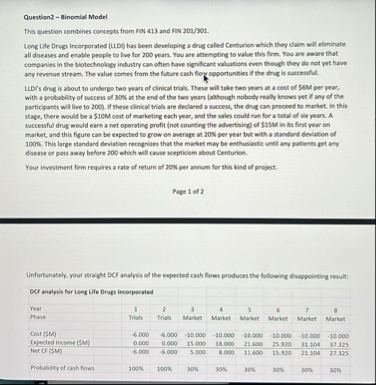

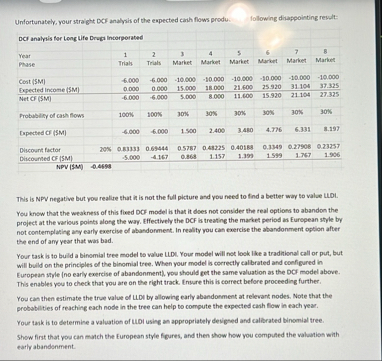

Questlion 2 - Einomial Model This question combines concepts from FIN 4 1 3 and FIN 2 0 1 / 3 0 1 . Long Ule Drugs Incorporabed ( LUDi ) has been developing a drug called Centurion which they claim will eliminate al diseases and enable people to live for 2 0 0 years. Fou are attempting to value this frm . Yow are aware that comparies in the biobedhnologr industry can often have signilicant waluations even though they do not yet have any reverve stream. The value comes from the future cash flow opportumities If the drag is successful. LLD ' s é rug is about to undergo two years of clinical triah. These will take two years at a cost of SEM per year, with a probability of succens of 3 0 % at the end of the two pears ( although nobody really lonows yet if any of the participants will live to 2 0 0 ) . If these clinical trials are declared a success, the drug can proceed to market. In this stage, there would be a $ 1 0 M cost of marketing rach year, and the sales could run for a total of sky years. A succenful drug would eurn a net operating problit ( not counting the advertising ) of $ 1 5 M in its frist year of market, and this figure can be expected to grew on average at 2 0 % per year but with a standard deviation of 1 0 0 K . This large standard deviation recogibes that the market may be enthuslastic until any patients get any disease or pass away before 2 0 0 which will cause soepticism about Centurion. Four investment from requires a rate ef return of 2 0 K per annum for this kind of project. Page 1 ell 2 Unfortunately, your struighe DCI unalyis of the expected canh flows produces the following disappointing result: \ table [ [ DCF analysls for Lang Ufe Brups lacerpereted ] , [ Tear , , 1 , 2 , 3 , 4 , 5 , 6 , 7 , 8 ] , [ Phase , , Trialis,Triah,Marlast,Market,Market,Marlast,Market,Market ] , [ Cent ( SIM ) , , - 4 . 0 0 0 , - 4 . 0 0 0 , - 1 0 . 0 0 0 , 2 0 . 0 0 0 , - 1 0 . 0 0 0 , - 1 0 . 0 0 0 , - 1 0 . 0 0 0 , - 1 0 . 0 0 0 ] , [ Expected linotome [ SM ] , , 0 . 0 0 0 , 0 . 0 0 0 , 1 5 . 0 0 0 , 3 8 . 0 0 0 , 7 1 . 4 0 0 , H . 9 9 5 , 1 1 . 9 5 4 , KP - 3 2 5 ] , [ Net CF [ FM ] , , - 6 0 0 0 , 4 0 0 0 , 5 . 0 0 9 , 8 0 0 0 , 1 1 . 4 0 0 , 1 5 . 5 2 0 , 2 1 . 1 0 4 , 2 7 . 3 2 5 ] , [ Frobability of canh fown,, 1 5 0 % , 1 0 0 % , 1 0 % , 3 0 % , HOS, 1 0 % , 3 0 % , 1 9 9 4 ] , [ Expented OP ( TM ) , , 4 . 0 0 0 , - 4 . 0 0 0 , 1 . 5 0 0 , 2 . 4 0 0 , 3 . 4 8 0 , 4 . 7 7 6 , 6 . 3 3 1 , 8 . 5 9 7 ] , [ Diabount flactor, 2 0 % , 0 . 0 3 3 3 3 , 0 . 6 9 4 4 , 0 . 5 7 8 7 , 0 . 4 0 2 2 5 , 0 . 0 0 1 2 8 , d . 3 3 4 9 , 0 . 2 9 9 0 8 , D . 2 . 2 5 . 5 ] , [ Diacounted CF ( 5 M ) , , - 5 0 0 6 , - 4 . 1 6 7 , 0 . 2 5 8 , 1 . 2 5 3 , 3 . 1 1 9 , 1 5 9 9 , 1 7 5 7 , 1 . 5 0 5 ] , [ NAV ( 5 M ) , - 6 . 4 6 0 8 , , , , , , , , ] ] propect at the various points along the way. Ulectlarly the DCI in treathy the market period as Europens style by the end of any pear that wan bad. Four tank in to buld a binomial tree model to value LUDL. Your model wil not look like a truditional call or pue, but Question 2 - Binomial Model This question combines concepts from FN 4 1 3 and FIN 2 0 1 / 3 0 1 . Long Life Drugs Incorporated ( L . LD ) has been developing a drug cafled Centurion which they claim will eliminate all diseases and enable people to live for 2 0 0 years. You are attempting to value this firm. Fou are aware that companies in the blotechnology industry can often have significant valuations even though they do not yet have any revenue stream. The value comes from the flute cash flog opportunities if the drug is successful. LLDI's drug is about to undergo two years of clinical trials. These will take two wars at a cost of $ 6 M per year, with a probability of success of 3 0 % at the end of the two years ( although nobody really knows yet if any of the participants will live to 2 0 0 ) . If these clinical trials are declared a success, the dnig can proceed to market. In this stage, there would be a $ 1 0 M cost of marketing each year, and the sales could run for a total ell six years. A successful drug would earn a net operating profit ( not counting the advertining ) of $ 1 5 M in ils finit war on market, and this figure can be expected to grow on average at 2 0 % per year but with a standard deviation of 1 0 0 % . This large standard deviation recognites that the market may be enthuslastic until any patients get any disease or pass away before 2 0 0 which will cause scepticism about Cenfurion. Your investment firm requires a rate of return of 2 0 % per annum for this lind of project. Page 1 of 2 Unfortunately, your straight DCF analyis of the expected cash flows produces the following disappointing result: \ table [ [ BES anatyls for teng Life Drugs Incorporated,,,,,, ] , [ Year , 1 , 2 , 3 , 4 , 5 , 6 , 7 , 8 ] , [ Pharie , Trials,Trials,Market,Market,Market,Market,Marhet,Market ] , [ Cont ( $M ) , 6 . 0 0 0 , - 6 . 0 0 0 , - 1 0 . 0 0 0 , - 3 0 . 0 0 0 , - 1 0 . 0 0 0 , - 1 0 . 0 0 0 , - 1 0 . 0 0 0 , - 1 0 . 0 0 0 ] , [ Espected income ( SU ) , 0 . 0 0 0 , 0 . 0 0 0 , 1 5 . 0 0 0 , 1 8 . 0 0 0 , 2 1 . 6 0 0 , 2 5 . 9 3 0 , 3 1 . 1 0 4 , 3 7 . 3 2 5 ] , [ Net CF ( $M ) , 6 . 0 0 0 , - 6 . 0 0 0 , $ . 0 0 0 , 8 . 0 0 0 , 1 1 . 6 0 0 , 1 5 . 9 2 0 , 2 1 . 1 0 4 , 2 7 . 3 2 5 ] , [ Probability of cash flows, 1 0 0 % , 1 0 0 % , 3 0 % , 3 0 % , 3 0 % , 3 0 % , 3 0 4 , 1 0 % ] ] Unfortunately, your straight DCF analysis of the expected cash flows produ. following dirappointing result: \ table [ [ BCI analysis for Long Uife Draga Interporated,,,,,, ] , [ Year Plase,, 1 Trials, 2 Triaee Ee et ementnias rete ed bret Er eet ty ee mt ee er tre EE Ee) TTR oreo vt rg mf ied opt. oan gin emia ew tes bE Nm NE MSMR E foretr Te te CT he i Te i To gm Te en toe tv. ct ome cy hd tps ee eee a Ser 50 [APTPEP—————E——— St tye mh ergo te 1 oo td hi

Question:

Questlion

2

-

Einomial Model

This question combines concepts from FIN

4

1

3

and FIN

2

0

1

/

3

0

1

.

Long Ule Drugs Incorporabed

(

LUDi

)

has been developing a drug called Centurion which they claim will eliminate al diseases and enable people to live for

2

0

0

years. Fou are attempting to value this frm

.

Yow are aware that comparies in the biobedhnologr industry can often have signilicant waluations even though they do not yet have any reverve stream. The value comes from the future cash flow opportumities If the drag is successful.

LLD

'

s

é

rug is about to undergo two years of clinical triah. These will take two years at a cost of SEM per year, with a probability of succens of

3

0

%

at the end of the two pears

(

although nobody really lonows yet if any of the participants will live to

2

0

0

)

.

If these clinical trials are declared a success, the drug can proceed to market. In this stage, there would be a $

1

0

M

cost of marketing rach year, and the sales could run for a total of sky years. A succenful drug would eurn a net operating problit

(

not counting the advertising

)

of $

1

5

M in its frist year of market, and this figure can be expected to grew on average at

2

0

%

per year but with a standard deviation of

1

0

0

K

.

This large standard deviation recogibes that the market may be enthuslastic until any patients get any disease or pass away before

2

0

0

which will cause soepticism about Centurion.

Four investment from requires a rate ef return of

2

0

K per annum for this kind of project.

Page

1

ell

2

Unfortunately, your struighe DCI unalyis of the expected canh flows produces the following disappointing result:

\

table

[

[

DCF analysls for Lang Ufe Brups lacerpereted

]

,

[

Tear

,

,

1

,

2

,

3

,

4

,

5

,

6

,

7

,

8

]

,

[

Phase

,

,

Trialis,Triah,Marlast,Market,Market,Marlast,Market,Market

]

,

[

Cent

(

SIM

)

,

,

-

4

.

0

0

0

,

-

4

.

0

0

0

,

-

1

0

.

0

0

0

,

2

0

.

0

0

0

,

-

1

0

.

0

0

0

,

-

1

0

.

0

0

0

,

-

1

0

.

0

0

0

,

-

1

0

.

0

0

0

]

,

[

Expected linotome

[

SM

]

,

,

0

.

0

0

0

,

0

.

0

0

0

,

1

5

.

0

0

0

,

3

8

.

0

0

0

,

7

1

.

4

0

0

,

H

.

9

9

5

,

1

1

.

9

5

4

,

KP

-

3

2

5

]

,

[

Net CF

[

FM

]

,

,

-

6

0

0

0

,

4

0

0

0

,

5

.

0

0

9

,

8

0

0

0

,

1

1

.

4

0

0

,

1

5

.

5

2

0

,

2

1

.

1

0

4

,

2

7

.

3

2

5

]

,

[

Frobability of canh fown,,

1

5

0

%

,

1

0

0

%

,

1

0

%

,

3

0

%

,

HOS,

1

0

%

,

3

0

%

,

1

9

9

4

]

,

[

Expented OP

(

TM

)

,

,

4

.

0

0

0

,

-

4

.

0

0

0

,

1

.

5

0

0

,

2

.

4

0

0

,

3

.

4

8

0

,

4

.

7

7

6

,

6

.

3

3

1

,

8

.

5

9

7

]

,

[

Diabount flactor,

2

0

%

,

0

.

0

3

3

3

3

,

0

.

6

9

4

4

,

0

.

5

7

8

7

,

0

.

4

0

2

2

5

,

0

.

0

0

1

2

8

,

d

.

3

3

4

9

,

0

.

2

9

9

0

8

,

D

.

2

.

2

5

.

5

]

,

[

Diacounted CF

(

5

M

)

,

,

-

5

0

0

6

,

-

4

.

1

6

7

,

0

.

2

5

8

,

1

.

2

5

3

,

3

.

1

1

9

,

1

5

9

9

,

1

7

5

7

,

1

.

5

0

5

]

,

[

NAV

(

5

M

)

,

-

6

.

4

6

0

8

,

,

,

,

,

,

,

,

]

]

propect at the various points along the way. Ulectlarly the DCI in treathy the market period as Europens style by the end of any pear that wan bad.

Four tank in to buld a binomial tree model to value LUDL. Your model wil not look like a truditional call or pue, but

Question

2

-

Binomial Model

This question combines concepts from FN

4

1

3

and FIN

2

0

1

/

3

0

1

.

Long Life Drugs Incorporated

(

L

.

LD

)

has been developing a drug cafled Centurion which they claim will eliminate all diseases and enable people to live for

2

0

0

years. You are attempting to value this firm. Fou are aware that companies in the blotechnology industry can often have significant valuations even though they do not yet have any revenue stream. The value comes from the flute cash flog opportunities if the drug is successful.

LLDI's drug is about to undergo two years of clinical trials. These will take two wars at a cost of $

6

M per year, with a probability of success of

3

0

%

at the end of the two years

(

although nobody really knows yet if any of the participants will live to

2

0

0

)

.

If these clinical trials are declared a success, the dnig can proceed to market. In this stage, there would be a $

1

0

M cost of marketing each year, and the sales could run for a total ell six years. A successful drug would earn a net operating profit

(

not counting the advertining

)

of $

1

5

M in ils finit war on market, and this figure can be expected to grow on average at

2

0

%

per year but with a standard deviation of

1

0

0

%

.

This large standard deviation recognites that the market may be enthuslastic until any patients get any disease or pass away before

2

0

0

which will cause scepticism about Cenfurion.

Your investment firm requires a rate of return of

2

0

%

per annum for this lind of project.

Page

1

of

2

Unfortunately, your straight DCF analyis of the expected cash flows produces the following disappointing result:

\

table

[

[

BES anatyls for teng Life Drugs Incorporated,,,,,,

]

,

[

Year

,

1

,

2

,

3

,

4

,

5

,

6

,

7

,

8

]

,

[

Pharie

,

Trials,Trials,Market,Market,Market,Market,Marhet,Market

]

,

[

Cont

(

$M

)

,

6

.

0

0

0

,

-

6

.

0

0

0

,

-

1

0

.

0

0

0

,

-

3

0

.

0

0

0

,

-

1

0

.

0

0

0

,

-

1

0

.

0

0

0

,

-

1

0

.

0

0

0

,

-

1

0

.

0

0

0

]

,

[

Espected income

(

SU

)

,

0

.

0

0

0

,

0

.

0

0

0

,

1

5

.

0

0

0

,

1

8

.

0

0

0

,

2

1

.

6

0

0

,

2

5

.

9

3

0

,

3

1

.

1

0

4

,

3

7

.

3

2

5

]

,

[

Net CF

(

$M

)

,

6

.

0

0

0

,

-

6

.

0

0

0

,

$

.

0

0

0

,

8

.

0

0

0

,

1

1

.

6

0

0

,

1

5

.

9

2

0

,

2

1

.

1

0

4

,

2

7

.

3

2

5

]

,

[

Probability of cash flows,

1

0

0

%

,

1

0

0

%

,

3

0

%

,

3

0

%

,

3

0

%

,

3

0

%

,

3

0

4

,

1

0

%

]

]

Unfortunately, your straight DCF analysis of the expected cash flows produ. following dirappointing result:

\

table

[

[

BCI analysis for Long Uife Draga Interporated,,,,,,

]

,

[

Year Plase,,

1

Trials,

2

Tria

ee

Ee

et ementnias rete ed bret Er

eet ty ee mt ee er tre

EE

Ee)

TTR

oreo vt rg mf ied opt. oan gin

emia ew tes bE Nm NE MSMR E

foretr Te te CT he i Te i

To gm Te en

toe tv. ct ome cy hd tps

ee eee a Ser 50

[APTPEP—————E———

St tye mh ergo te 1 oo td hi

ee

Ee

et ementnias rete ed bret Er

eet ty ee mt ee er tre

EE

Ee)

TTR

oreo vt rg mf ied opt. oan gin

emia ew tes bE Nm NE MSMR E

foretr Te te CT he i Te i

To gm Te en

toe tv. ct ome cy hd tps

ee eee a Ser 50

[APTPEP—————E———

St tye mh ergo te 1 oo td hi

Asked by: REDDY BHARGAVA SURYA TEJA

Created at: 2025-11-18 19:28:36

Final Answer:

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :