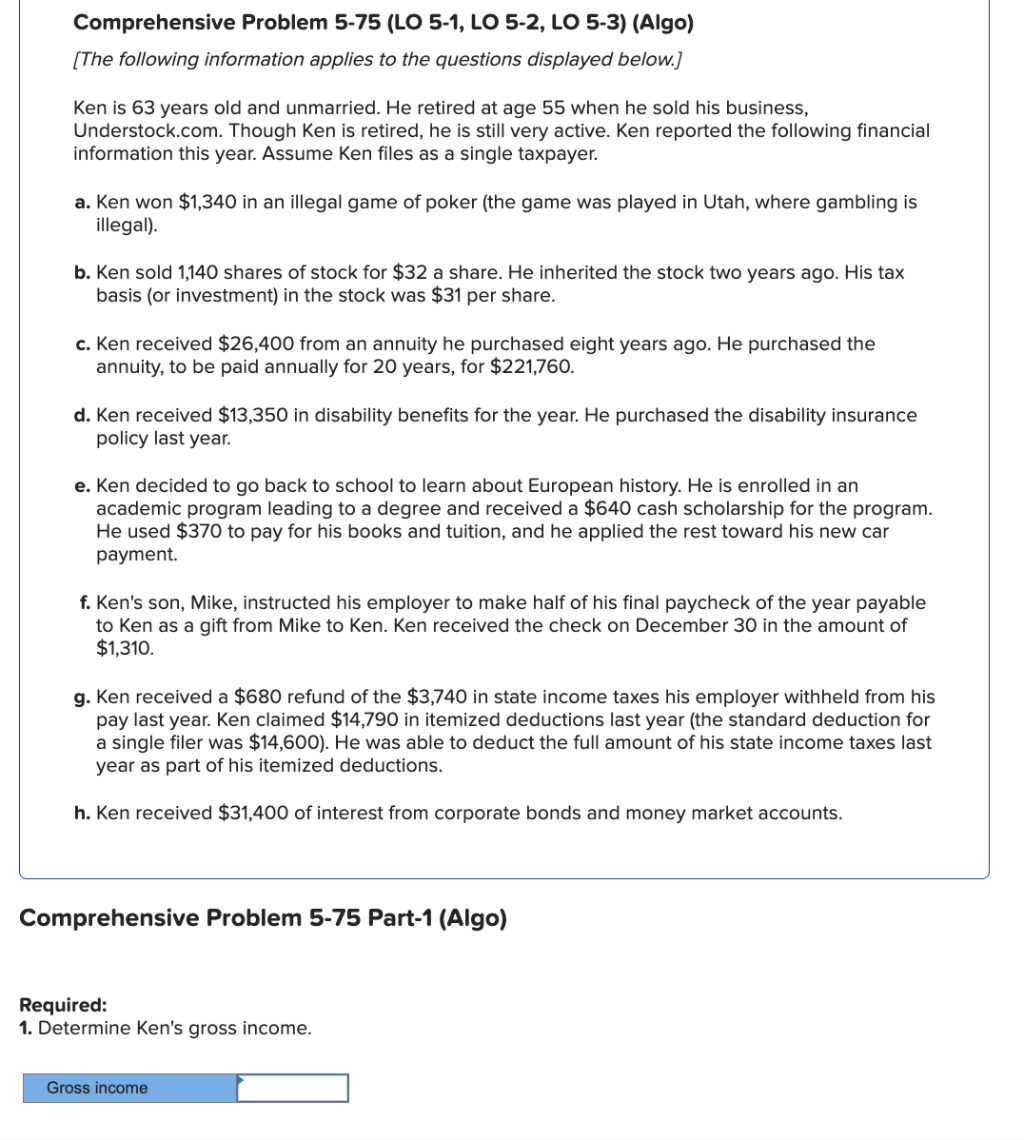

Give step-by-step solution with explanation and final answer:Comprehensive Problem 5-75 (LO 5-1, LO 5-2, LO 5-3) (Algo)

[The following information applies to the questions displayed below.]

Ken is 63 years old and unmarried. He retired at age 55 when he sold his business,

Understock.com. Though Ken is retired, he is still very active. Ken reported the following financial

information this year. Assume Ken files as a single taxpayer.

a. Ken won $1,340 in an illegal game of poker (the game was played in Utah, where gambling is

illegal).

b. Ken sold 1140 shares of stock for $32 a share. He inherited the stock two years ago. His tax

basis (or investment) in the stock was $31 per share.

c. Ken received $26,400 from an annuity he purchased eight years ago. He purchased the

annuity, to be paid annually for 20 years, for $221,760.

d. Ken received $13,350 in disability benefits for the year. He purchased the disability insurance

policy last year.

e. Ken decided to go back to school to learn about European history. He is enrolled in an

academic program leading to a degree and received a $640 cash scholarship for the program.

He used $370 to pay for his books and tuition, and he applied the rest toward his new car

payment.

f. Ken's son, Mike, instructed his employer to make half of his final paycheck of the year payable

to Ken as a gift from Mike to Ken. Ken received the check on December 30 in the amount of

$1,310.

g. Ken received a $680 refund of the $3,740 in state income taxes his employer withheld from his

pay last year. Ken claimed $14,790 in itemized deductions last year (the standard deduction for

a single filer was $14,600). He was able to deduct the full amount of his state income taxes last

year as part of his itemized deductions.

h. Ken received $31,400 of interest from corporate bonds and money market accounts.

Comprehensive Problem 5-75 Part-1 (Algo)

Required:

1. Determine Ken's gross income.

Question:

Give step-by-step solution with explanation and final answer:Comprehensive Problem 5-75 (LO 5-1, LO 5-2, LO 5-3) (Algo)

[The following information applies to the questions displayed below.]

Ken is 63 years old and unmarried. He retired at age 55 when he sold his business,

Understock.com. Though Ken is retired, he is still very active. Ken reported the following financial

information this year. Assume Ken files as a single taxpayer.

a. Ken won $1,340 in an illegal game of poker (the game was played in Utah, where gambling is

illegal).

b. Ken sold 1140 shares of stock for $32 a share. He inherited the stock two years ago. His tax

basis (or investment) in the stock was $31 per share.

c. Ken received $26,400 from an annuity he purchased eight years ago. He purchased the

annuity, to be paid annually for 20 years, for $221,760.

d. Ken received $13,350 in disability benefits for the year. He purchased the disability insurance

policy last year.

e. Ken decided to go back to school to learn about European history. He is enrolled in an

academic program leading to a degree and received a $640 cash scholarship for the program.

He used $370 to pay for his books and tuition, and he applied the rest toward his new car

payment.

f. Ken's son, Mike, instructed his employer to make half of his final paycheck of the year payable

to Ken as a gift from Mike to Ken. Ken received the check on December 30 in the amount of

$1,310.

g. Ken received a $680 refund of the $3,740 in state income taxes his employer withheld from his

pay last year. Ken claimed $14,790 in itemized deductions last year (the standard deduction for

a single filer was $14,600). He was able to deduct the full amount of his state income taxes last

year as part of his itemized deductions.

h. Ken received $31,400 of interest from corporate bonds and money market accounts.

Comprehensive Problem 5-75 Part-1 (Algo)

Required:

1. Determine Ken's gross income.

This is AI generated Response.

Asked by: Piyush makwana

Created at: 2026-01-20 23:21:31

Thought Process:

RenderedRaw Text

**Reviewing capital gains and annuity calculations**

I see that capital gains must be included in gross income, and that full gain amounts are counted—so that’s +$1,140. I also need to remember that for inherited stock, the basis gets stepped up to FMV at the decedent's death, and even if the holding period doesn’t affect gross income, it does affect the rate. In the case of Ken's annuity, I need to calculate the exclusion ratio based on his annual payment and the total cost of the annuity.**Calculating annuity exclusion ratios**

For annuities starting after 1986, the exclusion ratio equals the investment in the contract divided by the expected return. I know that for Ken's fixed-term annuity, the expected return is calculated as the number of payments times the payment amount. He paid $221,760 for a 20-year annuity with annual payments of $26,400, giving an expected return of $528,000. The exclusion percentage calculates to about 42%. So, I can derive that the excluded amount from gross income is $11,088, leaving a taxable portion of $15,312.**Reviewing annuity and disability benefits**

Ken purchased the annuity eight years ago and has been receiving annual payments of $26,400. The taxable portion of $15,312 must be included for this year. Even after eight years of payments, he hasn't fully recovered his initial investment of $221,760. In fact, he still has $133,056 left to recover. Now, regarding his disability benefits, Ken received $13,350 for the year, and it's worth noting that he bought the disability insurance policy just last year.**Evaluating disability benefits and scholarship use**

Benefits from a policy paid for with after-tax dollars aren't included in gross income, so since Ken purchased his disability policy himself, his $13,350 benefit is excludable from gross income. Now, regarding his scholarship of $640 for European history studies, I see that he used $370 for books and tuition, which are excludable expenses. However, the amount he applied toward his car payment isn’t qualified, so that portion will be taxable.**Summarizing income items for final calculations**

Okay, let's confirm the calculations for Ken's income items. His disability benefits are excludable because he purchased the policy himself. The total gross income calculates to $49,652. For the state income tax refund of $680, since he itemized last year and the tax benefit is $190, that's the amount included.

Here's a breakdown of all items:

a) Gambling winnings: $1,340

b) Stock sale (LTCG): $1,140

c) Annuity exclusion calculation shows tax of $15,312.

d) Disability benefits are $0, excludable.

e) Scholarship nonqualified amount: $270.

f) Gift from son: $0.

g) State refund inclusion: $190.

h) Interest income: $31,400.

Total: $1,340 + $1,140 + $15,312 + $270 + $190 + $31,400 = $49,652.

Final Answer:

RenderedRaw Text

Did you like this answer?

Step-by-step treatment of each item

a. Illegal poker winnings: taxable. Include $1,340.

b. Sale of inherited stock: include gain only.

- Proceeds: 1,140 shares × $32 = $36,480

- Basis: 1,140 × $31 = $35,340

- Long-term capital gain included: $36,480 − $35,340 = $1,140.

c. Annuity payments: part taxable under the exclusion ratio.

- Investment in contract: $221,760

- Expected return: $26,400 × 20 years = $528,000

- Exclusion ratio: $,760 ÷ $528,000 = 42%

- Excluded portion this year: 42% × $26,400 = $11,088

- Taxable portion: $26,400 − $11,088 = $15,312.

d. Disability benefits from a policy Ken purchased himself: excludable. Include $0.

e. Scholarship: excludable to the extent used for qualified tuition and required course materials.

- Scholarship received: $640

- Used for qualified expenses: $370

- Taxable amount (used for car): $640 − $370 = $270.

f. Paycheck directed to Ken by son: wages are taxable to the son; payment is a gift to Ken. Include $0.

g. State income tax refund: taxable only to the extent it produced a tax benefit last year.

- Last year’s itemized: $14,790; standard deduction: $14,600

- Excess over standard (tax benefit): $14,790 − $14,600 = $190

- Refund received: $680 → taxable portion = lesser of $680 or $190 = $190.

h. Interest from corporate bonds and money market accounts: fully taxable. Include $31,400.

Compute Ken’s gross income

1,340 (a) + 1,140 (b) + 15,312 (c) + 0 (d) + 270 (e) + 0 (f) + 190 (g) + 31,400 (h)

= $49,652

Final answer: Ken’s gross income for the year is $49,652.

VIPSolutions focuses on clear, step‑by‑step explanations so you can learn quickly. Whether you need an AI‑generated walkthrough or a short hint to get unstuck, each solution is organized for fast reading and easy review later.

Search similar questions, compare approaches, and bookmark the best answers for revision. Our goal is simple: quick, reliable study help that feels natural—not noisy.

Comprehensive Problem 5-75 (LO 5-1, LO 5-2, LO 5-3) (Algo)

[The following information applies to the questions displayed below.]

Ken is 63 years old and unmarried. He retired at age 55 when he sold his business,

Understock.com. Though Ken is retired, he is still very active. Ken reported the following financial

information this year. Assume Ken files as a single taxpayer.

a. Ken won $1,340 in an illegal game of poker (the game was played in Utah, where gambling is

illegal).

b. Ken sold 1140 shares of stock for $32 a share. He inherited the stock two years ago. His tax

basis (or investment) in the stock was $31 per share.

c. Ken received $26,400 from an annuity he purchased eight years ago. He purchased the

annuity, to be paid annually for 20 years, for $221,760.

d. Ken received $13,350 in disability benefits for the year. He purchased the disability insurance

policy last year.

e. Ken decided to go back to school to learn about European history. He is enrolled in an

academic program leading to a degree and received a $640 cash scholarship for the program.

He used $370 to pay for his books and tuition, and he applied the rest toward his new car

payment.

f. Ken's son, Mike, instructed his employer to make half of his final paycheck of the year payable

to Ken as a gift from Mike to Ken. Ken received the check on December 30 in the amount of

$1,310.

g. Ken received a $680 refund of the $3,740 in state income taxes his employer withheld from his

pay last year. Ken claimed $14,790 in itemized deductions last year (the standard deduction for

a single filer was $14,600). He was able to deduct the full amount of his state income taxes last

year as part of his itemized deductions.

h. Ken received $31,400 of interest from corporate bonds and money market accounts.

Comprehensive Problem 5-75 Part-1 (Algo)

Required:

1. Determine Ken's gross income.

Comprehensive Problem 5-75 (LO 5-1, LO 5-2, LO 5-3) (Algo)

[The following information applies to the questions displayed below.]

Ken is 63 years old and unmarried. He retired at age 55 when he sold his business,

Understock.com. Though Ken is retired, he is still very active. Ken reported the following financial

information this year. Assume Ken files as a single taxpayer.

a. Ken won $1,340 in an illegal game of poker (the game was played in Utah, where gambling is

illegal).

b. Ken sold 1140 shares of stock for $32 a share. He inherited the stock two years ago. His tax

basis (or investment) in the stock was $31 per share.

c. Ken received $26,400 from an annuity he purchased eight years ago. He purchased the

annuity, to be paid annually for 20 years, for $221,760.

d. Ken received $13,350 in disability benefits for the year. He purchased the disability insurance

policy last year.

e. Ken decided to go back to school to learn about European history. He is enrolled in an

academic program leading to a degree and received a $640 cash scholarship for the program.

He used $370 to pay for his books and tuition, and he applied the rest toward his new car

payment.

f. Ken's son, Mike, instructed his employer to make half of his final paycheck of the year payable

to Ken as a gift from Mike to Ken. Ken received the check on December 30 in the amount of

$1,310.

g. Ken received a $680 refund of the $3,740 in state income taxes his employer withheld from his

pay last year. Ken claimed $14,790 in itemized deductions last year (the standard deduction for

a single filer was $14,600). He was able to deduct the full amount of his state income taxes last

year as part of his itemized deductions.

h. Ken received $31,400 of interest from corporate bonds and money market accounts.

Comprehensive Problem 5-75 Part-1 (Algo)

Required:

1. Determine Ken's gross income.