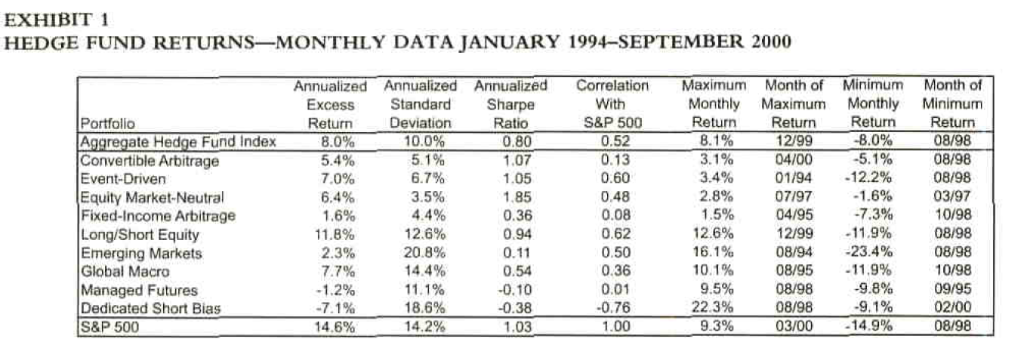

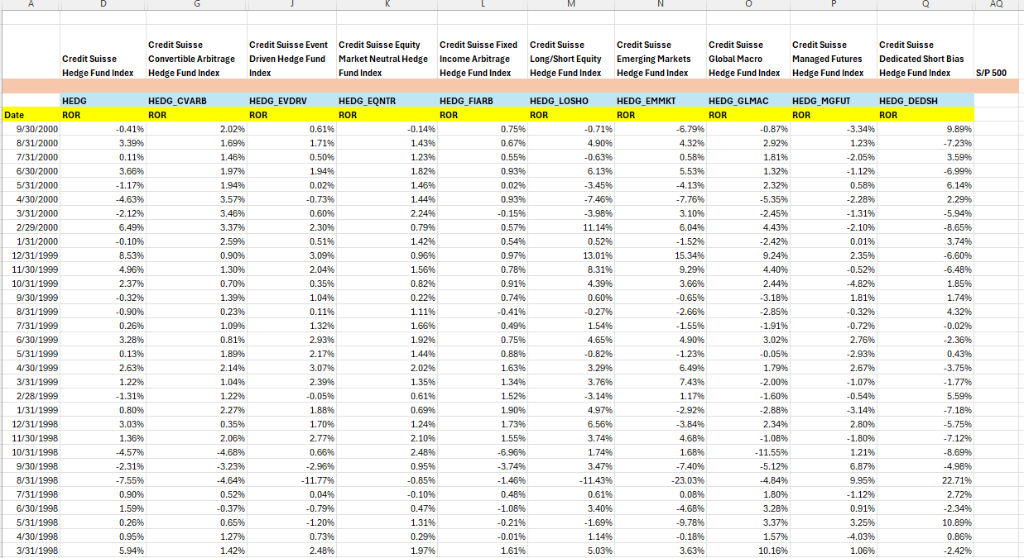

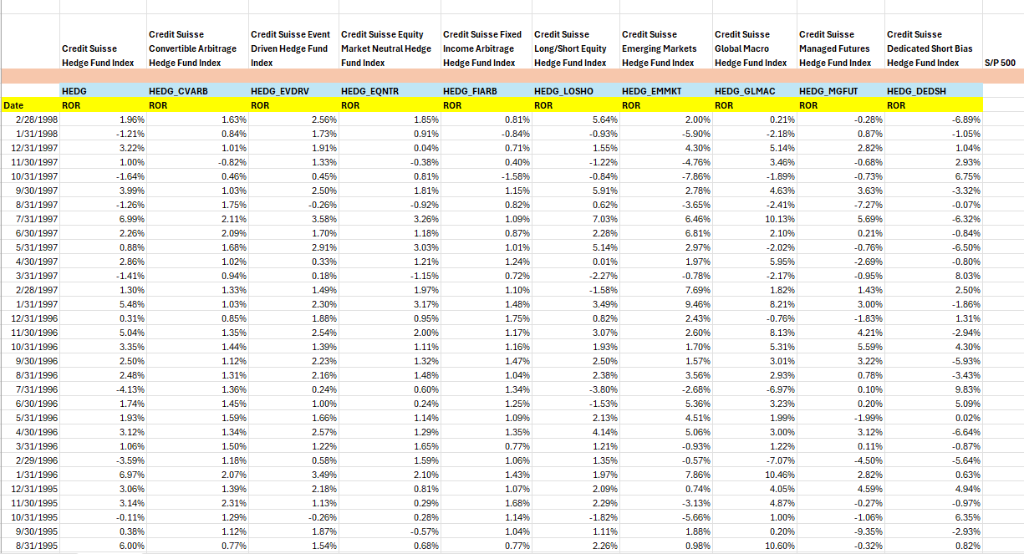

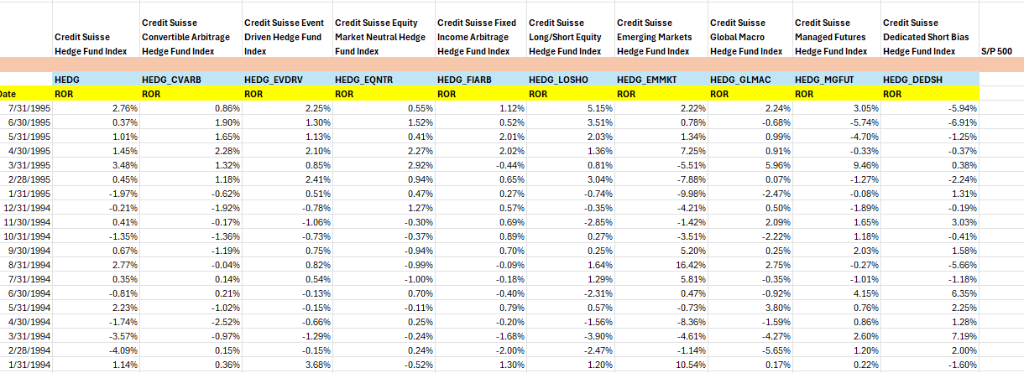

Below are the initial steps to gather your data together and prepare to reproduce Table 1 in the paper, the data summary, on page 8. Note that the months involved are January 1994 through September 2000.1. Turn to the S&P data. We will only use the 1-month Total Return column. Following the authors, we must subtract 20 basis points from the S&P values as a proxy for reasonable expenses to mimic an index. Recall that 20 basis points is one fifth of a percentage point. In excel this would be 0.002 or 0.2%. Subtract 20/12 basis points (0.002/12 in excel) from all the S&P monthly total return values. The goal is to then align the relevant date range of these adjusted return numbers next to the hedge fund data in the worksheet. Copy and paste these adjusted returns as values alongside the other data into your dataset. 2. Turn to the risk-free rate download. Divide the risk free rates by 12 to get an adequate monthly number. Divide them again by 100 to match the format of the S&P and the hedge fund indexes. Again, the goal is to then align the relevant date range of those numbers next to the other data in the dataset. But first you will likely need to “flip over” your risk-free data before you copy and paste the relevant range so that it matches the time direction of the dates in your dataset. This is usually done through using the sort function on the risk-free data. Then copy and paste the relevant range as values into your dataset. 3. We need the excess returns, not the absolute (ROR) returns. We will do this by subtracting the risk-free rate. As a precaution, recall that some numeric values in excel may be in a regular format, so something like 3.40 is simply a value of 3.40, and some values may be in a percentage format, so 3.40% may really have a cell value of 0.0340. Regardless of how your numbers are being displayed in excel, you must verify that your numbers are actually all in the same quantitative format, not differing by a factor of 100, before going further. 4. Choose a section of your workbook, probably to the right of your recently-created data block, and establish column titles for each of the 10 hedge fund data series and for the S&P column. For each cell in this workspace, enter a formula that takes the absolute return for that month and investment strategy and subtracts the risk-free rate for that month. Now you have a data block of excess returns. \begin{table}\captionsetup{labelformat=empty}\caption{EXHIBIT 1HEDGE FUND RETURNS-MONTHLY DATA JANUARY 1994-SEPTEMBER 2000}\begin{tabular}{|l|l|l|l|l|l|l|l|l|}\hline Portfollo & Annualized Excess Return & Annualized Standard Deviation & Annualized Sharpe Ratio & Correlation With S\&P 500 & Maximum Monthly Return & Month of Maximum Return & Minimum Monthly Return & Month of Minimum Return \\\hline Aggregate Hedge Fund Index & 8.0\% & 10.0\% & 0.80 & 0.52 & 8.1\% & 12/99 & -8.0\% & 08/98 \\\hline Convertible Arbitrage & 5.4\% & 5.1\% & 1.07 & 0.13 & 3.1\% & 04/00 & -5.1 Credit Suisse Hedge Fund IndexCredit Suisse Convertible Arbitrage Hedge Fund IndexCredit Suisse Event Driven Hedge Fund IndexCredit Suisse Equity Market Neutral Hedge Fund IndexCredit Suisse Fixed Income Arbitrage Hedge Fund IndexCredit Suisse Long/Short Equity Hedge Fund IndexCredit Suisse Emerging Markets Hedge Fund IndexCredit Suisse Global Macro Hedge Fund IndexCredit Suisse Managed Futures Hedge Fund IndexCredit Suisse Dedicated Short Bias Hedge Fund Index Show all imagesShow all imagesShow all images done loadingEXHIBIT 1 HEDGE FUND RETURNS—MONTHLY DATA JANUARY 1994-SEPTEMBER 2000 Annualized Annualized Annualized Correlation Maximum Month of Minimum Month of Excess Standard Sharpe With Monthly Maximum Monthly Minimum Portfolio Return Deviation Ratio S&P 500 Return Retwm _ Retum Retum [Convertible Arbitrage 5.4% 51% 1.07 0.13 31% 04100 5.1% 08/98 Event-Driven 7.0% 6.7% 1.05 060 34% 01/84 122% 08/98 Equity Market-Neutral 5.4% 35% 1.85 048 28% 0797 1.6% 03/97 Fixed-Income Arbitrage 16% 44% 036 008 15% 0495 7.3% 10/98 Long/Short Equity 1.8% 126% 094 062 126% 121909 11.9% 08/98 Emerging Markets 23% 20.8% 0.1 050 16.1% 08/94 234% 08/98 Global Macro 7.7% 14.4% 0.54 036 101% 085 1.9% 10/98 [Managed Futures 1.2% 1.1% 0.10 001 95% 08/98 98% 09/95 Dedicated Short Bias 71% 18.6% 0.38 -0.76 223% 08/98 91% 0200 Ea Es = E = - on = - a Credits. CredtSuissoEvent CreditSuisseEquty CrodiSusseFaed CrodiSuisse CrodtSuisse CroditSusse CrediSusse CreditSuisse CredtSuisse Comrie Avitsge Dive Hedge Fund Market Neutral Hedge locome Arbtisge Long/Short Equity EmergingMarkets GlobalMacro Managed Futures Dedicated Short Bias Madge Fundindes Wedge Funder Index Fund ex HedgoFundindex Hodge Fundindor HecgeFundindox edge Fund index HedgoFund index ModgeFundindes SIP500 eoe. Heoe_cuare a EDG FARE MEDGLOSHO WEDGEMMKI MEDGGLMAC WED MGFUT HED DEDSH ‘930200 oa 20m ose yr 07% one Fey osm am ry ava 330% 169% 171% Las oem. ass. ame 20% 123% EP 32000 oa re 050%. 123% fre 63% Pre La ET 350% sa0200 350% 19 108% 162% os 1% ss FE a “oso% s3v200 1m 19% oo. Laos, oom Eve an 23m sen em avon Fr 35m ar frre fry 740%, 770%, EE 22m 220% 3200 21m 300% 060%. 2288 015% as0% 31% 2am BEY som 29200 r=y 2am 230% 07%. 057%. fer sos. prey 210m ET av20 010 25% 051%. Lew ose 02%. 152% 2am oom by 21990 = 0% 200% 096%. osm. now 153%, 22 23% “eso m9 ry 130% 208 150% 7% saw 920% sion, osm “een wave 2am oom 035%. rey ow 4% 60% 200%, Fr 165% ‘93500 oa 139m prey ry oz os0% os5% EY fri 17m wave “oso 02m privy 1% oa om 260% 205% om am pee [ry 100m 1326 prey oaon prey 1556 1918 0mm oom sass Fry oan 206 126 07% prey prev 20m 270% 200m savin om fre 2m pores rey Pye 12% osm 20m am prey 26m 200% 0m 20 160% prey prey 170m 26m azn prey 12m Lom 239% prey Lae pry 7a “200 om arm prey am 12m yey ose press Jun 1am “Lem “osm som vsuie9 oon 22m 165% rey 1o0% aon 202%. Ee ET Er 123v1098 30m 0% 170% 126% 17% ssn. Ere 23am 200% ET 1w3ises 13% 200m 217% 2108 Ee Fy rey 108% 100% Er 10sv199 FEN Fe oes. 240%. 50% 178% 168% EE 1219 EE ‘saises 23 am 290% oss. ET 347% EZ san oom 450% vies EY om a7 Frey “Low, Fv Zo am Ey 27 Ey sox os 008%. 010%, oso%. oes. 00%. 100% 11m 27% saises 159% 0am 07% oa7%. ~Lo0% 30% as0% 20% oa 23 save ry = 120% 1% oz 160% arm%. 2am am 108% aaises osm 12m ome 02% oom per 01% 15 PT 080% w3v1908 Fry Tam 240% Lom prey som 263% 016% 106% 20% Creansusse. CredtSusseEint CrlegiSusseEquty CrediSusseFued CediiSusse CrediSusse CrediSusse CrediSisse Credisusse CredtSuisse Comerte Atbitiage Driven Hedge und Market Neutoledge Income Aritage Long/Short Equity Emerging Markets OobalMacro Managed Futures Dedicated Short Bias | edge Fundindex edge Fundindex ncex. Fundindex Hodge Fundinder Modo Fundinder HedgoFundindex Hodge Fundindex HodgoFundndes Hodge Fundindex SIP500 weds. HepG cuare. CTT WEDG FRB WEDGLOSHO WEDGEMMKI WEDGGLMAC HEDGMGFUT HEDG.DEDSH 21308 196% 16% 250% fry [ry som 20m [rr 028% Fry vaviss Eri rr prey ry o8e% ow S906 238% osm 105% 1211997 prey privy fry 00s on 155% am Sam 20 prey 1501997 100% Fr 139 03% 040% 122% azn 300m o6s%. 203. 10311997 Les 0so%. [ry om “156% ETT Er “Loo arm ors sraurser 200% 10% 250% fry 115% som 2m ry fry ame wiser ew 175% 0m 0s om ry ssw 2a 22%, oom 331997 pr 2ue rey pry 100m 70 ae freey soon sam sruse7 220% 200% 170% 116% osm 2209 sais 210% oz ass saiser [ry Leow 20% 20m 10m sum 207% 20 azem asm user 200% 10% om prey 120m oom 17% 90% 260% Fry ai007 aw rr 03% Fry om 22m ore 21m ssw ao 2nnss7 1308 13% Lan 1am 110m 156s 769% rs La 2508 vv1997 sa0% 105% 230% 3am Laon 30% sae sa 300m ees 121196 oa rey Loon [ry 179% [ry 240% 070% grey 1% 101996. som 135% 25 200% 1m 20m 26m sim aw 20% 102199 prey Lue Ey 1s Lin fren 10% sam sion am ors01s0s 2508 1% 22 EN Lams 2508 17%. 30 32% re 108 240% 1a 210% Lan 10m 230% sow. 20m 7% Ere Ty1%08 aw 10% 02 060% 13 300%. 260% FE ow Er eases pry prey Loo%, 026 125% 15% sa% 32m ry so0% sais prey prey rey 1108 Loom prey ase Loom 190% oo suisse sus 1% 25 129% Ee au S056. 300% sum py ysu1%08 ry 150% 122% Lon orm 121% Frey 12% ous Ere 21308 asm 1% sow 150% 100% 138% osm ET 450% fry vavioes. som 20 40% 210% Lom 1am 280% 104% prey prey 121995 fry ry 280 oan om 200% ore prey son ase 1301995. Jus 2318 113% 020% 16m 2208 Ere asm 027% ome 10511995 Fry 129% oz [ry 110% Ere ry 100% 100% 35% sra0rises 03% 1% 16m 057% 108 1% rey 020% 3% 280% asv1905. Go0% om pro sen 07m 226% 098% 10.80% ox2% Prey Creditsuisse CredtSuisseEuent CredtSuisseEquiy CroditSuissoFized CreditSuisse CredtSisse CrodtSusss CrediSuisse CreditSuisse CredtSuisse Comertibe Arbitrage Divenedge Fund Market Neutrl Hedge Income Arbitrage Long/Short Equity Emerging Markets GlobolMacro Managed Futures Dedicated Short Bias Hedge Fundindes Hedge Fundindex Indes Fundinces HedgeFundindes edgeFundindes HedgeFundindes HedgeFundindes edgeFundindes HedgeFundindes SPS00 rv) 270% 50% 225% 055% 112% sim 22% 2208 05%, EE ase om 150% 10%, 152% 052% asm oon Frey EY Fry savas 10% 165m 1% oan 20% 20% 13 05% 470% 125% wanes ase 200% 2108 22m 20% rey 725% oa Prey 0am vs Frey 132% oss, 20% yey oss EE son sen on 22m 0as%. 110% 201% [ry rey 08 750%, oom. zm 220% avis 197% 082% os oar fr oan 99% 247% 008% 1am 21084 yi 162m 07% 12m 057% 03% azn 050% 1a0% 10% sce oss. 01m 106% “030% 069%. Ere Las 200% 165% 30m 131508 as “Loon arm 0am rey om asm 22% 10% oa aa0s6s osm 119m 075% 9% 07% 02% sam 02% 20m 10% pre 27% oom Ir oom 009% fro froey 275% 027m som v1008 035% 1a 0ss%, 100% 01%. 129% so 03m ows Lies sass. Fry oa EYeY ox Fry 2% oar Fry ass [ey save 22% 102% 035% oa 07% osm orm 80% 07% 22% aa0nses 1a 25m yey [ry 020% 156% awn 150% ry 12m vee EEN “05m 129% “02% es 00m aos az 2609 710% 204 Pry 15% ais 02 200 2am 116% Frey rey 200% aves 114% 036% 268% 052% 130% 120% 1054 01% 022% Lox

Question:

Below are the initial steps to gather your data together and prepare to reproduce Table 1 in the paper, the data summary, on page 8. Note that the months involved are January 1994 through September 2000.1. Turn to the S&P data. We will only use the 1-month Total Return column. Following the authors, we must subtract 20 basis points from the S&P values as a proxy for reasonable expenses to mimic an index. Recall that 20 basis points is one fifth of a percentage point. In excel this would be 0.002 or 0.2%. Subtract 20/12 basis points (0.002/12 in excel) from all the S&P monthly total return values. The goal is to then align the relevant date range of these adjusted return numbers next to the hedge fund data in the worksheet. Copy and paste these adjusted returns as values alongside the other data into your dataset. 2. Turn to the risk-free rate download. Divide the risk free rates by 12 to get an adequate monthly number. Divide them again by 100 to match the format of the S&P and the hedge fund indexes. Again, the goal is to then align the relevant date range of those numbers next to the other data in the dataset. But first you will likely need to “flip over” your risk-free data before you copy and paste the relevant range so that it matches the time direction of the dates in your dataset. This is usually done through using the sort function on the risk-free data. Then copy and paste the relevant range as values into your dataset. 3. We need the excess returns, not the absolute (ROR) returns. We will do this by subtracting the risk-free rate. As a precaution, recall that some numeric values in excel may be in a regular format, so something like 3.40 is simply a value of 3.40, and some values may be in a percentage format, so 3.40% may really have a cell value of 0.0340. Regardless of how your numbers are being displayed in excel, you must verify that your numbers are actually all in the same quantitative format, not differing by a factor of 100, before going further. 4. Choose a section of your workbook, probably to the right of your recently-created data block, and establish column titles for each of the 10 hedge fund data series and for the S&P column. For each cell in this workspace, enter a formula that takes the absolute return for that month and investment strategy and subtracts the risk-free rate for that month. Now you have a data block of excess returns. \begin{table}\captionsetup{labelformat=empty}\caption{EXHIBIT 1HEDGE FUND RETURNS-MONTHLY DATA JANUARY 1994-SEPTEMBER 2000}\begin{tabular}{|l|l|l|l|l|l|l|l|l|}\hline Portfollo & Annualized Excess Return & Annualized Standard Deviation & Annualized Sharpe Ratio & Correlation With S\&P 500 & Maximum Monthly Return & Month of Maximum Return & Minimum Monthly Return & Month of Minimum Return \\\hline Aggregate Hedge Fund Index & 8.0\% & 10.0\% & 0.80 & 0.52 & 8.1\% & 12/99 & -8.0\% & 08/98 \\\hline Convertible Arbitrage & 5.4\% & 5.1\% & 1.07 & 0.13 & 3.1\% & 04/00 & -5.1 Credit Suisse Hedge Fund IndexCredit Suisse Convertible Arbitrage Hedge Fund IndexCredit Suisse Event Driven Hedge Fund IndexCredit Suisse Equity Market Neutral Hedge Fund IndexCredit Suisse Fixed Income Arbitrage Hedge Fund IndexCredit Suisse Long/Short Equity Hedge Fund IndexCredit Suisse Emerging Markets Hedge Fund IndexCredit Suisse Global Macro Hedge Fund IndexCredit Suisse Managed Futures Hedge Fund IndexCredit Suisse Dedicated Short Bias Hedge Fund Index Show all imagesShow all imagesShow all images done loading

EXHIBIT 1

HEDGE FUND RETURNS—MONTHLY DATA JANUARY 1994-SEPTEMBER 2000

Annualized Annualized Annualized Correlation Maximum Month of Minimum Month of

Excess Standard Sharpe With Monthly Maximum Monthly Minimum

Portfolio Return Deviation Ratio S&P 500 Return Retwm _ Retum Retum

[Convertible Arbitrage 5.4% 51% 1.07 0.13 31% 04100 5.1% 08/98

Event-Driven 7.0% 6.7% 1.05 060 34% 01/84 122% 08/98

Equity Market-Neutral 5.4% 35% 1.85 048 28% 0797 1.6% 03/97

Fixed-Income Arbitrage 16% 44% 036 008 15% 0495 7.3% 10/98

Long/Short Equity 1.8% 126% 094 062 126% 121909 11.9% 08/98

Emerging Markets 23% 20.8% 0.1 050 16.1% 08/94 234% 08/98

Global Macro 7.7% 14.4% 0.54 036 101% 085 1.9% 10/98

[Managed Futures 1.2% 1.1% 0.10 001 95% 08/98 98% 09/95

Dedicated Short Bias 71% 18.6% 0.38 -0.76 223% 08/98 91% 0200

Ea Es = E = - on = - a

Credits. CredtSuissoEvent CreditSuisseEquty CrodiSusseFaed CrodiSuisse CrodtSuisse CroditSusse CrediSusse CreditSuisse

CredtSuisse Comrie Avitsge Dive Hedge Fund Market Neutral Hedge locome Arbtisge Long/Short Equity EmergingMarkets GlobalMacro Managed Futures Dedicated Short Bias

Madge Fundindes Wedge Funder Index Fund ex HedgoFundindex Hodge Fundindor HecgeFundindox edge Fund index HedgoFund index ModgeFundindes SIP500

eoe. Heoe_cuare a EDG FARE MEDGLOSHO WEDGEMMKI MEDGGLMAC WED MGFUT HED DEDSH

‘930200 oa 20m ose yr 07% one Fey osm am ry

ava 330% 169% 171% Las oem. ass. ame 20% 123% EP

32000 oa re 050%. 123% fre 63% Pre La ET 350%

sa0200 350% 19 108% 162% os 1% ss FE a “oso%

s3v200 1m 19% oo. Laos, oom Eve an 23m sen em

avon Fr 35m ar frre fry 740%, 770%, EE 22m 220%

3200 21m 300% 060%. 2288 015% as0% 31% 2am BEY som

29200 r=y 2am 230% 07%. 057%. fer sos. prey 210m ET

av20 010 25% 051%. Lew ose 02%. 152% 2am oom by

21990 = 0% 200% 096%. osm. now 153%, 22 23% “eso

m9 ry 130% 208 150% 7% saw 920% sion, osm “een

wave 2am oom 035%. rey ow 4% 60% 200%, Fr 165%

‘93500 oa 139m prey ry oz os0% os5% EY fri 17m

wave “oso 02m privy 1% oa om 260% 205% om am

pee [ry 100m 1326 prey oaon prey 1556 1918 0mm oom

sass Fry oan 206 126 07% prey prev 20m 270% 200m

savin om fre 2m pores rey Pye 12% osm 20m am

prey 26m 200% 0m 20 160% prey prey 170m 26m azn

prey 12m Lom 239% prey Lae pry 7a “200 om arm

prey am 12m yey ose press Jun 1am “Lem “osm som

vsuie9 oon 22m 165% rey 1o0% aon 202%. Ee ET Er

123v1098 30m 0% 170% 126% 17% ssn. Ere 23am 200% ET

1w3ises 13% 200m 217% 2108 Ee Fy rey 108% 100% Er

10sv199 FEN Fe oes. 240%. 50% 178% 168% EE 1219 EE

‘saises 23 am 290% oss. ET 347% EZ san oom 450%

vies EY om a7 Frey “Low, Fv Zo am Ey 27

Ey sox os 008%. 010%, oso%. oes. 00%. 100% 11m 27%

saises 159% 0am 07% oa7%. ~Lo0% 30% as0% 20% oa 23

save ry = 120% 1% oz 160% arm%. 2am am 108%

aaises osm 12m ome 02% oom per 01% 15 PT 080%

w3v1908 Fry Tam 240% Lom prey som 263% 016% 106% 20%

Creansusse. CredtSusseEint CrlegiSusseEquty CrediSusseFued CediiSusse CrediSusse CrediSusse CrediSisse Credisusse

CredtSuisse Comerte Atbitiage Driven Hedge und Market Neutoledge Income Aritage Long/Short Equity Emerging Markets OobalMacro Managed Futures Dedicated Short Bias

| edge Fundindex edge Fundindex ncex. Fundindex Hodge Fundinder Modo Fundinder HedgoFundindex Hodge Fundindex HodgoFundndes Hodge Fundindex SIP500

weds. HepG cuare. CTT WEDG FRB WEDGLOSHO WEDGEMMKI WEDGGLMAC HEDGMGFUT HEDG.DEDSH

21308 196% 16% 250% fry [ry som 20m [rr 028% Fry

vaviss Eri rr prey ry o8e% ow S906 238% osm 105%

1211997 prey privy fry 00s on 155% am Sam 20 prey

1501997 100% Fr 139 03% 040% 122% azn 300m o6s%. 203.

10311997 Les 0so%. [ry om “156% ETT Er “Loo arm ors

sraurser 200% 10% 250% fry 115% som 2m ry fry ame

wiser ew 175% 0m 0s om ry ssw 2a 22%, oom

331997 pr 2ue rey pry 100m 70 ae freey soon sam

sruse7 220% 200% 170% 116% osm 2209 sais 210% oz ass

saiser [ry Leow 20% 20m 10m sum 207% 20 azem asm

user 200% 10% om prey 120m oom 17% 90% 260% Fry

ai007 aw rr 03% Fry om 22m ore 21m ssw ao

2nnss7 1308 13% Lan 1am 110m 156s 769% rs La 2508

vv1997 sa0% 105% 230% 3am Laon 30% sae sa 300m ees

121196 oa rey Loon [ry 179% [ry 240% 070% grey 1%

101996. som 135% 25 200% 1m 20m 26m sim aw 20%

102199 prey Lue Ey 1s Lin fren 10% sam sion am

ors01s0s 2508 1% 22 EN Lams 2508 17%. 30 32% re

108 240% 1a 210% Lan 10m 230% sow. 20m 7% Ere

Ty1%08 aw 10% 02 060% 13 300%. 260% FE ow Er

eases pry prey Loo%, 026 125% 15% sa% 32m ry so0%

sais prey prey rey 1108 Loom prey ase Loom 190% oo

suisse sus 1% 25 129% Ee au S056. 300% sum py

ysu1%08 ry 150% 122% Lon orm 121% Frey 12% ous Ere

21308 asm 1% sow 150% 100% 138% osm ET 450% fry

vavioes. som 20 40% 210% Lom 1am 280% 104% prey prey

121995 fry ry 280 oan om 200% ore prey son ase

1301995. Jus 2318 113% 020% 16m 2208 Ere asm 027% ome

10511995 Fry 129% oz [ry 110% Ere ry 100% 100% 35%

sra0rises 03% 1% 16m 057% 108 1% rey 020% 3% 280%

asv1905. Go0% om pro sen 07m 226% 098% 10.80% ox2% Prey

Creditsuisse CredtSuisseEuent CredtSuisseEquiy CroditSuissoFized CreditSuisse CredtSisse CrodtSusss CrediSuisse CreditSuisse

CredtSuisse Comertibe Arbitrage Divenedge Fund Market Neutrl Hedge Income Arbitrage Long/Short Equity Emerging Markets GlobolMacro Managed Futures Dedicated Short Bias

Hedge Fundindes Hedge Fundindex Indes Fundinces HedgeFundindes edgeFundindes HedgeFundindes HedgeFundindes edgeFundindes HedgeFundindes SPS00

rv) 270% 50% 225% 055% 112% sim 22% 2208 05%, EE

ase om 150% 10%, 152% 052% asm oon Frey EY Fry

savas 10% 165m 1% oan 20% 20% 13 05% 470% 125%

wanes ase 200% 2108 22m 20% rey 725% oa Prey 0am

vs Frey 132% oss, 20% yey oss EE son sen on

22m 0as%. 110% 201% [ry rey 08 750%, oom. zm 220%

avis 197% 082% os oar fr oan 99% 247% 008% 1am

21084 yi 162m 07% 12m 057% 03% azn 050% 1a0% 10%

sce oss. 01m 106% “030% 069%. Ere Las 200% 165% 30m

131508 as “Loon arm 0am rey om asm 22% 10% oa

aa0s6s osm 119m 075% 9% 07% 02% sam 02% 20m 10%

pre 27% oom Ir oom 009% fro froey 275% 027m som

v1008 035% 1a 0ss%, 100% 01%. 129% so 03m ows Lies

sass. Fry oa EYeY ox Fry 2% oar Fry ass [ey

save 22% 102% 035% oa 07% osm orm 80% 07% 22%

aa0nses 1a 25m yey [ry 020% 156% awn 150% ry 12m

vee EEN “05m 129% “02% es 00m aos az 2609 710%

204 Pry 15% ais 02 200 2am 116% Frey rey 200%

aves 114% 036% 268% 052% 130% 120% 1054 01% 022% Lox

EXHIBIT 1

HEDGE FUND RETURNS—MONTHLY DATA JANUARY 1994-SEPTEMBER 2000

Annualized Annualized Annualized Correlation Maximum Month of Minimum Month of

Excess Standard Sharpe With Monthly Maximum Monthly Minimum

Portfolio Return Deviation Ratio S&P 500 Return Retwm _ Retum Retum

[Convertible Arbitrage 5.4% 51% 1.07 0.13 31% 04100 5.1% 08/98

Event-Driven 7.0% 6.7% 1.05 060 34% 01/84 122% 08/98

Equity Market-Neutral 5.4% 35% 1.85 048 28% 0797 1.6% 03/97

Fixed-Income Arbitrage 16% 44% 036 008 15% 0495 7.3% 10/98

Long/Short Equity 1.8% 126% 094 062 126% 121909 11.9% 08/98

Emerging Markets 23% 20.8% 0.1 050 16.1% 08/94 234% 08/98

Global Macro 7.7% 14.4% 0.54 036 101% 085 1.9% 10/98

[Managed Futures 1.2% 1.1% 0.10 001 95% 08/98 98% 09/95

Dedicated Short Bias 71% 18.6% 0.38 -0.76 223% 08/98 91% 0200

Ea Es = E = - on = - a

Credits. CredtSuissoEvent CreditSuisseEquty CrodiSusseFaed CrodiSuisse CrodtSuisse CroditSusse CrediSusse CreditSuisse

CredtSuisse Comrie Avitsge Dive Hedge Fund Market Neutral Hedge locome Arbtisge Long/Short Equity EmergingMarkets GlobalMacro Managed Futures Dedicated Short Bias

Madge Fundindes Wedge Funder Index Fund ex HedgoFundindex Hodge Fundindor HecgeFundindox edge Fund index HedgoFund index ModgeFundindes SIP500

eoe. Heoe_cuare a EDG FARE MEDGLOSHO WEDGEMMKI MEDGGLMAC WED MGFUT HED DEDSH

‘930200 oa 20m ose yr 07% one Fey osm am ry

ava 330% 169% 171% Las oem. ass. ame 20% 123% EP

32000 oa re 050%. 123% fre 63% Pre La ET 350%

sa0200 350% 19 108% 162% os 1% ss FE a “oso%

s3v200 1m 19% oo. Laos, oom Eve an 23m sen em

avon Fr 35m ar frre fry 740%, 770%, EE 22m 220%

3200 21m 300% 060%. 2288 015% as0% 31% 2am BEY som

29200 r=y 2am 230% 07%. 057%. fer sos. prey 210m ET

av20 010 25% 051%. Lew ose 02%. 152% 2am oom by

21990 = 0% 200% 096%. osm. now 153%, 22 23% “eso

m9 ry 130% 208 150% 7% saw 920% sion, osm “een

wave 2am oom 035%. rey ow 4% 60% 200%, Fr 165%

‘93500 oa 139m prey ry oz os0% os5% EY fri 17m

wave “oso 02m privy 1% oa om 260% 205% om am

pee [ry 100m 1326 prey oaon prey 1556 1918 0mm oom

sass Fry oan 206 126 07% prey prev 20m 270% 200m

savin om fre 2m pores rey Pye 12% osm 20m am

prey 26m 200% 0m 20 160% prey prey 170m 26m azn

prey 12m Lom 239% prey Lae pry 7a “200 om arm

prey am 12m yey ose press Jun 1am “Lem “osm som

vsuie9 oon 22m 165% rey 1o0% aon 202%. Ee ET Er

123v1098 30m 0% 170% 126% 17% ssn. Ere 23am 200% ET

1w3ises 13% 200m 217% 2108 Ee Fy rey 108% 100% Er

10sv199 FEN Fe oes. 240%. 50% 178% 168% EE 1219 EE

‘saises 23 am 290% oss. ET 347% EZ san oom 450%

vies EY om a7 Frey “Low, Fv Zo am Ey 27

Ey sox os 008%. 010%, oso%. oes. 00%. 100% 11m 27%

saises 159% 0am 07% oa7%. ~Lo0% 30% as0% 20% oa 23

save ry = 120% 1% oz 160% arm%. 2am am 108%

aaises osm 12m ome 02% oom per 01% 15 PT 080%

w3v1908 Fry Tam 240% Lom prey som 263% 016% 106% 20%

Creansusse. CredtSusseEint CrlegiSusseEquty CrediSusseFued CediiSusse CrediSusse CrediSusse CrediSisse Credisusse

CredtSuisse Comerte Atbitiage Driven Hedge und Market Neutoledge Income Aritage Long/Short Equity Emerging Markets OobalMacro Managed Futures Dedicated Short Bias

| edge Fundindex edge Fundindex ncex. Fundindex Hodge Fundinder Modo Fundinder HedgoFundindex Hodge Fundindex HodgoFundndes Hodge Fundindex SIP500

weds. HepG cuare. CTT WEDG FRB WEDGLOSHO WEDGEMMKI WEDGGLMAC HEDGMGFUT HEDG.DEDSH

21308 196% 16% 250% fry [ry som 20m [rr 028% Fry

vaviss Eri rr prey ry o8e% ow S906 238% osm 105%

1211997 prey privy fry 00s on 155% am Sam 20 prey

1501997 100% Fr 139 03% 040% 122% azn 300m o6s%. 203.

10311997 Les 0so%. [ry om “156% ETT Er “Loo arm ors

sraurser 200% 10% 250% fry 115% som 2m ry fry ame

wiser ew 175% 0m 0s om ry ssw 2a 22%, oom

331997 pr 2ue rey pry 100m 70 ae freey soon sam

sruse7 220% 200% 170% 116% osm 2209 sais 210% oz ass

saiser [ry Leow 20% 20m 10m sum 207% 20 azem asm

user 200% 10% om prey 120m oom 17% 90% 260% Fry

ai007 aw rr 03% Fry om 22m ore 21m ssw ao

2nnss7 1308 13% Lan 1am 110m 156s 769% rs La 2508

vv1997 sa0% 105% 230% 3am Laon 30% sae sa 300m ees

121196 oa rey Loon [ry 179% [ry 240% 070% grey 1%

101996. som 135% 25 200% 1m 20m 26m sim aw 20%

102199 prey Lue Ey 1s Lin fren 10% sam sion am

ors01s0s 2508 1% 22 EN Lams 2508 17%. 30 32% re

108 240% 1a 210% Lan 10m 230% sow. 20m 7% Ere

Ty1%08 aw 10% 02 060% 13 300%. 260% FE ow Er

eases pry prey Loo%, 026 125% 15% sa% 32m ry so0%

sais prey prey rey 1108 Loom prey ase Loom 190% oo

suisse sus 1% 25 129% Ee au S056. 300% sum py

ysu1%08 ry 150% 122% Lon orm 121% Frey 12% ous Ere

21308 asm 1% sow 150% 100% 138% osm ET 450% fry

vavioes. som 20 40% 210% Lom 1am 280% 104% prey prey

121995 fry ry 280 oan om 200% ore prey son ase

1301995. Jus 2318 113% 020% 16m 2208 Ere asm 027% ome

10511995 Fry 129% oz [ry 110% Ere ry 100% 100% 35%

sra0rises 03% 1% 16m 057% 108 1% rey 020% 3% 280%

asv1905. Go0% om pro sen 07m 226% 098% 10.80% ox2% Prey

Creditsuisse CredtSuisseEuent CredtSuisseEquiy CroditSuissoFized CreditSuisse CredtSisse CrodtSusss CrediSuisse CreditSuisse

CredtSuisse Comertibe Arbitrage Divenedge Fund Market Neutrl Hedge Income Arbitrage Long/Short Equity Emerging Markets GlobolMacro Managed Futures Dedicated Short Bias

Hedge Fundindes Hedge Fundindex Indes Fundinces HedgeFundindes edgeFundindes HedgeFundindes HedgeFundindes edgeFundindes HedgeFundindes SPS00

rv) 270% 50% 225% 055% 112% sim 22% 2208 05%, EE

ase om 150% 10%, 152% 052% asm oon Frey EY Fry

savas 10% 165m 1% oan 20% 20% 13 05% 470% 125%

wanes ase 200% 2108 22m 20% rey 725% oa Prey 0am

vs Frey 132% oss, 20% yey oss EE son sen on

22m 0as%. 110% 201% [ry rey 08 750%, oom. zm 220%

avis 197% 082% os oar fr oan 99% 247% 008% 1am

21084 yi 162m 07% 12m 057% 03% azn 050% 1a0% 10%

sce oss. 01m 106% “030% 069%. Ere Las 200% 165% 30m

131508 as “Loon arm 0am rey om asm 22% 10% oa

aa0s6s osm 119m 075% 9% 07% 02% sam 02% 20m 10%

pre 27% oom Ir oom 009% fro froey 275% 027m som

v1008 035% 1a 0ss%, 100% 01%. 129% so 03m ows Lies

sass. Fry oa EYeY ox Fry 2% oar Fry ass [ey

save 22% 102% 035% oa 07% osm orm 80% 07% 22%

aa0nses 1a 25m yey [ry 020% 156% awn 150% ry 12m

vee EEN “05m 129% “02% es 00m aos az 2609 710%

204 Pry 15% ais 02 200 2am 116% Frey rey 200%

aves 114% 036% 268% 052% 130% 120% 1054 01% 022% Lox

Asked by: chandu

Created at: 2025-10-26 01:05:28

Final Answer:

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :