Summarize briefly about :

Act like a helpful tutor and exlain me :

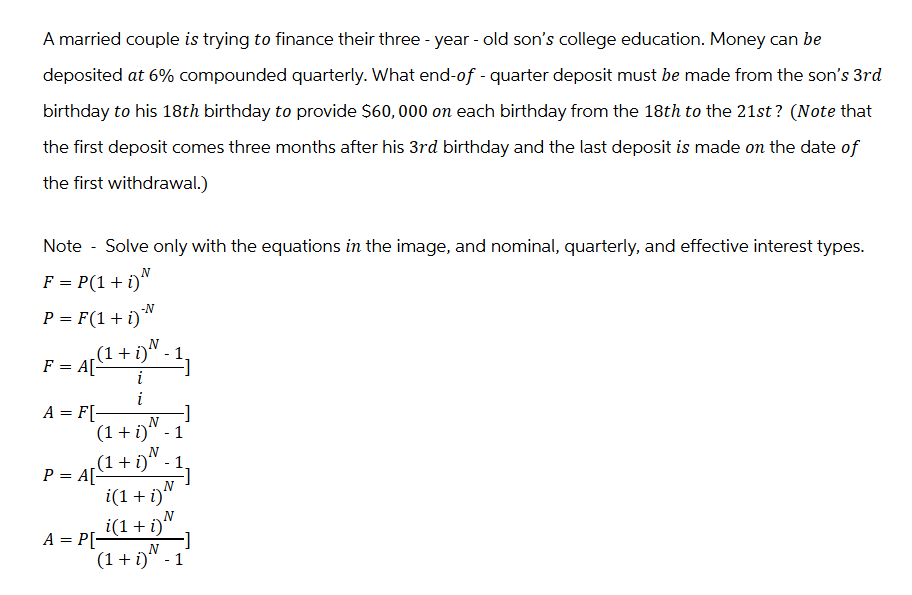

Give step-by-step solution with explanation and final answer:A married couple is trying to finance their three - year - old son's college education. Money can be

deposited at 6% compounded quarterly. What end-of - quarter deposit must be made from the son's 3rd

birthday to his 18th birthday to provide $60,000 on each birthday from the 18th to the 21st? (Note that

the first deposit comes three months after his 3rd birthday and the last deposit is made on the date of

the first withdrawal.)

Note - Solve only with the equations in the image, and nominal, quarterly, and effective interest types.

F=pP+D)"

P=Fa+i)"

~N

a+ 1

Foal

A=F———]

a+p¥-1

N

1+ -1

poait -t +1

(1+)

. ~N

1+

A= pt

a+p¥-1

Question:

Summarize briefly about :

Act like a helpful tutor and exlain me :

Give step-by-step solution with explanation and final answer:A married couple is trying to finance their three - year - old son's college education. Money can be

deposited at 6% compounded quarterly. What end-of - quarter deposit must be made from the son's 3rd

birthday to his 18th birthday to provide $60,000 on each birthday from the 18th to the 21st? (Note that

the first deposit comes three months after his 3rd birthday and the last deposit is made on the date of

the first withdrawal.)

Note - Solve only with the equations in the image, and nominal, quarterly, and effective interest types.

F=pP+D)"

P=Fa+i)"

~N

a+ 1

Foal

A=F———]

a+p¥-1

N

1+ -1

poait -t +1

(1+)

. ~N

1+

A= pt

a+p¥-1

This is AI generated Response.

Asked by: Smart Tv

Created at: 2025-09-18 09:00:32

Final Answer:

RenderedRaw Text

Did you like this answer?

Let's break down the problem and solve it step-by-step:

---

### **1. Understand the Problem**

- **Goal:** Make equal end-of-quarter deposits from son's 3rd birthday (first deposit 3 months after 3rd birthday) to his 18th birthday (last deposit at 18th birthday), such that there will be **$60,000 available on each birthday from the 18th to the 21st** for college.

- **Interest:** 6% compounded quarterly.

- **Withdrawal:** 4 withdrawals of $60,000 each (ages 18, 19, 20, 21).

---

### **2. Find the Quarterly Interest Rate**

- **Nominal Rate (annual, compounded quarterly):** \( r = 6\% \)

- **Quarterly Interest Rate:** \( i = \frac{0.06}{4} = 0.015 \)

---

### **3. Timeline and Number of Periods**

- **Deposits:** From age 3 (after 3rd birthday) to age 18 (at 18th birthday).

- Number of years = \( 18 - 3 = 15 \) years

- Number of quarters = \( 15 \times 4 = 60 \)

- **Number of deposits:** 60 (one each quarter, last one at 18th birthday)

- **Withdrawals:** 1 each at 18th, 19th, 20th, and 21st birthday.

- 4 annual withdrawals

---

### **4. Calculate the Present Value Required at 18th Birthday**

We need enough money at the 18th birthday to fund four annual withdrawals of $60,000 each (at ages 18, 19, 20, 21).

Let’s treat this as the **present value** of an ordinary annuity (annual withdrawals, but interest is quarterly).

- **Each withdrawal:** $60,000

- **Number of withdrawals:** 4

- **Effective interest per year (compounded quarterly):**

\[

(1 + i)^4 - 1 = (1.015)^4 - 1 \approx 0.06136

\]

So, the annual effective interest rate is about 6.136%.

#### **Present Value at 18th birthday:**

Using the formula for the present value of an ordinary annuity (from the given formulas, in terms of annual payments and effective annual rate):

\[

P = A \left[ \frac{1 - (1 + i)^{-N}}{i} \right]

\]

But since withdrawals are annual and interest is compounded quarterly, use the annual effective rate \( i_{eff} = 0.06136 \).

\[

P = 60,000 \left[ \frac{1 - (1 + 0.06136)^{-4}}{0.06136} \right]

\]

Calculate:

- \( (1 + 0.06136)^{-4} = (1.06136)^{-4} \approx 0.7823 \)

- \( 1 - 0.7823 = 0.2177 \)

- \( \frac{0.2177}{0.06136} \approx 3.548 \)

- \( 60,000 \times 3.548 \approx \$212,880 \)

**So, at the 18th birthday, we need $212,880 available.**

---

### **5. Find the End-of-Quarter Deposit (A) Needed**

Now, we have to find the quarterly deposit \( A \) that will accumulate to $212,880 at the end of 60 quarters (from just after age 3 to just at 18th birthday).

Use the future value formula for an ordinary annuity:

\[

F = A \left[ \frac{(1 + i)^N - 1}{i} \right]

\]

Where:

- \( F = 212,880 \)

- \( i = 0.015 \)

- \( N = 60 \)

Solve for \( A \):

\[

A = F \left[ \frac{i}{(1 + i)^N - 1} \right]

\]

Calculate \( (1.015)^{60} \):

- \( \ln(1.015) \approx 0.01489 \)

- \( 0.01489 \times 60 = 0.8934 \)

- \( e^{0.8934} \approx 2.443 \)

- \( (1.015)^{60} - 1 = 2.443 - 1 = 1.443 \)

Now substitute:

\[

A = 212,880 \times \frac{0.015}{1.443}

\]

\[

A = 212,880 \times 0.0104 \approx \$2,216.20

\]

---

## **Final Step-by-Step Answer**

### **Summary Table**

| Step | Calculation | Result |

|------|-------------|--------|

| 1 | Quarterly rate \( i \) | 0.015 |

| 2 | Effective annual rate \( i_{eff} \) | 0.06136 |

| 3 | PV at 18th birthday | \$212,880 |

| 4 | Number of deposits | 60 |

| 5 | Quarterly deposit \( A \) | \$2,216.20 |

### **Final Answer**

\[

\boxed{

\text{The end-of-quarter deposit that must be made is approximately } \$2,216.20.

}

\]

---

**Explanation:**

From the 3rd to the 18th birthday (60 quarters), depositing \$2,216.20 at the end of each quarter at 6% compounded quarterly will provide \$60,000 on each birthday from the 18th to 21st.

VIPSolutions focuses on clear, step‑by‑step explanations so you can learn quickly. Whether you need an AI‑generated walkthrough or a short hint to get unstuck, each solution is organized for fast reading and easy review later.

Search similar questions, compare approaches, and bookmark the best answers for revision. Our goal is simple: quick, reliable study help that feels natural—not noisy.

A married couple is trying to finance their three - year - old son's college education. Money can be

deposited at 6% compounded quarterly. What end-of - quarter deposit must be made from the son's 3rd

birthday to his 18th birthday to provide $60,000 on each birthday from the 18th to the 21st? (Note that

the first deposit comes three months after his 3rd birthday and the last deposit is made on the date of

the first withdrawal.)

Note - Solve only with the equations in the image, and nominal, quarterly, and effective interest types.

F=pP+D)"

P=Fa+i)"

~N

a+ 1

Foal

A=F———]

a+p¥-1

N

1+ -1

poait -t +1

(1+)

. ~N

1+

A= pt

a+p¥-1

A married couple is trying to finance their three - year - old son's college education. Money can be

deposited at 6% compounded quarterly. What end-of - quarter deposit must be made from the son's 3rd

birthday to his 18th birthday to provide $60,000 on each birthday from the 18th to the 21st? (Note that

the first deposit comes three months after his 3rd birthday and the last deposit is made on the date of

the first withdrawal.)

Note - Solve only with the equations in the image, and nominal, quarterly, and effective interest types.

F=pP+D)"

P=Fa+i)"

~N

a+ 1

Foal

A=F———]

a+p¥-1

N

1+ -1

poait -t +1

(1+)

. ~N

1+

A= pt

a+p¥-1