QUESTION 1 ( 2 5 marks ) Using the relevant information provided in the case study, prepare the following for Established Manufacturers ( Pty ) Ltd: 1 . 1 A Debtors scheduled for November 2 0 2 5 , December 2 0 2 5 , and January 2 0 2 6 ( 5 marks ) 1 . 2 A Cash flow projection for November 2 0 2 5 , December 2 0 2 5 , and January 2 0 2 6 ( 2 0 marks ) Statement of Financial Position as of 3 0 June 2 0 2 5 Assets Property, Plant, and Equipment Cash and Cash Equivalents Total Equity and Liabilities The Road Ahead Looking forward to the next financial year, the management team identified opportunities and challenges. Sales were evenly distributed over the past 1 2 months and are expected to grow by 5 % in the next financial year, while the cost of sales remains constant at 6 5 % of total sales revenue. Cost pressures are real in the current economy and the following have been identified: Salaries and Wages were incurred evenly throughout the year. However, this is expected to increase by 4 . 2 5 % after the anticipated industry - wide union negotiations in October Rent is paid quarterly, with the annual 1 0 % increase effective 1 January 2 0 2 6 . Insurance premiums are paid monthly and increase by 8 % on 1 July, each year. Due to planned changes in Established Manufacturers' credit policy, the total value of debtors is expected to double in the financial year. However, the 4 5 - day payment terms granted to debtors will remain, despite the widely varying payment patterns. 5 0 % of credit sales are collected within 3 0 days. 3 0 % are collected within 6 0 days. 5 % are written off as bad debts. 1 5 % of sales are cash sales, with a 1 % discount offered. Purchases are linked to sales, with monthly purchases equal to 5 0 % of monthly sales. 6 5 % of purchases are made on credit, with 6 0 - day payment terms. The balance is paid for in cash. The total trade creditors at the end of the financial year are envisaged to increase by R 4 . 4 m YOY, while the opening inventory as of 1 July 2 0 2 6 is expected to be R 1 m more than 1 July 2 0 2 5 . A new project will commence in January 2 0 2 6 , with a capital investment of R 1 . 2 million to be made in a new truck. While a 1 2 % cash deposit is required 3 0 days prior, the first repayment for the truck will be on 1 July 2 0 2 6 . Old equipment with a zero - book value will be sold in October 2 0 2 5 for R 8 0 0 , 0 0 0 , with payment terms of 3 0 days after the sale. The company maintains a depreciation policy of 1 0 % per annum on a straight - line basis. The short - term loan will be extinguished by October 2 0 2 5 , while the term loan with Home Bank has an annual repayment of R 5 m due on 3 1 March 2 0 2 6 . The total interest expense for FYE 2 0 2 6 is expected to rise by 6 % Based on the review and discussion, the CFO projected an unfavourable bank balance of R 1 8 3 7 3 5 0 at the end of October 2 0 2 5 . He also mentioned that given the loyalty and support of the shareholders, it is anticipated a dividend of 6 5 cents per share will be declared and paid out in theCASE STUDY Information Established Manufacturers (Pty) Ltd is a South African company specialising in producing and distributing electronic components. The company operates in a highly competitive market and sells its products locally and internationally. The year has been particularly eventful for the company, filled with growth, challenges, and critical decisions that will shape its financial future. | Reflections on the Past Year The management team, led by CEO Mr Dlamini, reviewed the company’s performance and presented the financial statements for Established Manufacturers (Pty) Ltd for the year ended 30 June 2025: Income Statement for the Year Ended 30 June 2025 Amount (R'000) EE 120000 Cost of Sales (78,000) Operating Expenses EE +200 oo%0 Salaries and Wages 15,000 EN hi Operating Profit 11,706 0199 Profi Before Tex EN Income Tax Expense (2,565) (30%) Position as of 30 June 2025 Assets Equipment Equivalents Liabilities The Road Ahead Looking forward to the next financial year, the management team identified opportunities and challenges. Sales were evenly distributed over the past 12 months and are expected to grow by 5% in the next financial year, while the cost of sales remains constant at 65% of total sales revenue. Cost pressures are real in the current economy and the following have been identified: Salaries and Wages were incurred evenly throughout the year. However, this is expected to increase by 4.25% after the anticipated industry-wide union negotiations in October 2025. Rent is paid quarterly, with the annual 10% increase effective 1 January 2026. Insurance premiums are paid monthly and increase by 8% on 1 July, each year. Due to planned changes in Established Manufacturers’ credit policy, the total value of debtors is expected to double in the financial year. However, the 45-day payment terms granted to debtors will remain, despite the widely varying payment patterns. + 50% of credit sales are collected within 30 days. + 30%are collected within 60 days. + S%are written off as bad debts. + 15%of sales are cash sales, with a 1% discount offered. Purchases are linked to sales, with monthly purchases equal to 50% of monthly sales. 65% of purchases are made on credit, with 60-day payment terms. The balance is paid forin cash. The total trade creditors at the end of the financial year are envisaged to increase by R4.4m YOY, while the opening inventory as of 1 July 2026 is expected to be RTm more than 1 July 2025. Anew project will commence in January 2026, with a capital investment of R1.2 million to be made in a new truck. While a 12% cash deposit is required 30 days prior, the first repayment for the truck will be on 1 July 2026. Old equipment with a zero-book value will be sold in October 2025 for R800,000, with payment terms of 30 days after the sale. The company maintains a depreciation policy of 10% per annum on a straight-line basis. The short-term loan will be extinguished by October 2025, while the term loan with Home Bank has an annual repayment of R5m due on 31 March 2026 ‘I'he total interest expense Tor FYE 2026 is expected to rise by 6% Based on the review and discussion, the CFO projected an unfavourable bank balance of R1837 350 at the end of October 2025. He also mentioned that given the loyalty and support of the shareholders, it is anticipated a dividend of 65 cents per share will be declared and paid out in the financial year. Established Manufacturers (Pty) Ltd has an authorised share capital of 800 000 ordinary shares of which 690 000 have been issued.

Question:

QUESTION

1

(

2

5

marks

)

Using the relevant information provided in the case study, prepare the following for Established Manufacturers

(

Pty

)

Ltd:

1

.

1

A Debtors scheduled for November

2

0

2

5

,

December

2

0

2

5

,

and January

2

0

2

6

(

5

marks

)

1

.

2

A Cash flow projection for November

2

0

2

5

,

December

2

0

2

5

,

and January

2

0

2

6

(

2

0

marks

)

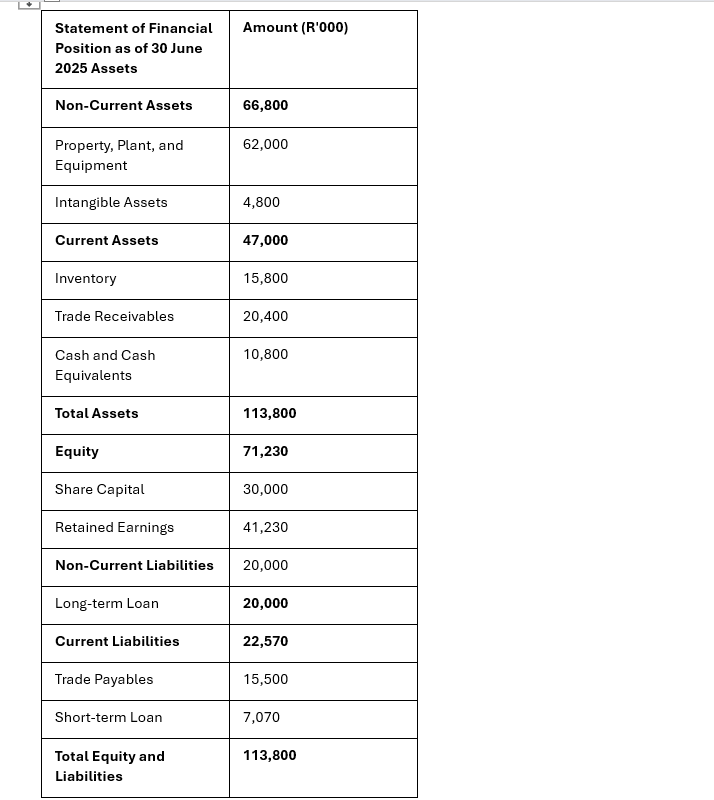

Statement of Financial Position as of

3

0

June

2

0

2

5

Assets Property, Plant, and Equipment Cash and Cash Equivalents Total Equity and Liabilities The Road Ahead Looking forward to the next financial year, the management team identified opportunities and challenges. Sales were evenly distributed over the past

1

2

months and are expected to grow by

5

%

in the next financial year, while the cost of sales remains constant at

6

5

%

of total sales revenue. Cost pressures are real in the current economy and the following have been identified: Salaries and Wages were incurred evenly throughout the year. However, this is expected to increase by

4

.

2

5

%

after the anticipated industry

-

wide union negotiations in October Rent is paid quarterly, with the annual

1

0

%

increase effective

1

January

2

0

2

6

.

Insurance premiums are paid monthly and increase by

8

%

on

1

July, each year. Due to planned changes in Established Manufacturers' credit policy, the total value of debtors is expected to double in the financial year. However, the

4

5

-

day payment terms granted to debtors will remain, despite the widely varying payment patterns.

5

0

%

of credit sales are collected within

3

0

days.

3

0

%

are collected within

6

0

days.

5

%

are written off as bad debts.

1

5

%

of sales are cash sales, with a

1

%

discount offered. Purchases are linked to sales, with monthly purchases equal to

5

0

%

of monthly sales.

6

5

%

of purchases are made on credit, with

6

0

-

day payment terms. The balance is paid for in cash. The total trade creditors at the end of the financial year are envisaged to increase by R

4

.

4

m YOY, while the opening inventory as of

1

July

2

0

2

6

is expected to be R

1

m more than

1

July

2

0

2

5

.

A new project will commence in January

2

0

2

6

,

with a capital investment of R

1

.

2

million to be made in a new truck. While a

1

2

%

cash deposit is required

3

0

days prior, the first repayment for the truck will be on

1

July

2

0

2

6

.

Old equipment with a zero

-

book value will be sold in October

2

0

2

5

for R

8

0

0

,

0

0

0

,

with payment terms of

3

0

days after the sale. The company maintains a depreciation policy of

1

0

%

per annum on a straight

-

line basis. The short

-

term loan will be extinguished by October

2

0

2

5

,

while the term loan with Home Bank has an annual repayment of R

5

m due on

3

1

March

2

0

2

6

.

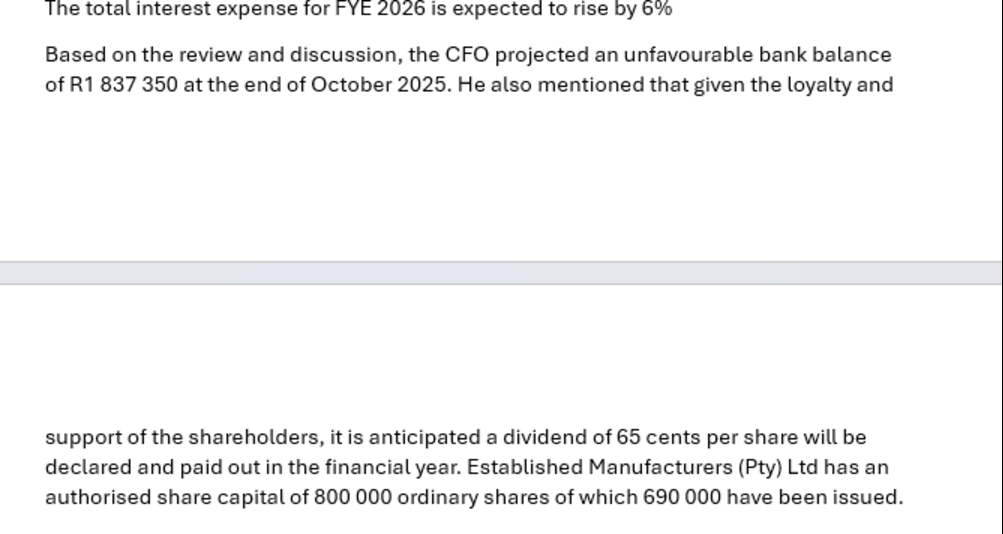

The total interest expense for FYE

2

0

2

6

is expected to rise by

6

%

Based on the review and discussion, the CFO projected an unfavourable bank balance of R

1

8

3

7

3

5

0

at the end of October

2

0

2

5

.

He also mentioned that given the loyalty and support of the shareholders, it is anticipated a dividend of

6

5

cents per share will be declared and paid out in the

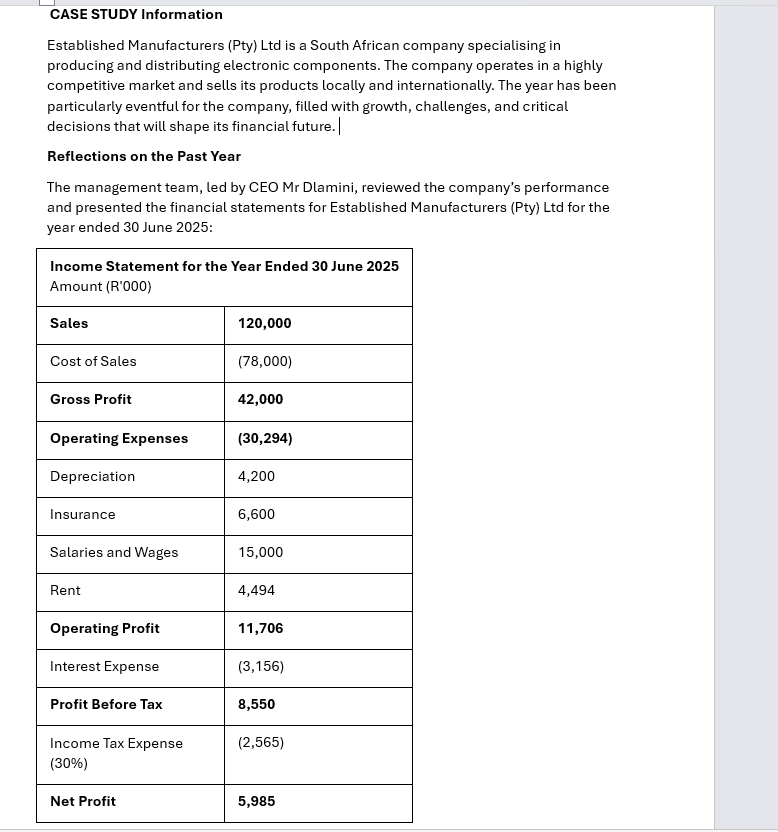

CASE STUDY Information

Established Manufacturers (Pty) Ltd is a South African company specialising in

producing and distributing electronic components. The company operates in a highly

competitive market and sells its products locally and internationally. The year has been

particularly eventful for the company, filled with growth, challenges, and critical

decisions that will shape its financial future. |

Reflections on the Past Year

The management team, led by CEO Mr Dlamini, reviewed the company’s performance

and presented the financial statements for Established Manufacturers (Pty) Ltd for the

year ended 30 June 2025:

Income Statement for the Year Ended 30 June 2025

Amount (R'000)

EE 120000

Cost of Sales (78,000)

Operating Expenses EE

+200

oo%0

Salaries and Wages 15,000

EN hi

Operating Profit 11,706

0199

Profi Before Tex EN

Income Tax Expense (2,565)

(30%)

Position as of 30 June

2025 Assets

Equipment

Equivalents

Liabilities

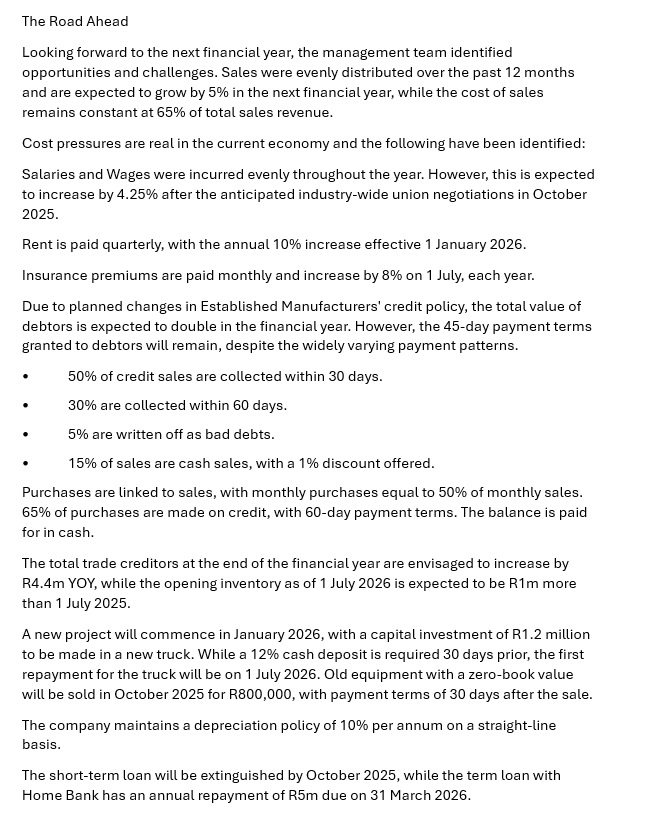

The Road Ahead

Looking forward to the next financial year, the management team identified

opportunities and challenges. Sales were evenly distributed over the past 12 months

and are expected to grow by 5% in the next financial year, while the cost of sales

remains constant at 65% of total sales revenue.

Cost pressures are real in the current economy and the following have been identified:

Salaries and Wages were incurred evenly throughout the year. However, this is expected

to increase by 4.25% after the anticipated industry-wide union negotiations in October

2025.

Rent is paid quarterly, with the annual 10% increase effective 1 January 2026.

Insurance premiums are paid monthly and increase by 8% on 1 July, each year.

Due to planned changes in Established Manufacturers’ credit policy, the total value of

debtors is expected to double in the financial year. However, the 45-day payment terms

granted to debtors will remain, despite the widely varying payment patterns.

+ 50% of credit sales are collected within 30 days.

+ 30%are collected within 60 days.

+ S%are written off as bad debts.

+ 15%of sales are cash sales, with a 1% discount offered.

Purchases are linked to sales, with monthly purchases equal to 50% of monthly sales.

65% of purchases are made on credit, with 60-day payment terms. The balance is paid

forin cash.

The total trade creditors at the end of the financial year are envisaged to increase by

R4.4m YOY, while the opening inventory as of 1 July 2026 is expected to be RTm more

than 1 July 2025.

Anew project will commence in January 2026, with a capital investment of R1.2 million

to be made in a new truck. While a 12% cash deposit is required 30 days prior, the first

repayment for the truck will be on 1 July 2026. Old equipment with a zero-book value

will be sold in October 2025 for R800,000, with payment terms of 30 days after the sale.

The company maintains a depreciation policy of 10% per annum on a straight-line

basis.

The short-term loan will be extinguished by October 2025, while the term loan with

Home Bank has an annual repayment of R5m due on 31 March 2026

‘I'he total interest expense Tor FYE 2026 is expected to rise by 6%

Based on the review and discussion, the CFO projected an unfavourable bank balance

of R1837 350 at the end of October 2025. He also mentioned that given the loyalty and

support of the shareholders, it is anticipated a dividend of 65 cents per share will be

declared and paid out in the financial year. Established Manufacturers (Pty) Ltd has an

authorised share capital of 800 000 ordinary shares of which 690 000 have been issued.

CASE STUDY Information

Established Manufacturers (Pty) Ltd is a South African company specialising in

producing and distributing electronic components. The company operates in a highly

competitive market and sells its products locally and internationally. The year has been

particularly eventful for the company, filled with growth, challenges, and critical

decisions that will shape its financial future. |

Reflections on the Past Year

The management team, led by CEO Mr Dlamini, reviewed the company’s performance

and presented the financial statements for Established Manufacturers (Pty) Ltd for the

year ended 30 June 2025:

Income Statement for the Year Ended 30 June 2025

Amount (R'000)

EE 120000

Cost of Sales (78,000)

Operating Expenses EE

+200

oo%0

Salaries and Wages 15,000

EN hi

Operating Profit 11,706

0199

Profi Before Tex EN

Income Tax Expense (2,565)

(30%)

Position as of 30 June

2025 Assets

Equipment

Equivalents

Liabilities

The Road Ahead

Looking forward to the next financial year, the management team identified

opportunities and challenges. Sales were evenly distributed over the past 12 months

and are expected to grow by 5% in the next financial year, while the cost of sales

remains constant at 65% of total sales revenue.

Cost pressures are real in the current economy and the following have been identified:

Salaries and Wages were incurred evenly throughout the year. However, this is expected

to increase by 4.25% after the anticipated industry-wide union negotiations in October

2025.

Rent is paid quarterly, with the annual 10% increase effective 1 January 2026.

Insurance premiums are paid monthly and increase by 8% on 1 July, each year.

Due to planned changes in Established Manufacturers’ credit policy, the total value of

debtors is expected to double in the financial year. However, the 45-day payment terms

granted to debtors will remain, despite the widely varying payment patterns.

+ 50% of credit sales are collected within 30 days.

+ 30%are collected within 60 days.

+ S%are written off as bad debts.

+ 15%of sales are cash sales, with a 1% discount offered.

Purchases are linked to sales, with monthly purchases equal to 50% of monthly sales.

65% of purchases are made on credit, with 60-day payment terms. The balance is paid

forin cash.

The total trade creditors at the end of the financial year are envisaged to increase by

R4.4m YOY, while the opening inventory as of 1 July 2026 is expected to be RTm more

than 1 July 2025.

Anew project will commence in January 2026, with a capital investment of R1.2 million

to be made in a new truck. While a 12% cash deposit is required 30 days prior, the first

repayment for the truck will be on 1 July 2026. Old equipment with a zero-book value

will be sold in October 2025 for R800,000, with payment terms of 30 days after the sale.

The company maintains a depreciation policy of 10% per annum on a straight-line

basis.

The short-term loan will be extinguished by October 2025, while the term loan with

Home Bank has an annual repayment of R5m due on 31 March 2026

‘I'he total interest expense Tor FYE 2026 is expected to rise by 6%

Based on the review and discussion, the CFO projected an unfavourable bank balance

of R1837 350 at the end of October 2025. He also mentioned that given the loyalty and

support of the shareholders, it is anticipated a dividend of 65 cents per share will be

declared and paid out in the financial year. Established Manufacturers (Pty) Ltd has an

authorised share capital of 800 000 ordinary shares of which 690 000 have been issued.

Asked by: REDDY BHARGAVA SURYA TEJA

Created at: 2025-11-16 16:14:56

Final Answer:

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :