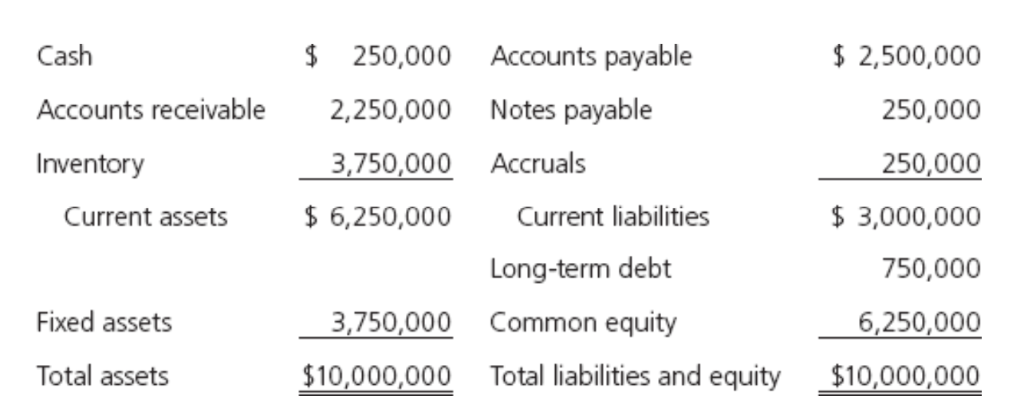

Stewart Manufacturing buys on terms of 2 / 1 0 , net 3 0 , but it has not been paying on time — it is a “ slower payer ” and its suppliers are getting upset. Stewart does not take discounts, and it has been paying in 5 0 rather than the required 3 0 days. Assume that the accounts payable are recorded at full cost, not net of discounts. Stewart ’ s suppliers are fed up and will not continue selling to Stewart unless Stewart begins making prompt payments ( that is , paying in 3 0 days or less ) . The firm is going to have to reduce its level of accounts payable, either to an amount that is equal to 3 0 days purchases ( if it does not take discounts ) or to 1 0 days purchases ( if it decides to take discounts ) . Management has decided to obtain the needed funds by borrowing on an additional 1 - year note payable ( call this a current liability ) from its bank at a rate of 1 6 % , discount interest, with a 1 5 % compensating balance required. The cash currently held by Stewart is needed for transactions, so it cannot be used as part of the compensating balance. So , the issue now facing the company is this: How much trade credit should it use, and how large a loan should it obtain from its bank? Stewart ’ s balance sheet follows:(2) Cost of the bank loan Terms of the bank loan are a 16% discount interest rate, and a 15% compensating balance. This terms (and the effective rate on the loan) are the same regardless of how much the firm borrows. Assume an amount equal to the amount needed if Stewart does not take discounts on its purchases. We will set up a one-year timeline to analyze the cash flow relevant to this situation. 0 (1 Year) 1 ee Ee ee ee mmm ss was De Discount interest — Compensating balance ~~ ———» — Netcashflows ———*> Using the RATE function, we can determine the cost of the bank loan. Cost of bank loan = Co 4493% This cost rate would be the same for the larger loan. Since the cost of the bank loan exceeds the cost of nonfree trade credit, Stewart should take out the smaller bank loan and then use nonfree trade credit. d. Assume that Stewart foregoes the discount and borrows the amount needed to become current on its payables. Construct a pro forma balance sheet based on this decision. (Hint: you will need to include an account called "prepaid interest" under current assets.) The operating assets will remain unchanged, but a new current asset, "Prepaid interest,” will be created. Also, cash will increase by the amount of the compensating balance. On the liability side, accounts payable will decline, and notes payable will increase. Total assets will increase by the sum of the compensating balance and the prepaid interest, or: $ 1449275 Stewart Manufacturing Balance Sheet Cash Accounts payable Accounts Receivable Notes payable Inventory Accruals Prepaid interest Current liabilities Current Assets Long-term debt Fixed assets Common equity Total assets Total liabilities and equity Cash § 250,000 Accounts payable $ 2,500,000 Accounts receivable 2,250,000 Notes payable 250,000 Inventory 3,750,000 Accruals 250,000 Current assets $ 6,250,000 Current liabilities $ 3,000,000 Long-term debt 750,000 Fixed assets 3,750,000 Common equity 6,250,000 Total assets $10,000,000 Total liabilities and equity $10,000,000

Question:

Stewart Manufacturing buys on terms of

2

/

1

0

,

net

3

0

,

but it has not been paying on time

—

it is a

“

slower payer

”

and its suppliers are getting upset. Stewart does not take discounts, and it has been paying in

5

0

rather than the required

3

0

days. Assume that the accounts payable are recorded at full cost, not net of discounts. Stewart

’

s suppliers are fed up and will not continue selling to Stewart unless Stewart begins making prompt payments

(

that is

,

paying in

3

0

days or less

)

.

The firm is going to have to reduce its level of accounts payable, either to an amount that is equal to

3

0

days purchases

(

if it does not take discounts

)

or to

1

0

days purchases

(

if it decides to take discounts

)

.

Management has decided to obtain the needed funds by borrowing on an additional

1

-

year note payable

(

call this a current liability

)

from its bank at a rate of

1

6

%

,

discount interest, with a

1

5

%

compensating balance required. The cash currently held by Stewart is needed for transactions, so it cannot be used as part of the compensating balance. So

,

the issue now facing the company is this: How much trade credit should it use, and how large a loan should it obtain from its bank? Stewart

’

s balance sheet follows:

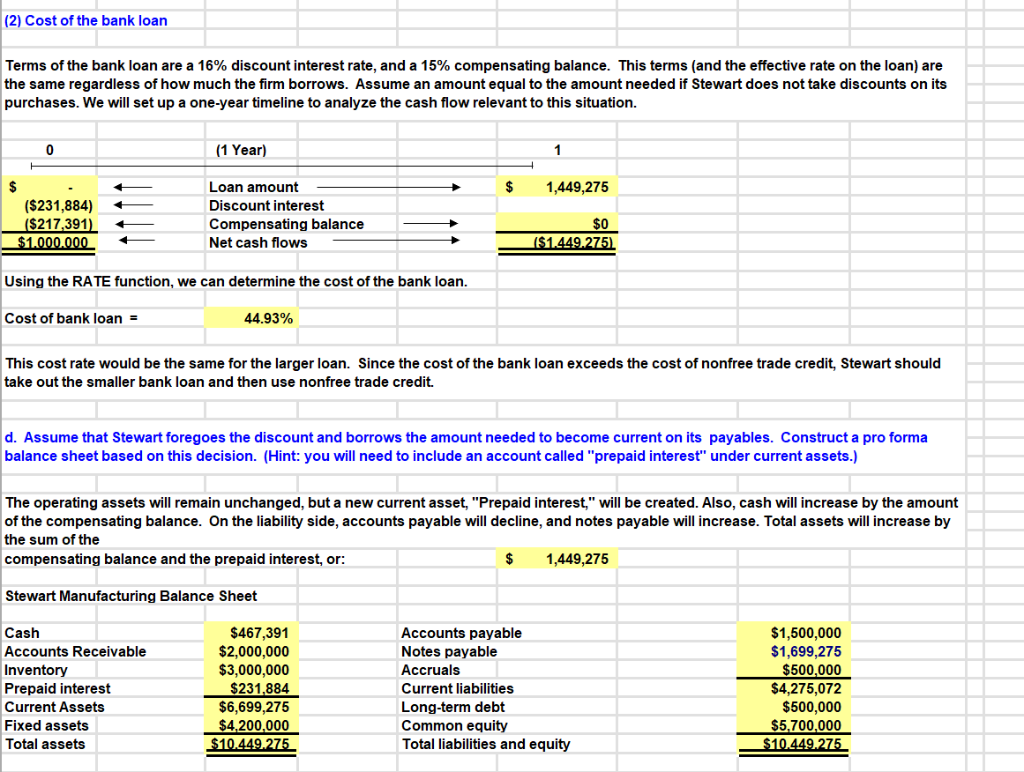

(2) Cost of the bank loan

Terms of the bank loan are a 16% discount interest rate, and a 15% compensating balance. This terms (and the effective rate on the loan) are

the same regardless of how much the firm borrows. Assume an amount equal to the amount needed if Stewart does not take discounts on its

purchases. We will set up a one-year timeline to analyze the cash flow relevant to this situation.

0 (1 Year) 1

ee Ee ee ee

mmm ss was

De Discount interest

— Compensating balance ~~ ———»

— Netcashflows ———*>

Using the RATE function, we can determine the cost of the bank loan.

Cost of bank loan = Co 4493%

This cost rate would be the same for the larger loan. Since the cost of the bank loan exceeds the cost of nonfree trade credit, Stewart should

take out the smaller bank loan and then use nonfree trade credit.

d. Assume that Stewart foregoes the discount and borrows the amount needed to become current on its payables. Construct a pro forma

balance sheet based on this decision. (Hint: you will need to include an account called "prepaid interest" under current assets.)

The operating assets will remain unchanged, but a new current asset, "Prepaid interest,” will be created. Also, cash will increase by the amount

of the compensating balance. On the liability side, accounts payable will decline, and notes payable will increase. Total assets will increase by

the sum of the

compensating balance and the prepaid interest, or: $ 1449275

Stewart Manufacturing Balance Sheet

Cash Accounts payable

Accounts Receivable Notes payable

Inventory Accruals

Prepaid interest Current liabilities

Current Assets Long-term debt

Fixed assets Common equity

Total assets Total liabilities and equity

Cash § 250,000 Accounts payable $ 2,500,000

Accounts receivable 2,250,000 Notes payable 250,000

Inventory 3,750,000 Accruals 250,000

Current assets $ 6,250,000 Current liabilities $ 3,000,000

Long-term debt 750,000

Fixed assets 3,750,000 Common equity 6,250,000

Total assets $10,000,000 Total liabilities and equity $10,000,000

(2) Cost of the bank loan

Terms of the bank loan are a 16% discount interest rate, and a 15% compensating balance. This terms (and the effective rate on the loan) are

the same regardless of how much the firm borrows. Assume an amount equal to the amount needed if Stewart does not take discounts on its

purchases. We will set up a one-year timeline to analyze the cash flow relevant to this situation.

0 (1 Year) 1

ee Ee ee ee

mmm ss was

De Discount interest

— Compensating balance ~~ ———»

— Netcashflows ———*>

Using the RATE function, we can determine the cost of the bank loan.

Cost of bank loan = Co 4493%

This cost rate would be the same for the larger loan. Since the cost of the bank loan exceeds the cost of nonfree trade credit, Stewart should

take out the smaller bank loan and then use nonfree trade credit.

d. Assume that Stewart foregoes the discount and borrows the amount needed to become current on its payables. Construct a pro forma

balance sheet based on this decision. (Hint: you will need to include an account called "prepaid interest" under current assets.)

The operating assets will remain unchanged, but a new current asset, "Prepaid interest,” will be created. Also, cash will increase by the amount

of the compensating balance. On the liability side, accounts payable will decline, and notes payable will increase. Total assets will increase by

the sum of the

compensating balance and the prepaid interest, or: $ 1449275

Stewart Manufacturing Balance Sheet

Cash Accounts payable

Accounts Receivable Notes payable

Inventory Accruals

Prepaid interest Current liabilities

Current Assets Long-term debt

Fixed assets Common equity

Total assets Total liabilities and equity

Cash § 250,000 Accounts payable $ 2,500,000

Accounts receivable 2,250,000 Notes payable 250,000

Inventory 3,750,000 Accruals 250,000

Current assets $ 6,250,000 Current liabilities $ 3,000,000

Long-term debt 750,000

Fixed assets 3,750,000 Common equity 6,250,000

Total assets $10,000,000 Total liabilities and equity $10,000,000

Asked by: REDDY BHARGAVA SURYA TEJA

Created at: 2025-11-28 09:16:21

Final Answer:

📢 Instructions:

- Ask anything relatd to above question only.

- For new Question goto :