This is AI generated Response.

Asked by: Sandeep kumar

Created at: 2025-10-27 23:45:45

Final Answer:

RenderedRaw Text

Did you like this answer?

# Introduction

The questions involve understanding the financial transactions related to a partnership. The first question pertains to the calculation of ordinary income from a land sale, while the second involves determining the partnership interest after a property transfer, based on profit and loss sharing ratios.

---

# Step-by-step Solution

## Question 1:

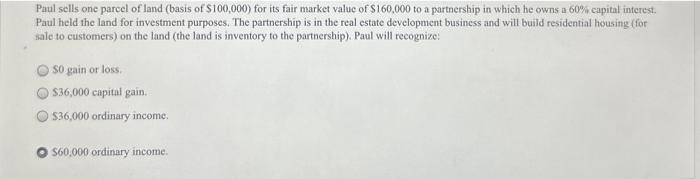

**"Paul sells one parcel of land (basis of $100,000) for its fair market value of $160,000 to a partnership in which he owns a 60% capital interest. Paul held the land for investment purposes. The partnership is in the real estate development business and will build residential housing (for sale to customers) on the land (the land is inventory to the partnership). Paul will recognize:"**

### Step 1: Determine capital gain or loss

- **Selling price of land**: $160,000

- **Basis of land**: $100,000

- **Gain on sale**: $160,000 - $100,000 = **$60,000**

### Step 2: Determine the nature of the gain

- Since Paul held the land for investment purposes and is now selling it to a partnership that develops the land, the gain is considered **ordinary income** if the land is inventory or held for resale in the ordinary course of business.

- The problem states the partnership will build residential housing on land inventory, implying the land is inventory, and thus, the gain is **ordinary income**.

### **Final answer**:

**$60,000 ordinary income**

---

## Question 2:

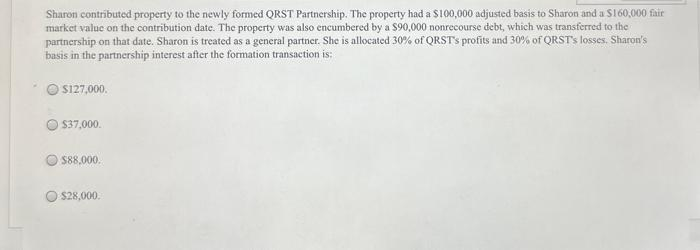

**"Sharon contributed property to the newly formed QRST Partnership. The property had a $100,000 adjusted basis to Sharon and a $160,000 fair market value at contribution. The property was also encumbered by a $90,000 nonrecourse debt transferred to the partnership. Sharon is allocated 30% of QRST’s profits and losses. After the formation transaction, Sharon’s basis in the partnership interest is:"**

### Step 1: Calculate Sharon's initial basis in the property

- Basis of property: **$100,000**

### Step 2: Adjust basis for debt transferred

- Nonrecourse debt transferred: **$90,000**

- Sharon's share of debt: 30%

- Sharon's share of debt: 30% of $90,000 = **$27,000**

### Step 3: Determine basis in partnership interest

- Starting basis (property basis): $100,000

- Add Sharon’s share of debt transferred: +$27,000

- **Sharon's initial basis in partnership**: $100,000 + $27,000 = **$127,000**

### **Final answer**:

**$127,000**

---

# **Summary**

- In the first question, Paul’s sale of land held for investment results in a **$60,000 ordinary income**.

- In the second question, Sharon’s basis in the partnership interest after contributing property with associated debt is **$127,000**.

---

**Note:** These solutions assume standard tax rules and the data provided.

Question:

need explanation of above questions answers

This is AI generated Response.

Asked by: Sandeep kumar

Created at: 2025-10-27 23:46:59

Final Answer:

RenderedRaw Text

Did you like this answer?

# Explanation of Answers

## Question 1 Explanation

Paul's transaction involves the sale of land to a partnership. Here’s a breakdown of the reasoning behind the calculations:

1. **Capital Gain Calculation**:

- **Basis of Land**: This is the amount Paul originally invested in the land, which is $100,000.

- **Fair Market Value (FMV)**: The land was sold for $160,000.

- **Gain Realized**: The gain from the sale is calculated as:

\[

\text{Gain} = \text{Selling Price} - \text{Basis} = 160,000 - 100,000 = 60,000

\]

2. **Nature of Gain**:

- Since the partnership is involved in real estate development and the land will be treated as inventory (for resale), the gain is classified as ordinary income rather than capital gain. This is because the land is sold in the ordinary course of business.

Thus, Paul recognizes **$60,000 ordinary income** from this transaction.

---

## Question 2 Explanation

Sharon's contribution of property to the partnership involves calculating her basis in the partnership interest, considering both the property's basis and the debt associated with it.

1. **Initial Basis of Property**:

- Sharon’s original basis in the contributed property is **$100,000**.

2. **Debt Consideration**:

- The property was encumbered by a **$90,000 nonrecourse debt**.

- When the property is contributed to the partnership, Sharon is allocated a share of this debt based on her profit and loss sharing ratio (30%).

- **Sharon’s Share of Debt**:

\[

\text{Sharon's Debt Share} = 0.30 \times 90,000 = 27,000

\]

3. **Calculating Basis in Partnership Interest**:

- Sharon's basis in her partnership interest after the contribution is calculated as follows:

\[

\text{Basis in Partnership} = \text{Initial Property Basis} + \text{Sharon's Share of Debt}

\]

\[

\text{Basis in Partnership} = 100,000 + 27,000 = 127,000

\]

Therefore, Sharon’s basis in the partnership interest after the formation transaction is **$127,000**.

---

# Summary of Key Points

- In the first case, the ordinary income realization is due to the nature of the business activity (land as inventory).

- In the second case, the basis calculation incorporates the original property basis and the partner's share of the debt, essential for determining the partner's financial stake in the partnership.

This detailed explanation clarifies how each figure is derived and the underlying principles guiding the taxation of these transactions.

VIPSolutions focuses on clear, step‑by‑step explanations so you can learn quickly. Whether you need an AI‑generated walkthrough or a short hint to get unstuck, each solution is organized for fast reading and easy review later.

Search similar questions, compare approaches, and bookmark the best answers for revision. Our goal is simple: quick, reliable study help that feels natural—not noisy.

Paull sells one parcel of land (basis of $100,000) for its fair market valu of $160,000 to a partnership in which he owns a 60% capital interest.

Paul held the land for investment purposes, The partnership sin the eal tae development business and will build residential housing (for

salle 0 customers) on the and (he and s inventory to the partnership). Paul will recognize

© 30 gain or loss

© $36,000 capital gain.

(© 536,000 ordinary income.

© $60,000 ordinary income

‘Sharon contributed property 0 he newly formed QRST Parnership. The property had $100,000 adjusted basis t Sharon and $160,000 ie

‘marke value on the contribution dat. The property was aio rcumbercd by a 0,000 nonrecourse deb, which was transfered 0 the

partnership on that date. Sharon i treated a a general partner. She salocaed 30% of QRST' profits and 30% of QRSTs losses. Sharo's

| basisin the parmnership interest afr th formation transaction is |

| osm.

© 537.000.

© 388.000.

© 526,000.

Paull sells one parcel of land (basis of $100,000) for its fair market valu of $160,000 to a partnership in which he owns a 60% capital interest.

Paul held the land for investment purposes, The partnership sin the eal tae development business and will build residential housing (for

salle 0 customers) on the and (he and s inventory to the partnership). Paul will recognize

© 30 gain or loss

© $36,000 capital gain.

(© 536,000 ordinary income.

© $60,000 ordinary income

‘Sharon contributed property 0 he newly formed QRST Parnership. The property had $100,000 adjusted basis t Sharon and $160,000 ie

‘marke value on the contribution dat. The property was aio rcumbercd by a 0,000 nonrecourse deb, which was transfered 0 the

partnership on that date. Sharon i treated a a general partner. She salocaed 30% of QRST' profits and 30% of QRSTs losses. Sharo's

| basisin the parmnership interest afr th formation transaction is |

| osm.

© 537.000.

© 388.000.

© 526,000.