in guestrooms and hotel restaurants are purchased

from regional dealers and distributors. This was a significant income source in the past. Owner and

CEO, Mr. John Maxims, is considering a strategic initiative to produce a proprietary juice and

cocktail brand with his family recipe to supply its internal beverage needs. If successful, the Group |

intends to expand the juice and cocktail brand into a standalone commercial product line, selling

to external hospitality and retail clients. :

The research was carried out from September to December 2025:

= Phase 1: Preliminary questionnaires and suggestions were collected from room guests and

restaurant customers. The cost was absorbed in normal operation costs. The result was

encouraging and positive.

= Phase 2: Sample production, with free tasting sessions carried out in the reception area and

restaurants. The cost of sample production was $8,000. The feedback and comments from

tasters were also positive.

= Phase 3: Marketing research and a pilot tasting group were carried out by Alberta Marketer,

Inc. The research cost was $40,000. The marketer believed the new product was attractive

and recommended a 5-year pilot project on small-scale production.

i As a result, the Group is considering an investment in the juice processing and bottling facility in

i one of the storage facilities in the hotel area owned by the company. It was currently abandoned

(i and has no resale value. A production machine set, with an expected life of five years, will be

fil acquired for this project.

hi

EEE Er EN es FET LT gr TTI Chee meme

Below are the project financial estimates.

Investment Plan:

ECT a bam Sa le Ee [EA A BR CA Be ee

All figures in CAD'000 (Thousands).

TT ee es Ee] I I Eee

Working capital required {Zo [sss las [a3 [ams fase]

[ewstomense ———— 1 [ow [oa [ma [we Ta]

Production Plan: i

Revenue: hil

Ori Price or cae] EI HN 1 3 om Xo

2 Production Quantity (000 | Te76 [610 | [o45 [eds Teio |

lover masons rE TTT JST ie

1.Unit Material Cost percase) | [$100 | [$1.00 [$1.00

Labour 1,013 [11215 [1485 1,485

Overhead (incremental cash flow) 405 473 473 || [473

These figures are based on current (year 0) prices. Neither inflation nor capital allowances on the

equipment have been reflected yet. The following additional data also apply to the project. All cash

flows are assumed to occur at the end of the year,

(1) Selling prices, working capital, and cost of materials increase with inflation by 5% each year

over the prior year.

(2) Labour costs and overhead expenses (assumed all incremental cash flow) increase by 15%

each year over the prior year. I

(8) For tax purposes, Capital Cost Allowances (CCA) will be available against the taxable profits of

the project, at a CCA rate of 20% a year (half-year rule applies). The first claim will start in Year 1.

Cash flow from tax savings will materialise in the same year when allowances are claimed. Any

unclaimed allowance at the end of 5 years will be forfeited.

(4) The corporate tax rate is 309%, and payment is due one year in arrears.

(5) The equipment will have a zero salvage value at the end of the. project's life.

(6) The company's real after-tax weighted average cost of capital is estimated to be 15%, and its

nominal after-tax weighted average cost of capital is 20%.

Mr. Maxims has no idea about project risk. He assumed the project risk to be the same as the overall

risk of the company.

Holiday Group, Inc. (“The Group”) is a Canadian hotel group that has operated for over 30 years. =|

The Group owns and manages five hotels across Alberta: Traveler's Inn, Holiday Lodge, Resort :

Alpha, Resort Beta, and Hotel Charles.

Currently, all soft drinks and beverages served in guestrooms and hotel restaurants are purchased

from regional dealers and distributors. This was a significant income source in the past. Owner and

CEO, Mr. John Maxims, is considering a strategic initiative to produce a proprietary juice and

cocktail brand with his family recipe to supply its internal beverage needs. If successful, the Group |

intends to expand the juice and cocktail brand into a standalone commercial product line, selling

to external hospitality and retail clients. :

The research was carried out from September to December 2025:

= Phase 1: Preliminary questionnaires and suggestions were collected from room guests and

restaurant customers. The cost was absorbed in normal operation costs. The result was

encouraging and positive.

= Phase 2: Sample production, with free tasting sessions carried out in the reception area and

restaurants. The cost of sample production was $8,000. The feedback and comments from

tasters were also positive.

= Phase 3: Marketing research and a pilot tasting group were carried out by Alberta Marketer,

Inc. The research cost was $40,000. The marketer believed the new product was attractive

and recommended a 5-year pilot project on small-scale production.

i As a result, the Group is considering an investment in the juice processing and bottling facility in

i one of the storage facilities in the hotel area owned by the company. It was currently abandoned

(i and has no resale value. A production machine set, with an expected life of five years, will be

fil acquired for this project.

hi

Asked by: Francis

Created at: 2026-02-13 08:40:17

Final Answer:

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :