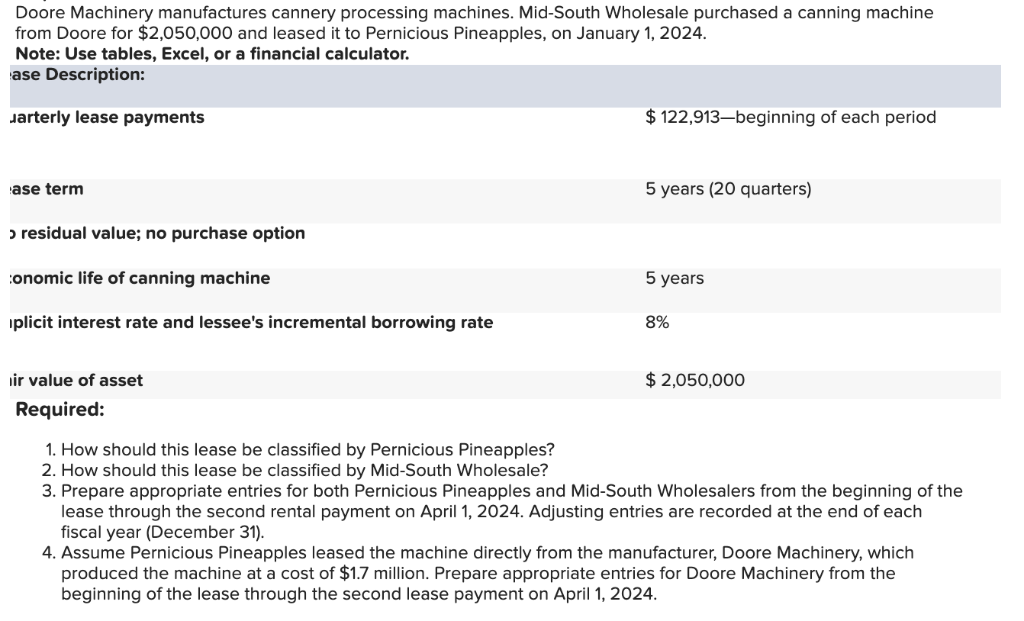

explain and give final summaryDoore Machinery manufactures cannery processing machines. Mid-South Wholesale purchased a canning machine

from Doore for $2,050,000 and leased it to Pernicious Pineapples, on January 1, 2024.

Note: Use tables, Excel, or a financial calculator.

ŌĆśase Description:

Jarterly lease payments $122,913ŌĆöbeginning of each period

ase term 5 years (20 quarters)

> residual value; no purchase option

:onomic life of canning machine 5 years

plicit interest rate and lessee's incremental borrowing rate 8%

iir value of asset $2,050,000

Required:

1. How should this lease be classified by Pernicious Pineapples?

2. How should this lease be classified by Mid-South Wholesale?

3. Prepare appropriate entries for both Pernicious Pineapples and Mid-South Wholesalers from the beginning of the

lease through the second rental payment on April 1, 2024. Adjusting entries are recorded at the end of each

fiscal year (December 31)

4. Assume Pernicious Pineapples leased the machine directly from the manufacturer, Doore Machinery, which

produced the machine at a cost of $1.7 million. Prepare appropriate entries for Doore Machinery from the

beginning of the lease through the second lease payment on April 1, 2024.

Question:

explain and give final summaryDoore Machinery manufactures cannery processing machines. Mid-South Wholesale purchased a canning machine

from Doore for $2,050,000 and leased it to Pernicious Pineapples, on January 1, 2024.

Note: Use tables, Excel, or a financial calculator.

ŌĆśase Description:

Jarterly lease payments $122,913ŌĆöbeginning of each period

ase term 5 years (20 quarters)

> residual value; no purchase option

:onomic life of canning machine 5 years

plicit interest rate and lessee's incremental borrowing rate 8%

iir value of asset $2,050,000

Required:

1. How should this lease be classified by Pernicious Pineapples?

2. How should this lease be classified by Mid-South Wholesale?

3. Prepare appropriate entries for both Pernicious Pineapples and Mid-South Wholesalers from the beginning of the

lease through the second rental payment on April 1, 2024. Adjusting entries are recorded at the end of each

fiscal year (December 31)

4. Assume Pernicious Pineapples leased the machine directly from the manufacturer, Doore Machinery, which

produced the machine at a cost of $1.7 million. Prepare appropriate entries for Doore Machinery from the

beginning of the lease through the second lease payment on April 1, 2024.

This is AI generated Response.

Asked by: sreegeeth

Created at: 2025-07-28 11:31:10

Final Answer:

RenderedRaw Text

Did you like this answer?

Let's break down the requirements and provide a final summary based on the information given.

---

## **Lease Details Summary**

- **Lease Payments:** $122,913 per quarter (beginning of each period)

- **Lease Term:** 5 years (20 quarters)

- **No residual value, no purchase option**

- **Economic Life of Asset:** 5 years

- **Interest Rate:** 8%

- **Fair Value of Asset:** $2,050,000

---

## **Required Answers**

### **1. Lease Classification by Pernicious Pineapples (Lessee)**

**Analysis:**

Under ASC 842 (US GAAP), a lease is classified as a **finance lease** by the lessee if any of the following criteria are met:

- Lease transfers ownership by the end of the term.

- Lease contains a purchase option that is reasonably certain to be exercised.

- Lease term is for the major part (generally 75% or more) of the economic life.

- Present value of lease payments equals or exceeds substantially all (generally 90% or more) of the fair value of the asset.

**Here:**

- Lease term = economic life (5 years).

- No transfer of ownership or purchase option.

- Present value of lease payments likely equals fair value (since lease payments are designed for full payout).

**Conclusion:**

**Classified as a Finance Lease** by Pernicious Pineapples.

---

### **2. Lease Classification by Mid-South Wholesale (Lessor)**

**Analysis:**

Under ASC 842, a lessor classifies a lease as a **sales-type** lease if it meets any of the following:

- Lease transfers ownership.

- Contains a purchase option that is reasonably certain to be exercised.

- Lease term is for the major part of the economic life.

- Present value of lease payments equals or exceeds substantially all of the fair value.

**Here:**

- Lease term = economic life.

- Lease payments equal the fair value of the asset.

- No purchase option or ownership transfer.

**Conclusion:**

**Classified as a Sales-Type Lease** by Mid-South Wholesale.

---

### **3. Journal Entries through April 1, 2024 (Second Rental Payment)**

#### **A. Pernicious Pineapples (Lessee):**

**At Lease Inception (Jan 1, 2024):**

- Recognize Right-of-Use Asset and Lease Liability at present value of lease payments.

*Assume PV = $2,050,000 (since payments match fair value and rate is given):*

```

Dr. Right-of-Use Asset $2,050,000

Cr. Lease Liability $2,050,000

```

**First Lease Payment (Jan 1, 2024):**

- Payment made at beginning, reduces lease liability

```

Dr. Lease Liability $122,913

Cr. Cash $122,913

```

**Interest and Amortization at March 31, 2024:**

- Interest for Q1: ($2,050,000 - $122,913) ├Ś 2% = $38,542 (2% is quarterly rate from 8%/4)

- Amortization: ($2,050,000 / 20) = $102,500 per quarter (straight-line for simplicity if required)

```

Dr. Interest Expense $38,542

Cr. Lease Liability $38,542

Dr. Amortization Expense $102,500

Cr. Right-of-Use Asset $102,500

```

**Second Lease Payment (April 1, 2024):**

```

Dr. Lease Liability $122,913

Cr. Cash $122,913

```

---

#### **B. Mid-South Wholesale (Lessor):**

**At Lease Inception (Jan 1, 2024):**

- Derecognize asset, recognize lease receivable and sales revenue

```

Dr. Lease Receivable $2,050,000

Cr. Equipment $2,050,000

```

**First Lease Payment (Jan 1, 2024):**

```

Dr. Cash $122,913

Cr. Lease Receivable $122,913

```

**Interest Income at March 31, 2024:**

- Interest for Q1: ($2,050,000 - $122,913) ├Ś 2% = $38,542

```

Dr. Lease Receivable $38,542

Cr. Interest Income $38,542

```

**Second Lease Payment (April 1, 2024):**

```

Dr. Cash $122,913

Cr. Lease Receivable $122,913

```

---

### **4. If Pernicious Pineapples Leased Directly from Doore Machinery**

**Doore Machinery (Manufacturer/Lessor):**

- Cost: $1,700,000; Fair Value: $2,050,000; thus, Manufacturer Profit = $350,000

**At Lease Inception (Jan 1, 2024):**

- Recognize sales revenue at fair value, cost of goods sold at cost, and lease receivable

```

Dr. Lease Receivable $2,050,000

Cr. Sales Revenue $2,050,000

Dr. Cost of Goods Sold $1,700,000

Cr. Inventory $1,700,000

```

**First Lease Payment (Jan 1, 2024):**

```

Dr. Cash $122,913

Cr. Lease Receivable $122,913

```

**Interest Income at March 31, 2024:**

- Interest for Q1: ($2,050,000 - $122,913) ├Ś 2% = $38,542

```

Dr. Lease Receivable $38,542

Cr. Interest Income $38,542

```

**Second Lease Payment (April 1, 2024):**

```

Dr. Cash $122,913

Cr. Lease Receivable $122,913

```

---

## **Final Summary**

- **Lease is a finance lease for the lessee (Pernicious Pineapples) and a sales-type lease for the lessor (Mid-South Wholesale or Doore Machinery).**

- **Both parties recognize the lease at the present value of payments; lessee records a right-of-use asset and liability, lessor records a lease receivable.**

- **Journal entries track lease payments, interest, amortization (lessee), and income recognition (lessor).**

- **If the lessor is a manufacturer (Doore Machinery), additional entries for sales revenue and cost of goods sold are needed.**

Let me know if you need the full amortization schedule or any further breakdown!

VIPSolutions focuses on clear, stepŌĆæbyŌĆæstep explanations so you can learn quickly. Whether you need an AIŌĆægenerated walkthrough or a short hint to get unstuck, each solution is organized for fast reading and easy review later.

Search similar questions, compare approaches, and bookmark the best answers for revision. Our goal is simple: quick, reliable study help that feels naturalŌĆönot noisy.

Doore Machinery manufactures cannery processing machines. Mid-South Wholesale purchased a canning machine

from Doore for $2,050,000 and leased it to Pernicious Pineapples, on January 1, 2024.

Note: Use tables, Excel, or a financial calculator.

ŌĆśase Description:

Jarterly lease payments $122,913ŌĆöbeginning of each period

ase term 5 years (20 quarters)

> residual value; no purchase option

:onomic life of canning machine 5 years

plicit interest rate and lessee's incremental borrowing rate 8%

iir value of asset $2,050,000

Required:

1. How should this lease be classified by Pernicious Pineapples?

2. How should this lease be classified by Mid-South Wholesale?

3. Prepare appropriate entries for both Pernicious Pineapples and Mid-South Wholesalers from the beginning of the

lease through the second rental payment on April 1, 2024. Adjusting entries are recorded at the end of each

fiscal year (December 31)

4. Assume Pernicious Pineapples leased the machine directly from the manufacturer, Doore Machinery, which

produced the machine at a cost of $1.7 million. Prepare appropriate entries for Doore Machinery from the

beginning of the lease through the second lease payment on April 1, 2024.

Doore Machinery manufactures cannery processing machines. Mid-South Wholesale purchased a canning machine

from Doore for $2,050,000 and leased it to Pernicious Pineapples, on January 1, 2024.

Note: Use tables, Excel, or a financial calculator.

ŌĆśase Description:

Jarterly lease payments $122,913ŌĆöbeginning of each period

ase term 5 years (20 quarters)

> residual value; no purchase option

:onomic life of canning machine 5 years

plicit interest rate and lessee's incremental borrowing rate 8%

iir value of asset $2,050,000

Required:

1. How should this lease be classified by Pernicious Pineapples?

2. How should this lease be classified by Mid-South Wholesale?

3. Prepare appropriate entries for both Pernicious Pineapples and Mid-South Wholesalers from the beginning of the

lease through the second rental payment on April 1, 2024. Adjusting entries are recorded at the end of each

fiscal year (December 31)

4. Assume Pernicious Pineapples leased the machine directly from the manufacturer, Doore Machinery, which

produced the machine at a cost of $1.7 million. Prepare appropriate entries for Doore Machinery from the

beginning of the lease through the second lease payment on April 1, 2024.