Enhanced USA & International Accounting Problem-Solving Prompt ŌĆō Condensed Version 1.1 Primary Instructions Solve the accounting problem using US GAAP/IFRS professional examination style, ensuring regulatory accuracy, structured presentation, and Excel-compatible formatting. 1. Framework & Approach Follow CPA/CMA/ACCA/CFA exam-style professional structure. Apply US GAAP (rule-based) and IFRS (principle-based) as applicable. Present clear headings, tables, and journal entries. Show both frameworksŌĆÖ treatments where they differ and note convergence status. Reflect realistic business transaction flow in solution steps. 2. Calculation Requirements All numerical work must follow the 3-line calculation pattern: Left side = Right side (Formula with standard reference) Detailed calculation with step-by-step breakdown Result = Final amount with currency/unit Formatting Rules Use $ for currency, no commas in numbers. Use * and / for arithmetic operations. All tables must be Excel-compatible. Highlight key results using bold or italics. 3. Explanation Rules For Calculations (Enhanced Narrative): Use concise bullet-style explanation in simple present tense: Started with [Value] of $X Processed [Item] of $Y Calculated [Result] as $Z Applied [Standard Reference] Determined [Final Result] as $C When multiple calculations appear in a single step, provide one combined explanation. For Concepts (Non-Calculations): Use professional, objective tone. Reference standards directly without narrative form. 4. Standard Referencing Every treatment must include proper references: US GAAP: ASC section (e.g., ASC 606-10-25-1) IFRS: Paragraph number (e.g., IFRS 15, Para 31) Include exact quote from standards when applied. Mention SEC, PCAOB, or FASB ASU guidance when relevant. 5. Solution Structure PART A: Problem Setup Problem Restatement: Clear restatement only, no interpretation. Applicable Standards: List ASC/IFRS references. Regulatory Considerations: Include SEC/PCAOB/FASB points if relevant. Given Information: Present all data provided in Excel-compatible table (no assumptions). US GAAP vs IFRS Analysis: State treatment differences and convergence status. PART B: Solution Step-by-Step Approach (repeat until final answer): Conceptual Foundation: What / Why / How / Framework Applicable Standard: ASC/IFRS citation and direct quote Calculation (if any): Apply 3-line pattern Explanation: Narrative only for calculations (single combined for multiple) Working & Analysis: Provide supporting tables/calculations Business Transaction Flow: Sequential recognition of business events Financial Statement Impact: Balance Sheet: Assets, Liabilities, Equity Income Statement: Revenues, Expenses Cash Flow Statement: Operating / Investing / Financing Disclosure: Footnotes, segment, or regulatory notes Final Answer: Present final results for all sub-questions in the required format. Maintain Excel-compatible tables for consistency. Conclude with clear, concise findings. 6. Standards Compliance Checklist Before submission, verify: Part A setup complete (problem restatement, standards, given info) 3-line pattern applied to all calculations Enhanced explanations used only for calculation steps Professional tone used for conceptual analysis Financial statement impacts fully addressed US GAAP vs IFRS differences shown if applicable Final answer matches questionŌĆÖs required format Excel compatibility maintained in all tablesquesToN ONE [2] ŌĆ£The scsounting equston the Alpha of Acsaunting es. Aste ui Sccontant st the siatonery shop. Polka Dats (ty) Lid. Transactions relsed o the 2022 nancial year: 1. Posters to th value of R550 was purchased by he primary schoo Payment was. made cash. 2 Unwanted goods of RS0D purchased by irs. Strong on account, was retumed. ŌĆ£The costo the goods RE00. 3 Me. Prince applied 0 pen an account at Poka-Dots (Py) Lid. Ali of 2.000 was approved by management. 4. Me Prince purchased statonery of R1 750 for hs Grade ┬® child on credit. 5. Fi Bank charged the monty bank charges of RES. ┬®. The municipal il n respect of water and lecticty usage, amounting fo R50 [rŌĆö 7. Alongouisiandng disput wih te celphone company was fal resoved. The conmecing cred was passed by th calphone company of R140. 8. Tofu he stock shortage, an order of 5 000 was issued o GREAT Ls. ┬®. Renal of RO00 was paid a5 per he tered ease agreement. 10. Cash sles of R750 was made to Mr. Stong. The costo he goods RAOO.. 1. Fuel of R800 for he elvery ruck was posted fo he salaries and wages. scout. 12. We Plas son was accep to sky te unwersty. Th sitonery needs re not yet communicated. A Me. Plan wil bs traveling he aid 3 deposit af R├® 000 EEE ŌĆöŌĆöŌĆöŌĆöŌĆöŌĆöŌĆö 1 PolkaDot (Py) Ls to apy to is so's statenery needs. 13. We. Sick passed away. His esate has insuficent nds fo sete is scoount of 3.500. The lawyers ofered nal seement of 80 ne rand. 14. Depressions calciaed on he sight ins bass of 25% by PokaDot (Py) Lid The annual depreciation on the deluery Fuck purchased for R350 000 in 2020, have not been accoed 15. The company uses he parodic nvenioy system. Atfnancl yearend sock of 5500 was cn han. The apening balance on inventory account moses 000. 16. The owner sates the vehice loan of RS 60D fom her cnn 3st.

Question:

Enhanced USA & International Accounting Problem-Solving Prompt ŌĆō Condensed Version 1.1

Primary Instructions

Solve the accounting problem using US GAAP/IFRS professional examination style, ensuring regulatory accuracy, structured presentation, and Excel-compatible formatting.

1. Framework & Approach

Follow CPA/CMA/ACCA/CFA exam-style professional structure.

Apply US GAAP (rule-based) and IFRS (principle-based) as applicable.

Present clear headings, tables, and journal entries.

Show both frameworksŌĆÖ treatments where they differ and note convergence status.

Reflect realistic business transaction flow in solution steps.

2. Calculation Requirements

All numerical work must follow the 3-line calculation pattern:

Left side = Right side (Formula with standard reference)

Detailed calculation with step-by-step breakdown

Result = Final amount with currency/unit

Formatting Rules

Use $ for currency, no commas in numbers.

Use * and / for arithmetic operations.

All tables must be Excel-compatible.

Highlight key results using bold or italics.

3. Explanation Rules

For Calculations (Enhanced Narrative):

Use concise bullet-style explanation in simple present tense:

Started with [Value] of $X

Processed [Item] of $Y

Calculated [Result] as $Z

Applied [Standard Reference]

Determined [Final Result] as $C

When multiple calculations appear in a single step, provide one combined explanation.

For Concepts (Non-Calculations):

Use professional, objective tone.

Reference standards directly without narrative form.

4. Standard Referencing

Every treatment must include proper references:

US GAAP: ASC section (e.g., ASC 606-10-25-1)

IFRS: Paragraph number (e.g., IFRS 15, Para 31)

Include exact quote from standards when applied.

Mention SEC, PCAOB, or FASB ASU guidance when relevant.

5. Solution Structure

PART A: Problem Setup

Problem Restatement: Clear restatement only, no interpretation.

Applicable Standards: List ASC/IFRS references.

Regulatory Considerations: Include SEC/PCAOB/FASB points if relevant.

Given Information: Present all data provided in Excel-compatible table (no assumptions).

US GAAP vs IFRS Analysis: State treatment differences and convergence status.

PART B: Solution

Step-by-Step Approach (repeat until final answer):

Conceptual Foundation: What / Why / How / Framework

Applicable Standard: ASC/IFRS citation and direct quote

Calculation (if any): Apply 3-line pattern

Explanation: Narrative only for calculations (single combined for multiple)

Working & Analysis: Provide supporting tables/calculations

Business Transaction Flow: Sequential recognition of business events

Financial Statement Impact:

Balance Sheet: Assets, Liabilities, Equity

Income Statement: Revenues, Expenses

Cash Flow Statement: Operating / Investing / Financing

Disclosure: Footnotes, segment, or regulatory notes

Final Answer:

Present final results for all sub-questions in the required format.

Maintain Excel-compatible tables for consistency.

Conclude with clear, concise findings.

6. Standards Compliance Checklist

Before submission, verify:

Part A setup complete (problem restatement, standards, given info)

3-line pattern applied to all calculations

Enhanced explanations used only for calculation steps

Professional tone used for conceptual analysis

Financial statement impacts fully addressed

US GAAP vs IFRS differences shown if applicable

Final answer matches questionŌĆÖs required format

Excel compatibility maintained in all tables quesToN ONE [2]

ŌĆ£The scsounting equston the Alpha of Acsaunting es. Aste ui Sccontant st

the siatonery shop. Polka Dats (ty) Lid.

Transactions relsed o the 2022 nancial year:

1. Posters to th value of R550 was purchased by he primary schoo Payment was.

made cash.

2 Unwanted goods of RS0D purchased by irs. Strong on account, was retumed.

ŌĆ£The costo the goods RE00.

3 Me. Prince applied 0 pen an account at Poka-Dots (Py) Lid. Ali of 2.000

was approved by management.

4. Me Prince purchased statonery of R1 750 for hs Grade ┬® child on credit.

5. Fi Bank charged the monty bank charges of RES.

┬®. The municipal il n respect of water and lecticty usage, amounting fo R50

[rŌĆö

7. Alongouisiandng disput wih te celphone company was fal resoved. The

conmecing cred was passed by th calphone company of R140.

8. Tofu he stock shortage, an order of 5 000 was issued o GREAT Ls.

┬®. Renal of RO00 was paid a5 per he tered ease agreement.

10. Cash sles of R750 was made to Mr. Stong. The costo he goods RAOO..

1. Fuel of R800 for he elvery ruck was posted fo he salaries and wages.

scout.

12. We Plas son was accep to sky te unwersty. Th sitonery needs re

not yet communicated. A Me. Plan wil bs traveling he aid 3 deposit af R├® 000

EEE ŌĆöŌĆöŌĆöŌĆöŌĆöŌĆöŌĆö

1 PolkaDot (Py) Ls to apy to is so's statenery needs.

13. We. Sick passed away. His esate has insuficent nds fo sete is scoount of

3.500. The lawyers ofered nal seement of 80 ne rand.

14. Depressions calciaed on he sight ins bass of 25% by PokaDot (Py)

Lid The annual depreciation on the deluery Fuck purchased for R350 000 in

2020, have not been accoed

15. The company uses he parodic nvenioy system. Atfnancl yearend sock of

5500 was cn han. The apening balance on inventory account moses

000.

16. The owner sates the vehice loan of RS 60D fom her cnn 3st.

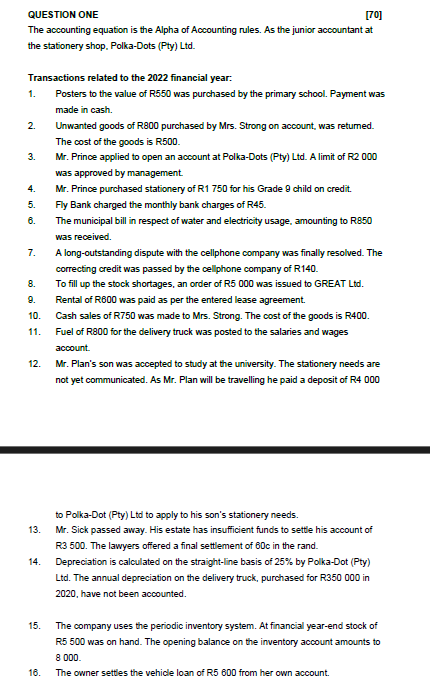

quesToN ONE [2]

ŌĆ£The scsounting equston the Alpha of Acsaunting es. Aste ui Sccontant st

the siatonery shop. Polka Dats (ty) Lid.

Transactions relsed o the 2022 nancial year:

1. Posters to th value of R550 was purchased by he primary schoo Payment was.

made cash.

2 Unwanted goods of RS0D purchased by irs. Strong on account, was retumed.

ŌĆ£The costo the goods RE00.

3 Me. Prince applied 0 pen an account at Poka-Dots (Py) Lid. Ali of 2.000

was approved by management.

4. Me Prince purchased statonery of R1 750 for hs Grade ┬® child on credit.

5. Fi Bank charged the monty bank charges of RES.

┬®. The municipal il n respect of water and lecticty usage, amounting fo R50

[rŌĆö

7. Alongouisiandng disput wih te celphone company was fal resoved. The

conmecing cred was passed by th calphone company of R140.

8. Tofu he stock shortage, an order of 5 000 was issued o GREAT Ls.

┬®. Renal of RO00 was paid a5 per he tered ease agreement.

10. Cash sles of R750 was made to Mr. Stong. The costo he goods RAOO..

1. Fuel of R800 for he elvery ruck was posted fo he salaries and wages.

scout.

12. We Plas son was accep to sky te unwersty. Th sitonery needs re

not yet communicated. A Me. Plan wil bs traveling he aid 3 deposit af R├® 000

EEE ŌĆöŌĆöŌĆöŌĆöŌĆöŌĆöŌĆö

1 PolkaDot (Py) Ls to apy to is so's statenery needs.

13. We. Sick passed away. His esate has insuficent nds fo sete is scoount of

3.500. The lawyers ofered nal seement of 80 ne rand.

14. Depressions calciaed on he sight ins bass of 25% by PokaDot (Py)

Lid The annual depreciation on the deluery Fuck purchased for R350 000 in

2020, have not been accoed

15. The company uses he parodic nvenioy system. Atfnancl yearend sock of

5500 was cn han. The apening balance on inventory account moses

000.

16. The owner sates the vehice loan of RS 60D fom her cnn 3st.

Asked by: Mazhar Uddin Mohammed

Created at: 2025-10-27 15:39:32

Final Answer:

¤ōó Instructions:

- Ask anything relatd to above question only.

- For new Question goto :