Give step-by-step solution with explanation and final answer:Phoenix Incorporated, a cellular communication company, has multiple business units, organized as divisions. Each division's management is compensated based on the division's operating income. Division A currently purchases cellular equipment from outside markets and uses it to produce communication systems. Division B produces similar cellular equipment that it sells to outside customers—but not to Division A at this time. Division A's manager approaches Division B's manager with a proposal to buy the equipment from Division B. If it produces the cellular equipment that Division A desires, Division B will incur variable manufacturing costs of $60 per unit Relevant Information about Division B Sells 65.000 units of equipment to outside customers at $130 per unit Operating capacity is currently 80% the division can operate at 100% Variable manufacturing costs are $70 per unit Variable marketing costs are $8 per unit Fixed manufacturing costs are $700,000 Income per Unit for Division A (assuming parts purchased externally, not internally from division B) Sales revenue $320 Manufacturing costs Cellular equipnent a Other materials 10 Fixed costs 0 Total manufacturing costs 130 Gross margin 150 Marketing costs: Variable 35 Fixed 1 Total marketing costs so Operating income per unit 5 140 Required: 1. Division A proposes to buy 32,500 units from Division B at $75 per unit. What would be the effect of accepting this proposal on Division Bs operating income? What would be the effect on the operating income of Phoenix Incorporated as a whole? 2. Now suppose Division A could purchase from multiple suppliers and would accept partialshipment from Division B. How many units should Division B sell to Division A at $75 per unit, if any? What would be the effect on Division B's operating income? What would be the effect on the operating income of Phoenix Incorporated as a whole? 3. What is the range of transfer prices over which the divisional managers might negotiate a final transfer price? Complete this question by entering your answers in the tabs below. Required 1 | Required 2 Required 3 Division A proposes to buy 32,500 units from Division B at $75 per unit. What would be the effect of accepting this proposal on Division B's operating income? What would be the effect on the operating income of Phoenix Incorporated as a whole? Effect on division B's operating income Effect on firm's operating income

Question:

Give step-by-step solution with explanation and final answer:

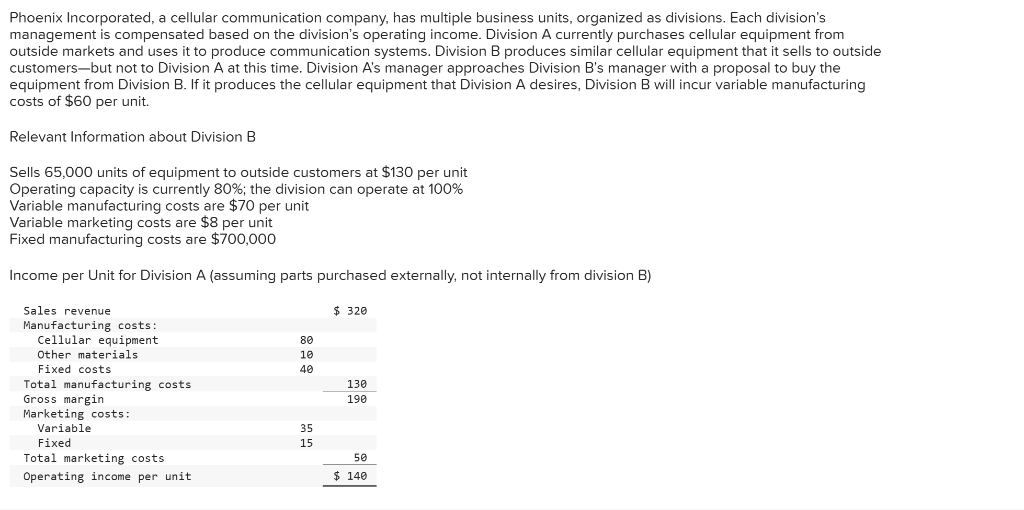

Phoenix Incorporated, a cellular communication company, has multiple business units, organized as divisions. Each division's

management is compensated based on the division's operating income. Division A currently purchases cellular equipment from

outside markets and uses it to produce communication systems. Division B produces similar cellular equipment that it sells to outside

customers—but not to Division A at this time. Division A's manager approaches Division B's manager with a proposal to buy the

equipment from Division B. If it produces the cellular equipment that Division A desires, Division B will incur variable manufacturing

costs of $60 per unit

Relevant Information about Division B

Sells 65.000 units of equipment to outside customers at $130 per unit

Operating capacity is currently 80% the division can operate at 100%

Variable manufacturing costs are $70 per unit

Variable marketing costs are $8 per unit

Fixed manufacturing costs are $700,000

Income per Unit for Division A (assuming parts purchased externally, not internally from division B)

Sales revenue $320

Manufacturing costs

Cellular equipnent a

Other materials 10

Fixed costs 0

Total manufacturing costs 130

Gross margin 150

Marketing costs:

Variable 35

Fixed 1

Total marketing costs so

Operating income per unit 5 140

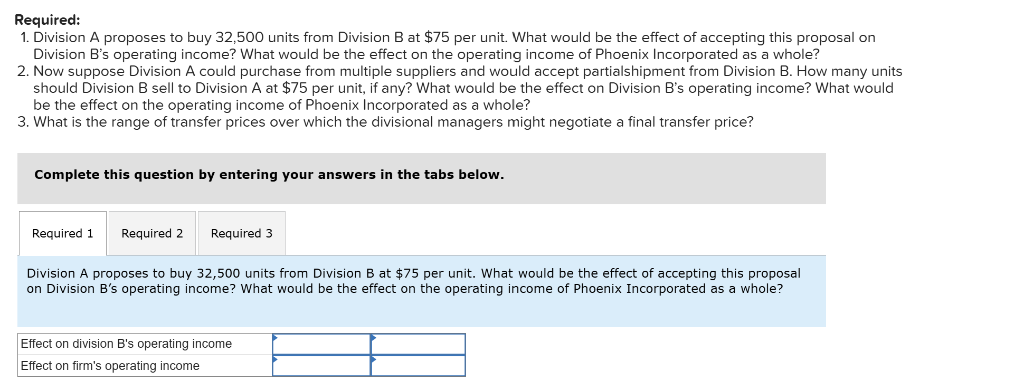

Required:

1. Division A proposes to buy 32,500 units from Division B at $75 per unit. What would be the effect of accepting this proposal on

Division Bs operating income? What would be the effect on the operating income of Phoenix Incorporated as a whole?

2. Now suppose Division A could purchase from multiple suppliers and would accept partialshipment from Division B. How many units

should Division B sell to Division A at $75 per unit, if any? What would be the effect on Division B's operating income? What would

be the effect on the operating income of Phoenix Incorporated as a whole?

3. What is the range of transfer prices over which the divisional managers might negotiate a final transfer price?

Complete this question by entering your answers in the tabs below.

Required 1 | Required 2 Required 3

Division A proposes to buy 32,500 units from Division B at $75 per unit. What would be the effect of accepting this proposal

on Division B's operating income? What would be the effect on the operating income of Phoenix Incorporated as a whole?

Effect on division B's operating income

Effect on firm's operating income

Phoenix Incorporated, a cellular communication company, has multiple business units, organized as divisions. Each division's

management is compensated based on the division's operating income. Division A currently purchases cellular equipment from

outside markets and uses it to produce communication systems. Division B produces similar cellular equipment that it sells to outside

customers—but not to Division A at this time. Division A's manager approaches Division B's manager with a proposal to buy the

equipment from Division B. If it produces the cellular equipment that Division A desires, Division B will incur variable manufacturing

costs of $60 per unit

Relevant Information about Division B

Sells 65.000 units of equipment to outside customers at $130 per unit

Operating capacity is currently 80% the division can operate at 100%

Variable manufacturing costs are $70 per unit

Variable marketing costs are $8 per unit

Fixed manufacturing costs are $700,000

Income per Unit for Division A (assuming parts purchased externally, not internally from division B)

Sales revenue $320

Manufacturing costs

Cellular equipnent a

Other materials 10

Fixed costs 0

Total manufacturing costs 130

Gross margin 150

Marketing costs:

Variable 35

Fixed 1

Total marketing costs so

Operating income per unit 5 140

Required:

1. Division A proposes to buy 32,500 units from Division B at $75 per unit. What would be the effect of accepting this proposal on

Division Bs operating income? What would be the effect on the operating income of Phoenix Incorporated as a whole?

2. Now suppose Division A could purchase from multiple suppliers and would accept partialshipment from Division B. How many units

should Division B sell to Division A at $75 per unit, if any? What would be the effect on Division B's operating income? What would

be the effect on the operating income of Phoenix Incorporated as a whole?

3. What is the range of transfer prices over which the divisional managers might negotiate a final transfer price?

Complete this question by entering your answers in the tabs below.

Required 1 | Required 2 Required 3

Division A proposes to buy 32,500 units from Division B at $75 per unit. What would be the effect of accepting this proposal

on Division B's operating income? What would be the effect on the operating income of Phoenix Incorporated as a whole?

Effect on division B's operating income

Effect on firm's operating income

Asked by: Shikhar

Created at: 2025-09-29 15:11:47

Thought Process:

Final Answer:

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :