Give step-by-step solution with explanation and final answer: Act like a helpful tutor and exlain me :Problem 4.32. The following table gives the prices of bonds Bond Principal (8) Time to Maturity (yrs) | Annual Coupon ($)* Bond Price ($) [wo 10 [00 [9% | *Half the stated coupon is paid every six months a) Calculate zero rates for maturities of 6 months, 12 months, 18 months, and 24 months. b) What are the forward rates for the periods: 6 months to 12 months, 12 months to 18 months, 18 months to 24 months? ¢) What are the 6-month, 12-month, 18-month, and 24-month par yields for bonds that provide semiannual coupon payments? d) Estimate the price and yield of a two-year bond providing a semiannual coupon of 7% per annum.

Question:

Give step-by-step solution with explanation and final answer:

Act like a helpful tutor and exlain me : Problem 4.32.

The following table gives the prices of bonds

Bond Principal (8) Time to Maturity (yrs) | Annual Coupon ($)* Bond Price ($)

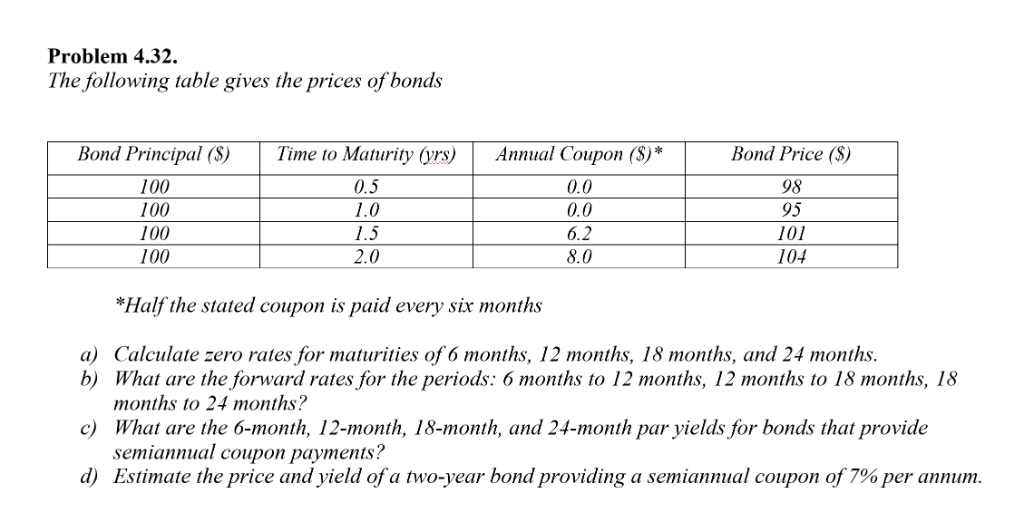

[wo 10 [00 [9% |

*Half the stated coupon is paid every six months

a) Calculate zero rates for maturities of 6 months, 12 months, 18 months, and 24 months.

b) What are the forward rates for the periods: 6 months to 12 months, 12 months to 18 months, 18

months to 24 months?

¢) What are the 6-month, 12-month, 18-month, and 24-month par yields for bonds that provide

semiannual coupon payments?

d) Estimate the price and yield of a two-year bond providing a semiannual coupon of 7% per annum.

Problem 4.32.

The following table gives the prices of bonds

Bond Principal (8) Time to Maturity (yrs) | Annual Coupon ($)* Bond Price ($)

[wo 10 [00 [9% |

*Half the stated coupon is paid every six months

a) Calculate zero rates for maturities of 6 months, 12 months, 18 months, and 24 months.

b) What are the forward rates for the periods: 6 months to 12 months, 12 months to 18 months, 18

months to 24 months?

¢) What are the 6-month, 12-month, 18-month, and 24-month par yields for bonds that provide

semiannual coupon payments?

d) Estimate the price and yield of a two-year bond providing a semiannual coupon of 7% per annum.

This is AI generated Response.

Asked by: Smart Tv

Created at: 2025-10-05 17:17:55

Asked by: Smart Tv

Created at: 2025-10-05 17:17:55

Final Answer:

Rendered

Raw Text

Did you like this answer?

Let's solve the problem step by step:

---

## **a) Calculate zero rates for 6, 12, 18, and 24 months**

**Zero-coupon bonds:**

- 6 months: Price = $98, Principal = $100, Coupon = $

- 12 months: Price = $95, Principal = $100, Coupon = $

### **Step 1: 6-Month Zero Rate**

For a zero-coupon bond, the price formula is:

\[

P = \frac{F}{(1 + r)^{n}}

\]

Where:

- \( P \) = Price now

- \( F \) = Face value ($100)

- \( r \) = periodic rate (for 6 months)

- \( n \) = number of periods (here, just 1 for 6 months)

\[

98 = \frac{100}{1 + r_{.5}}

\]

\[

1 + r_{.5} = \frac{100}{98} = 1.02041

\]

\[

r_{.5} = 2.041\%

\]

Annualized (compounded semiannually):

\[

\text{Zero rate for 6 months (annualized)} = 2 \times 2.041\% = 4.08\%

\]

---

### **Step 2: 12-Month Zero Rate**

\[

95 = \frac{100}{(1 + r_{1})^2}

\]

\[

(1 + r_{1})^2 = \frac{100}{95} = 1.05263

\]

\[

1 + r_{1} = \sqrt{1.05263} = 1.02596

\]

\[

r_{1} = 2.596\% \ \text{per 6 months}

\]

Annualized:

\[

\text{Zero rate for 12 months (annualized)} = 2 \times 2.596\% = 5.19\%

\]

---

### **Step 3: 18-Month Zero Rate**

The 1.5-year bond has a 6.2% coupon (paid semiannually: 3.1 every 6 months).

\[

\text{Cash flows: } 3.1 \ (\text{at 6, 12 months}), \ 103.1 \ (\text{at 18 months})

\]

The price is:

\[

101 = \frac{3.1}{1.02041} + \frac{3.1}{(1.02596)^2} + \frac{103.1}{(1 + r_{1.5})^3}

\]

Calculate present values of the first two coupons using earlier zero rates:

\[

\frac{3.1}{1.02041} = 3.038

\]

\[

\frac{3.1}{(1.02596)^2} = \frac{3.1}{1.05263} = 2.946

\]

So:

\[

101 = 3.038 + 2.946 + \frac{103.1}{(1 + r_{1.5})^3}

\]

\[

101 - 3.038 - 2.946 = \frac{103.1}{(1 + r_{1.5})^3}

\]

\[

95.016 = \frac{103.1}{(1 + r_{1.5})^3}

\]

\[

(1 + r_{1.5})^3 = \frac{103.1}{95.016} = 1.0852

\]

\[

1 + r_{1.5} = (1.0852)^{1/3} = 1.02764

\]

\[

r_{1.5} = 2.764\% \text{ per 6 months}

\]

Annualized:

\[

\text{Zero rate for 18 months (annualized)} = 2 \times 2.764\% = 5.53\%

\]

---

### **Step 4: 24-Month Zero Rate**

2-year bond: 8.% coupon (4. every 6 months), price = $104

\[

\text{Cash flows: } 4., 4., 4., 104. \text{ at 6, 12, 18, 24 months}

\]

\[

104 = \frac{4}{1.02041} + \frac{4}{(1.02596)^2} + \frac{4}{(1.02764)^3} + \frac{104}{(1 + r_2)^4}

\]

\[

\frac{4}{1.02041} = 3.922

\]

\[

\frac{4}{1.05263} = 3.801

\]

\[

\frac{4}{1.0852} = 3.687

\]

\[

104 = 3.922 + 3.801 + 3.687 + \frac{104}{(1 + r_2)^4}

\]

\[

104 - 3.922 - 3.801 - 3.687 = \frac{104}{(1 + r_2)^4}

\]

\[

92.59 = \frac{104}{(1 + r_2)^4}

\]

\[

(1 + r_2)^4 = \frac{104}{92.59} = 1.1232

\]

\[

1 + r_2 = (1.1232)^{1/4} = 1.02945

\]

\[

r_2 = 2.945\% \text{ per 6 months}

\]

Annualized:

\[

\text{Zero rate for 24 months (annualized)} = 2 \times 2.945\% = 5.89\%

\]

---

### **Summary Table**

| Maturity | Zero Rate (annualized, comp. semiannual) |

|------------|------------------------------------------|

| 6 months | 4.08% |

| 12 months | 5.19% |

| 18 months | 5.53% |

| 24 months | 5.89% |

---

## **b) Forward Rates**

The formula for the forward rate \( f \) from time \( t_1 \) to \( t_2 \) is:

\[

(1 + z_2)^{t_2} = (1 + z_1)^{t_1} \cdot (1 + f)^{t_2 - t_1}

\]

Where \( z_1 \) and \( z_2 \) are the zero rates for \( t_1 \) and \( t_2 \) (in periods of 6 months).

- \( z_1 \) for 6 months = 2.041% (per 6 months)

- \( z_2 \) for 12 months = 2.596% (per 6 months)

**Forward Rate from 6 to 12 months:**

\[

(1 + .02596)^2 = (1 + .02041)^1 \cdot (1 + f_{.5,1})^1

\]

\[

1.05263 = 1.02041 \cdot (1 + f_{.5,1})

\]

\[

(1 + f_{.5,1}) = \frac{1.05263}{1.02041} = 1.0316

\]

\[

f_{.5,1} = 3.16\% \text{ per 6 months}

\]

Annualized: 6.32%

---

**Forward Rate from 12 to 18 months:**

- \( z_1 \) for 12 months = 2.596%

- \( z_2 \) for 18 months = 2.764%

\[

(1 + .02764)^3 = (1 + .02596)^2 \cdot (1 + f_{1,1.5})^1

\]

\[

1.0852 = 1.05263 \cdot (1 + f_{1,1.5})

\]

\[

(1 + f_{1,1.5}) = \frac{1.0852}{1.05263} = 1.031

\]

\[

f_{1,1.5} = 3.10\% \text{ per 6 months}

\]

Annualized: 6.20%

---

**Forward Rate from 18 to 24 months:**

- \( z_1 \) for 18 months = 2.764%

- \( z_2 \) for 24 months = 2.945%

\[

(1 + .02945)^4 = (1 + .02764)^3 \cdot (1 + f_{1.5,2})^1

\]

\[

1.1232 = 1.0852 \cdot (1 + f_{1.5,2})

\]

\[

(1 + f_{1.5,2}) = \frac{1.1232}{1.0852} = 1.0351

\]

\[

f_{1.5,2} = 3.51\% \text{ per 6 months}

\]

Annualized: 7.02%

---

### **Summary Table**

| Period | Forward Rate (per 6 mo) | Annualized |

|--------------------|------------------------|-------------|

| 6 to 12 months | 3.16% | 6.32% |

| 12 to 18 months | 3.10% | 6.20% |

| 18 to 24 months | 3.51% | 7.02% |

---

## **c) Par Yields (6, 12, 18, 24 months)**

Par yield is the coupon rate that makes the bond price equal to face value ($100).

### **Formula:**

\[

P = \sum_{i=1}^{n} \frac{c}{(1 + z_i)^i} + \frac{100}{(1 + z_n)^n}

\]

Set \( P = 100 \) and solve for \( c \).

**Let’s do for each:**

---

### **6-month Par Yield**

\[

100 = \frac{c}{1.02041} + \frac{100}{1.02041}

\]

\[

100 = \frac{c + 100}{1.02041}

\]

\[

c + 100 = 100 \times 1.02041 = 102.041

\]

\[

c = 2.041

\]

Annual coupon = \( 2 \times 2.041 = 4.08\% \)

---

### **12-month Par Yield**

\[

100 = \frac{c}{1.02041} + \frac{c}{(1.02596)^2} + \frac{100}{(1.02596)^2}

\]

\[

(1.02596)^2 = 1.05263

\]

\[

100 = \frac{c}{1.02041} + \frac{c}{1.05263} + \frac{100}{1.05263}

\]

\[

100 = .980 + .950c + 95.

\]

Calculate each term:

\[

\frac{c}{1.02041} = .980c

\]

\[

\frac{c}{1.05263} = .950c

\]

\[

\frac{100}{1.05263} = 95.

\]

So,

\[

100 = .980c + .950c + 95.

\]

\[

100 - 95. = 1.93c

\]

\[

c = \frac{5.}{1.93} = 2.59

\]

Annual coupon = \( 2 \times 2.59 = 5.18\% \)

---

### **18-month Par Yield**

\[

100 = \frac{c}{1.02041} + \frac{c}{1.05263} + \frac{c}{1.0852} + \frac{100}{1.0852}

\]

\[

\frac{c}{1.02041} = .980c

\]

\[

\frac{c}{1.05263} = .950c

\]

\[

\frac{c}{1.0852} = .921c

\]

\[

\frac{100}{1.0852} = 92.18

\]

\[

100 = .980c + .950c + .921c + 92.18

\]

\[

100 - 92.18 = 2.851c

\]

\[

7.82 = 2.851c

\]

\[

c = \frac{7.82}{2.851} = 2.74

\]

Annual coupon = \( 2 \times 2.74 = 5.48\% \)

---

### **24-month Par Yield**

\[

100 = \frac{c}{1.02041} + \frac{c}{1.05263} + \frac{c}{1.0852} + \frac{c}{1.1232} + \frac{100}{1.1232}

\]

\[

\frac{c}{1.02041} = .980

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :