Give step-by-step solution with explanation and final answer: Act like a helpful tutor and exlain me :A married couple is trying to finance their three - year - old son's college education. Money can be deposited at 6% compounded quarterly. What end-of - quarter deposit must be made from the son's 3rd birthday to his 18th birthday to provide $60,000 on each birthday from the 18th to the 21st? (Note that the first deposit comes three months after his 3rd birthday and the last deposit is made on the date of the first withdrawal.) Note - Solve only with the equations in the image, and nominal, quarterly, and effective interest types. F=pP+D)" P=Fa+i)" ~N a+ 1 Foal A=F———] a+p¥-1 N 1+ -1 poait -t +1 (1+) . ~N 1+ A= pt a+p¥-1

Question:

Give step-by-step solution with explanation and final answer:

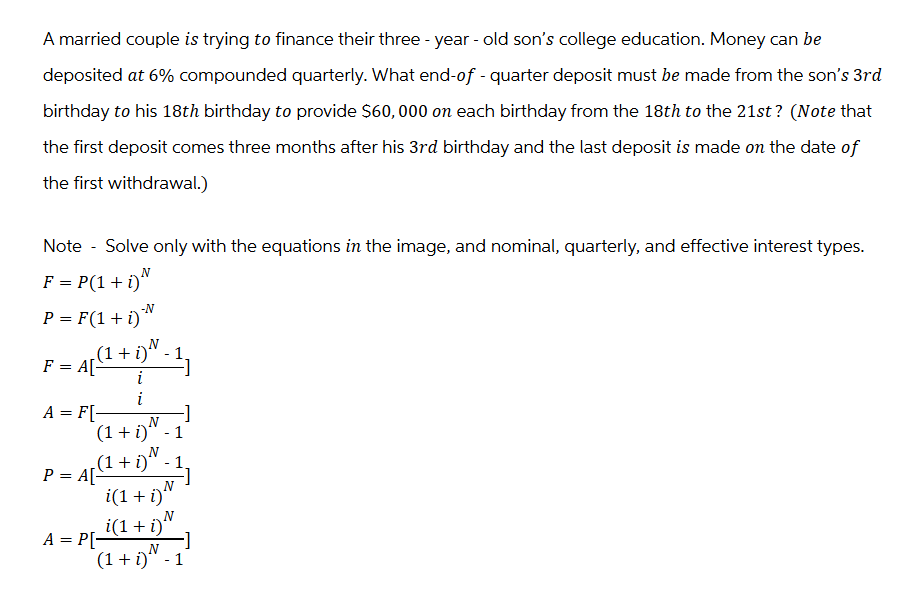

Act like a helpful tutor and exlain me : A married couple is trying to finance their three - year - old son's college education. Money can be

deposited at 6% compounded quarterly. What end-of - quarter deposit must be made from the son's 3rd

birthday to his 18th birthday to provide $60,000 on each birthday from the 18th to the 21st? (Note that

the first deposit comes three months after his 3rd birthday and the last deposit is made on the date of

the first withdrawal.)

Note - Solve only with the equations in the image, and nominal, quarterly, and effective interest types.

F=pP+D)"

P=Fa+i)"

~N

a+ 1

Foal

A=F———]

a+p¥-1

N

1+ -1

poait -t +1

(1+)

. ~N

1+

A= pt

a+p¥-1

A married couple is trying to finance their three - year - old son's college education. Money can be

deposited at 6% compounded quarterly. What end-of - quarter deposit must be made from the son's 3rd

birthday to his 18th birthday to provide $60,000 on each birthday from the 18th to the 21st? (Note that

the first deposit comes three months after his 3rd birthday and the last deposit is made on the date of

the first withdrawal.)

Note - Solve only with the equations in the image, and nominal, quarterly, and effective interest types.

F=pP+D)"

P=Fa+i)"

~N

a+ 1

Foal

A=F———]

a+p¥-1

N

1+ -1

poait -t +1

(1+)

. ~N

1+

A= pt

a+p¥-1

This is AI generated Response.

Asked by: Smart Tv

Created at: 2025-09-18 08:43:12

Asked by: Smart Tv

Created at: 2025-09-18 08:43:12

Final Answer:

Rendered

Raw Text

Did you like this answer?

Let's break down the problem and solve step by step using **only the given formulas**.

---

## **Step 1: Understanding the Problem**

- **Goal:** Find the end-of-quarter deposit amount, \( A \).

- **Deposits:** Start 3 months after son's 3rd birthday, end on his 18th birthday (inclusive).

- **Withdrawals:** $60,000 each on son's 18th, 19th, 20th, and 21st birthdays (4 equal annual withdrawals).

- **Interest:** 6% nominal annual, compounded quarterly.

---

## **Step 2: Key Parameters**

### **Interest Rate**

- **Nominal annual rate:** \( r = 6\% = 0.06 \)

- **Quarterly rate:** \( i = \frac{0.06}{4} = 0.015 \) per quarter

### **Deposits**

- **From:** 3 months after 3rd birthday, i.e., at age 3.25 years

- **To:** On 18th birthday, i.e., at age 18 years

- **Number of years depositing:** \( 18 - 3 = 15 \) years

- **Quarters:** \( 15 \times 4 = 60 \) deposits

### **Withdrawals**

- **$60,000 on each of the son's 18th, 19th, 20th, and 21st birthdays**

- **Time of first withdrawal:** Immediately after the last deposit

---

## **Step 3: Find Present Value Needed at Age 18**

At age 18, the account must have enough to pay four $60,000 annual withdrawals:

- These are at the beginning of each year (birthday), so treat as ordinary annuity (use \( F = A \left[\frac{(1+i)^N-1}{i}\right] \) if needed, but here, we use present value at the time of first withdrawal).

### **Quarterly Periods Between Withdrawals**

- 1 year = 4 quarters, so withdrawals are spaced by 4 quarters.

- Effective quarterly interest rate \( i = 0.015 \)

#### **Present Value at 18th Birthday**

Each $60,000 is withdrawn at 0, 4, 8, and 12 quarters from the 18th birthday.

\[

PV = 60,000 + \frac{60,000}{(1+i)^4} + \frac{60,000}{(1+i)^8} + \frac{60,000}{(1+i)^{12}}

\]

Calculate \( (1+i)^4 = (1.015)^4 \):

\[

(1.015)^4 \approx 1.06136

\]

\[

(1.06136)^2 = 1.1265 \quad \text{(for 8 quarters)}

\]

\[

(1.06136)^3 = 1.1956 \quad \text{(for 12 quarters)}

\]

So,

\[

PV = 60,000 + \frac{60,000}{1.06136} + \frac{60,000}{1.1265} + \frac{60,000}{1.1956}

\]

Calculate each term:

- \( 60,000/1.06136 \approx 56,546 \)

- \( 60,000/1.1265 \approx 53,282 \)

- \( 60,000/1.1956 \approx 50,194 \)

Sum:

\[

PV = 60,000 + 56,546 + 53,282 + 50,194 = 220,022

\]

---

## **Step 4: Find the Required Quarterly Deposit**

Now, we need the quarterly deposit \( A \) such that, after 60 deposits, the amount at the 18th birthday is $220,022.

Use the future value of an ordinary annuity formula (from the image):

\[

F = A \left[ \frac{(1+i)^N - 1}{i} \right]

\]

But we want \( A \), so rearrange (from the image):

\[

A = F \left[ \frac{i}{(1+i)^N - 1} \right]

\]

- \( F = 220,022 \)

- \( i = 0.015 \)

- \( N = 60 \)

First, calculate \( (1.015)^{60} \):

\[

\ln(1.015) \approx 0.01489

\]

\[

60 \times 0.01489 \approx 0.8934

\]

\[

e^{0.8934} \approx 2.443

\]

So,

\[

(1.015)^{60} \approx 2.443

\]

\[

(1.015)^{60} - 1 = 2.443 - 1 = 1.443

\]

Plug values into the formula:

\[

A = 220,022 \times \frac{0.015}{1.443}

\]

\[

A = 220,022 \times 0.0104 = 2,288

\]

---

## **Step 5: Final Answer**

\[

\boxed{A = \$2,288}

\]

**Explanation:**

To provide $60,000 on each birthday from the 18th to the 21st, the couple must deposit $2,288 at the end of each quarter from the son's 3rd birthday to his 18th birthday, assuming a nominal 6% annual interest rate compounded quarterly.

---

### **Summary Table**

| Step | Description | Value |

|------|-------------|-------|

| 1 | Quarterly interest rate | 0.015 |

| 2 | Number of deposits | 60 |

| 3 | Present value needed at 18 | $220,022 |

| 4 | Quarterly deposit | $\boxed{2,288}$ |

---

**Let me know if you need a more detailed explanation for any step!**

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :