Answer in three steps along with explanation at the end of each step and final answer at the end of the answer. Calculate three times before answering as i need accurate answer.1. (5 Points) You are given the following information:

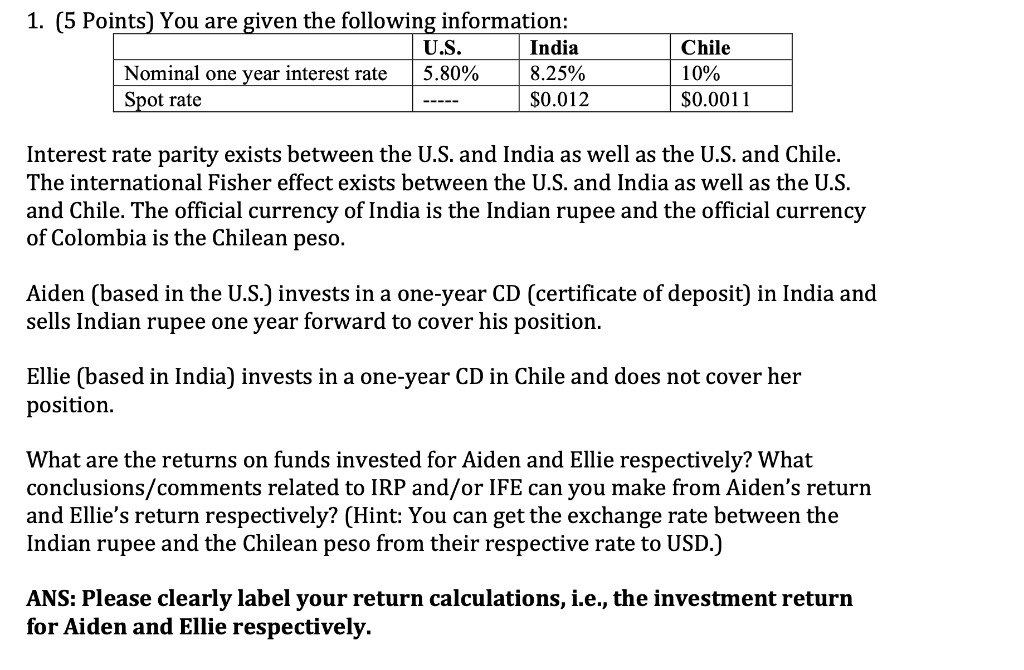

[~~ Jus. [india [Chile |

[Spotrate ~~ [-— [s0012 _|sogotl

Interest rate parity exists between the U.S. and India as well as the U.S. and Chile.

The international Fisher effect exists between the U.S. and India as well as the U.S.

and Chile. The official currency of India is the Indian rupee and the official currency

of Colombia is the Chilean peso.

Aiden (based in the U.S.) invests in a one-year CD (certificate of deposit) in India and

sells Indian rupee one year forward to cover his position.

Ellie (based in India) invests in a one-year CD in Chile and does not cover her

position.

What are the returns on funds invested for Aiden and Ellie respectively? What

conclusions/comments related to IRP and/or IFE can you make from Aiden’s return

and Ellie’s return respectively? (Hint: You can get the exchange rate between the

Indian rupee and the Chilean peso from their respective rate to USD.)

ANS: Please clearly label your return calculations, i.e., the investment return

for Aiden and Ellie respectively.

This is AI generated Response.

Asked by: Test User 100150

Created at: 2025-05-09 08:27:12

Answer:

RenderedRaw Text

Let's answer step by step, clearly showing the calculations for **Aiden** and **Ellie**, and explain at each step.

---

### **Step 1: Calculate Aiden’s Return (U.S. investor in India, hedged with forward contract)**

#### **Explanation:**

Aiden invests in India but hedges his currency risk by selling Indian rupees forward for USD. According to **Interest Rate Parity (IRP)**, the return for a hedged US investor in India will be the same as the US interest rate.

#### **Calculation:**

- **US Interest Rate:** 5.80%

- **India Interest Rate:** 8.25%

- **Spot Rate (INR/USD):** $0.012

**Forward rate using IRP:**

\[

\text{Forward Rate} = \text{Spot Rate} \times \left(\frac{1 + r_{India}}{1 + r_{US}}\right)

\]

\[

= 0.012 \times \left(\frac{1 + 0.0825}{1 + 0.058}\right)

= 0.012 \times \frac{1.0825}{1.058}

= 0.012 \times 1.02317

= 0.012278

\]

- If Aiden invests $1 in India at 8.25%, he has $1 × 1.0825 = $1.0825 worth of INR at year-end.

- He converts this back to USD at the forward rate.

\[

\text{Final USD} = \frac{1.0825 \times 0.012278}{0.012} = 1.0825 \times 1.02317 = 1.1081

\]

But since the forward rate locks in the parity, the USD return will always match the US rate.

\[

\text{Aiden's hedged return in USD} = 5.80\%

\]

#### **Explanation:**

The return matches the US interest rate, as required by covered interest rate parity.

---

### **Step 2: Calculate Ellie’s Return (Indian investor in Chile, unhedged)**

#### **Explanation:**

Ellie invests in Chilean CD at 10% without hedging. International Fisher Effect (IFE) applies, so the expected return for an Indian investor will be affected by both the Chilean interest rate and the expected change in exchange rates (INR/CLP).

- **India Interest Rate:** 8.25%

- **Chile Interest Rate:** 10%

- **Spot Rate (CLP/USD):** $0.0011

**Expected depreciation of the Chilean peso vs. rupee:**

\[

\text{IFE: } E\left(\frac{S_1}{S_0}\right) = \frac{1 + r_{India}}{1 + r_{Chile}}

\]

\[

= \frac{1.0825}{1.10} = 0.9841

\]

So, the Chilean peso is expected to depreciate by:

\[

\text{Depreciation} = 1 - 0.9841 = 0.0159 = 1.59\%

\]

**Unhedged return in INR:**

\[

\text{Return} = (1 + r_{Chile}) \times \left(\frac{S_1}{S_0}\right) - 1

\]

\[

= 1.10 \times 0.9841 - 1 = 1.0825 - 1 = 0.0825 = 8.25\%

\]

#### **Explanation:**

Ellie’s expected return in rupees is 8.25%, same as the Indian rate, as explained by the international Fisher effect.

---

### **Step 3: Summarize and State Final Answers**

#### **Aiden (US investor in India, hedged):**

- **Return in USD:** **5.80%**

- **Reason:** Covered IRP ensures Aiden gets the same return as US deposits when hedged.

#### **Ellie (Indian investor in Chile, unhedged):**

- **Return in INR:** **8.25%**

- **Reason:** IFE predicts the expected INR return equals the Indian deposit rate due to anticipated currency depreciation offsetting the interest differential.

---

## **Final Answers**

### **Aiden’s Investment Return:** **5.80% (in USD)**

### **Ellie’s Investment Return:** **8.25% (in INR)**

**Comment/Conclusion:**

- Aiden’s hedged return matches the US interest rate due to IRP.

- Ellie’s unhedged expected return matches the Indian interest rate due to the IFE.

- Both theories predict no arbitrage profits in international investments when hedging (IRP) or on average (IFE).

1. (5 Points) You are given the following information:

[~~ Jus. [india [Chile |

[Spotrate ~~ [-— [s0012 _|sogotl

Interest rate parity exists between the U.S. and India as well as the U.S. and Chile.

The international Fisher effect exists between the U.S. and India as well as the U.S.

and Chile. The official currency of India is the Indian rupee and the official currency

of Colombia is the Chilean peso.

Aiden (based in the U.S.) invests in a one-year CD (certificate of deposit) in India and

sells Indian rupee one year forward to cover his position.

Ellie (based in India) invests in a one-year CD in Chile and does not cover her

position.

What are the returns on funds invested for Aiden and Ellie respectively? What

conclusions/comments related to IRP and/or IFE can you make from Aiden’s return

and Ellie’s return respectively? (Hint: You can get the exchange rate between the

Indian rupee and the Chilean peso from their respective rate to USD.)

ANS: Please clearly label your return calculations, i.e., the investment return

for Aiden and Ellie respectively.

1. (5 Points) You are given the following information:

[~~ Jus. [india [Chile |

[Spotrate ~~ [-— [s0012 _|sogotl

Interest rate parity exists between the U.S. and India as well as the U.S. and Chile.

The international Fisher effect exists between the U.S. and India as well as the U.S.

and Chile. The official currency of India is the Indian rupee and the official currency

of Colombia is the Chilean peso.

Aiden (based in the U.S.) invests in a one-year CD (certificate of deposit) in India and

sells Indian rupee one year forward to cover his position.

Ellie (based in India) invests in a one-year CD in Chile and does not cover her

position.

What are the returns on funds invested for Aiden and Ellie respectively? What

conclusions/comments related to IRP and/or IFE can you make from Aiden’s return

and Ellie’s return respectively? (Hint: You can get the exchange rate between the

Indian rupee and the Chilean peso from their respective rate to USD.)

ANS: Please clearly label your return calculations, i.e., the investment return

for Aiden and Ellie respectively.